Downloaded 7,292 times

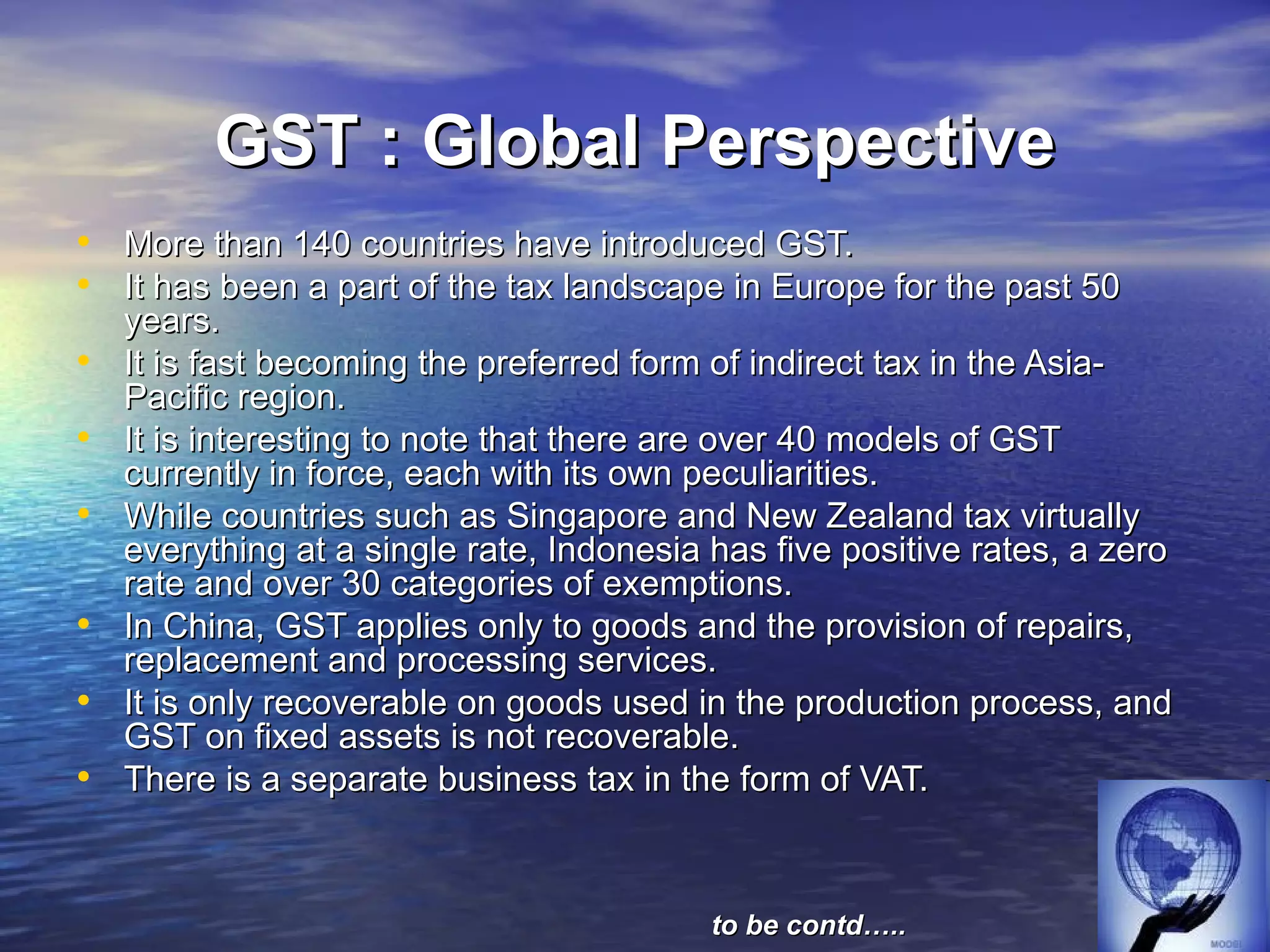

This document provides an overview of the Goods and Services Tax (GST) in India. It discusses the key features of GST, including that it will combine multiple taxes into a single tax on goods and services, provide full tax credits, and follow a multi-rate structure. The document also reviews the journey towards implementing GST in India and compares GST structures in other countries.

![GST RETURNS [ TAXATION ]](https://cdn.slidesharecdn.com/ss_thumbnails/taxationgstreturns-210303051831-thumbnail.jpg?width=640&height=640&fit=bounds)