Downloaded 150 times

![Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

1

SERVICE TAX DOSSIER

on

EDUCATIONAL SERVICES

Introduction

Education is the life line of any nation and blood for economic growth. Our Government realizes

its importance and hence has taken several initiatives to boost the growth of this sector,

including setting up of several universities, deregulating policies and making significant pacts

with foreign nations. While education is a priority in Indian context, given its population base and

mounting service sector and its contribution to GDP, (about 60% now), coaching, which aids or

supplements formal education also plays a catalytic role in advancement of education in our

Country. Coaching, which is generally imparted on commercial basis is deep rooted in Indian

system and cannot be ignored or left unnoticed. Infact coaching and education go hand in hand

to a large extent.

Understanding the Concept of Education and Coaching

All education is not exempted and all coachings are not taxed. However, one needs to

understand the difference between the two terms – education and coaching.

According to Aiyar’s Advanced Law Lexicon, education means the bringing up, the process

of developing and training the powers and capabilities of human beings. It is an act of

providing with knowledge.

Coaching or training is a very narrow activity imparting skill in a particular discipline but

education is a broader term which is a process of development of personality of body, mind

and intellect. The scope of education is broad but training or coaching is in a particular field.

In ICAFI case [2009 -TMI - 32004 - Cestat, Bangalore], tribunal observed that coaching

normally refers to a special teaching or a personalized teaching in certain subjects. Training

is generally used to refer to practical instruction or learning process. Education is the

process of overall development of a person. It included moral, intellectual and physical

development of a child or a person. It is not restricted to a particular subject and it covers](https://image.slidesharecdn.com/x2vkk3fer0jxarumoyaa-signature-0eb22c7754159c56f3b2001536c4f1dd0e1935bc2fc5811546367e407efebf3b-poli-150120034558-conversion-gate02/85/Service-tax-dossier-on-educational-services-1-320.jpg)

![Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

1

SERVICE TAX DOSSIER

on

EDUCATIONAL SERVICES

Introduction

Education is the life line of any nation and blood for economic growth. Our Government realizes

its importance and hence has taken several initiatives to boost the growth of this sector,

including setting up of several universities, deregulating policies and making significant pacts

with foreign nations. While education is a priority in Indian context, given its population base and

mounting service sector and its contribution to GDP, (about 60% now), coaching, which aids or

supplements formal education also plays a catalytic role in advancement of education in our

Country. Coaching, which is generally imparted on commercial basis is deep rooted in Indian

system and cannot be ignored or left unnoticed. Infact coaching and education go hand in hand

to a large extent.

Understanding the Concept of Education and Coaching

All education is not exempted and all coachings are not taxed. However, one needs to

understand the difference between the two terms – education and coaching.

According to Aiyar’s Advanced Law Lexicon, education means the bringing up, the process

of developing and training the powers and capabilities of human beings. It is an act of

providing with knowledge.

Coaching or training is a very narrow activity imparting skill in a particular discipline but

education is a broader term which is a process of development of personality of body, mind

and intellect. The scope of education is broad but training or coaching is in a particular field.

In ICAFI case [2009 -TMI - 32004 - Cestat, Bangalore], tribunal observed that coaching

normally refers to a special teaching or a personalized teaching in certain subjects. Training

is generally used to refer to practical instruction or learning process. Education is the

process of overall development of a person. It included moral, intellectual and physical

development of a child or a person. It is not restricted to a particular subject and it covers](https://image.slidesharecdn.com/x2vkk3fer0jxarumoyaa-signature-0eb22c7754159c56f3b2001536c4f1dd0e1935bc2fc5811546367e407efebf3b-poli-150120034558-conversion-gate02/75/Service-tax-dossier-on-educational-services-1-2048.jpg)

![Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

6

designated trades as notified under the Apprentices Act, 1961. (w.e.f. 10-5-2013,

affiliations to State Council for Vocational Training are also covered)

a Modular Employable Skill Course, approved by the National Council of

Vocational Training, run by a person registered with the Directorate General of

Employment and Training, Ministry of Labour and Employment, Government of

India.

a course run by an institute affiliated to the National Skill Development

Corporation set up by the Government of India. (only upto 9-5-2013)

Negative list may, therefore, not include –

a) Private tuitions

b) Education as a part of prescribed curriculum for obtaining qualification

recognized by law of a foreign country

c) Services provided to educational institutions (except covered elsewhere)

d) Placement services

e) Services provided by educational Institutes such as IITs, ITMs charge a fee from

prospective employers like corporate houses / MNCs, who come to the institutes

for recruiting candidates through campus interview.

The admission / examination fee is covered under negative list. Further, tuition fee or

development fees are also not liable for Service Tax. When students avail the services of

admission / development / examination and pay the fees in respect of such services

alongwith basic tuition fee, it may be considered as a case of bundled services where tuition

is having dominant nature covered under negative list and accordingly, all other fees

charged mandatorily along with tuition fees would not be liable for service tax.

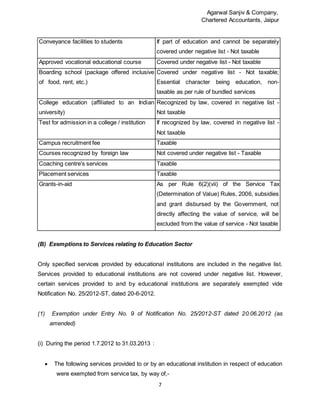

The inclusion in / exclusion from negative list [section 66D(l) of Finance Act, 1994 ] for

different types of education related services can be illustrated as follows :

Nature of Service Taxability

School education upto 12th

standard Covered under negative list - Not taxable.

School examinations fee, etc. It is part of education and hence covered under

the negative list - Not taxable](https://image.slidesharecdn.com/x2vkk3fer0jxarumoyaa-signature-0eb22c7754159c56f3b2001536c4f1dd0e1935bc2fc5811546367e407efebf3b-poli-150120034558-conversion-gate02/85/Service-tax-dossier-on-educational-services-6-320.jpg)

![Agarwal Sanjiv & Company,

Chartered Accountants, Jaipur

16

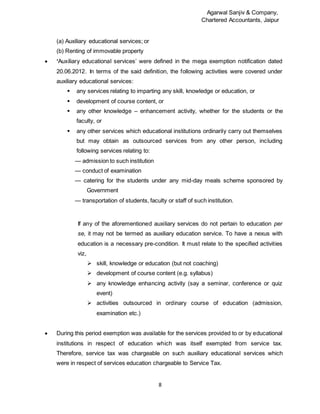

Relevant Provisions / Notifications etc.

Upto 30.06.2012

1. Section 65(26) of the Finance Act, 1994 – Meaning of Commercial Training or Coaching

2. Section 65(27) of the Finance Act, 1994 – Meaning of Commercial Training or Coaching

Centre

3. Section 65(105) (zzzc) of the Finance Act, 1994 – Taxable Services relating to

Commercial Training & Coaching

w.e.f. 01.07.2012

1. Section 65B(11) of Finance Act, 1994 - Definition of Approved Vocational Education

Course

2. Clause (l) of Section 66D of Finance Act, 1994 i.e. Negative List – Pre –school, higher

secondary, vocational education etc.

3. Notification 25/2012 – ST dated 20.06.2012 - Entry No. 9 & 12 – Services provided to or

by educational institutions and construction services respectively

4. Para 2 (f) of Notification 25/2012 – ST dated 20.06.2012 – Definition of Auxiliary

Education Services (deleted w.e.f 11.07.2014)

5. Para 2 (oa) of Notification 25/2012 – ST dated 20.06.2012 - Education Institution [para 2

(oa)]

6. Notification No. 30/2012-ST dated 20.06.2012 – Reverse charge provisions

7. CBEC Letter No. 334/3/2013-TRU dated 28/02/2013 – CBEC clarification on exemption

8. Circular No. 172/7/2013 –ST dated 19.09.2013- CBEC clarification on exempt services –

Auxiliary Education Services

For clarification, please contact:

AGARWAL SANJIV & COMPANY

CHARTERED ACCOUNTANTS

503, GURUKRIPA TOWER,

MAHAVEER MARG,

C-SCHEME,

JAIPUR-302001

Phone : 0141-2368071, Fax : 0141-2369250

E- mail :asandco@gmail.com](https://image.slidesharecdn.com/x2vkk3fer0jxarumoyaa-signature-0eb22c7754159c56f3b2001536c4f1dd0e1935bc2fc5811546367e407efebf3b-poli-150120034558-conversion-gate02/85/Service-tax-dossier-on-educational-services-16-320.jpg)

The document discusses the tax treatment of educational and coaching services under Indian service tax law, both prior to and after July 1, 2012. Key points: 1) Prior to July 1, 2012, only specified commercial coaching and training services were taxable, while educational services were excluded. 2) After July 1, 2012, all services are taxable unless specifically exempted or included in the negative list. The negative list includes pre-school, school, and vocational education, as well as education leading to a recognized qualification. 3) Some auxiliary educational services and renting of property to educational institutions are also exempted until March 31, 2013, but services provided by educational institutions became taxable