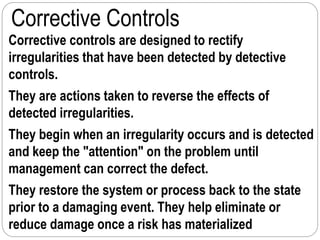

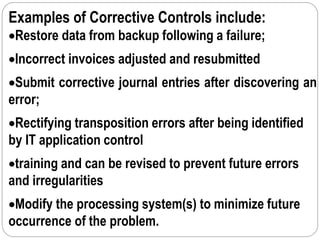

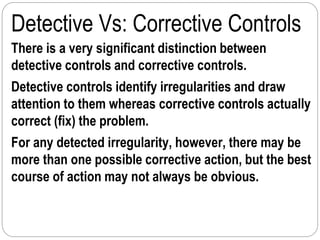

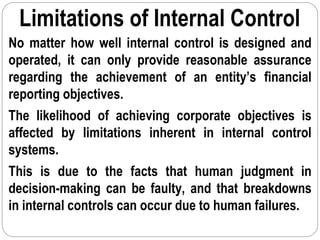

The document discusses the three main types of internal controls: preventive, detective, and corrective controls. It provides examples for each type and explains the key differences between detective and corrective controls. The document also discusses some limitations of internal controls, noting that they can only provide reasonable assurance and not absolute guarantees due to factors like human judgment errors. It identifies the five main components of an effective internal control system according to international standards.

![1. The Control Environment

The control environment is the foundation for all other

components of internal control, providing discipline

and structure.

The importance of internal control to the entity is

reflected in the overall attitude and actions of

management:

through those charged with governance [e.g. board of

directors (BOD)] and

owners with regard to control provided by the BOD](https://image.slidesharecdn.com/topic3internalcontrols-240123151825-8d6571a9/85/topic-3-internal-controls-audit-pptx-18-320.jpg)