This document provides an overview of the Goods and Services Tax (GST) system that is being implemented in India. Some key points:

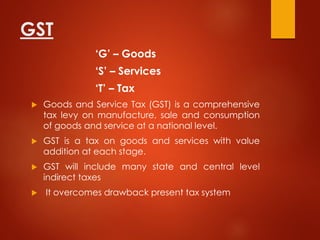

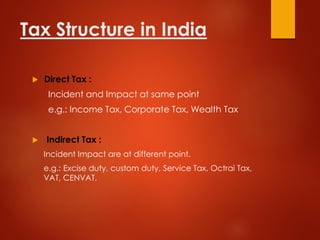

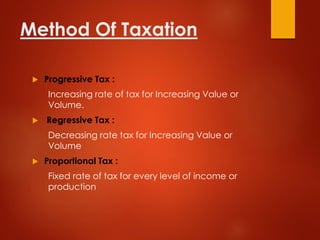

- GST is a comprehensive indirect tax that will combine multiple state and central taxes into one. It is levied at each stage of production and distribution.

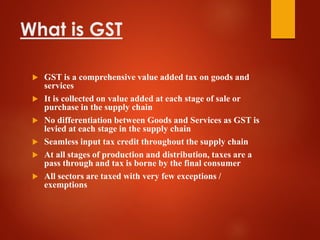

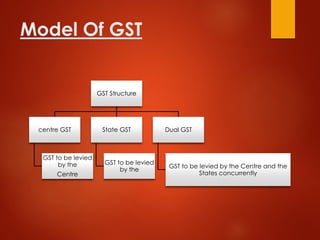

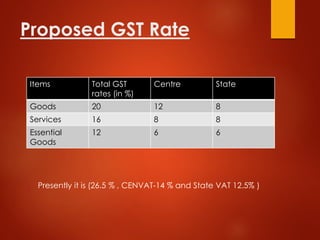

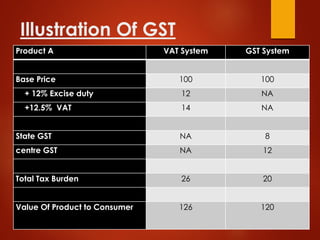

- The proposed GST structure has two components - Central GST to be levied by the Centre and State GST to be levied by the states. Standard rates are proposed at 20% for goods and 16% for services.

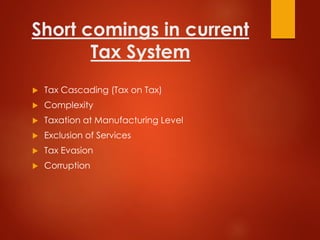

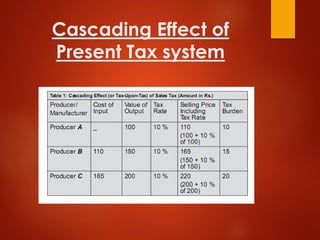

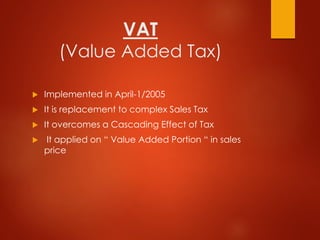

- GST aims to reduce tax cascading and make India's tax system simpler, more transparent and boost the economy by making exports more competitive.

- There were challenges

![Power point presentation on gst[goods and service tax ]](https://cdn.slidesharecdn.com/ss_thumbnails/powerpointpresentationongst-200315095209-thumbnail.jpg?width=640&height=640&fit=bounds)

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)