Downloaded 30 times

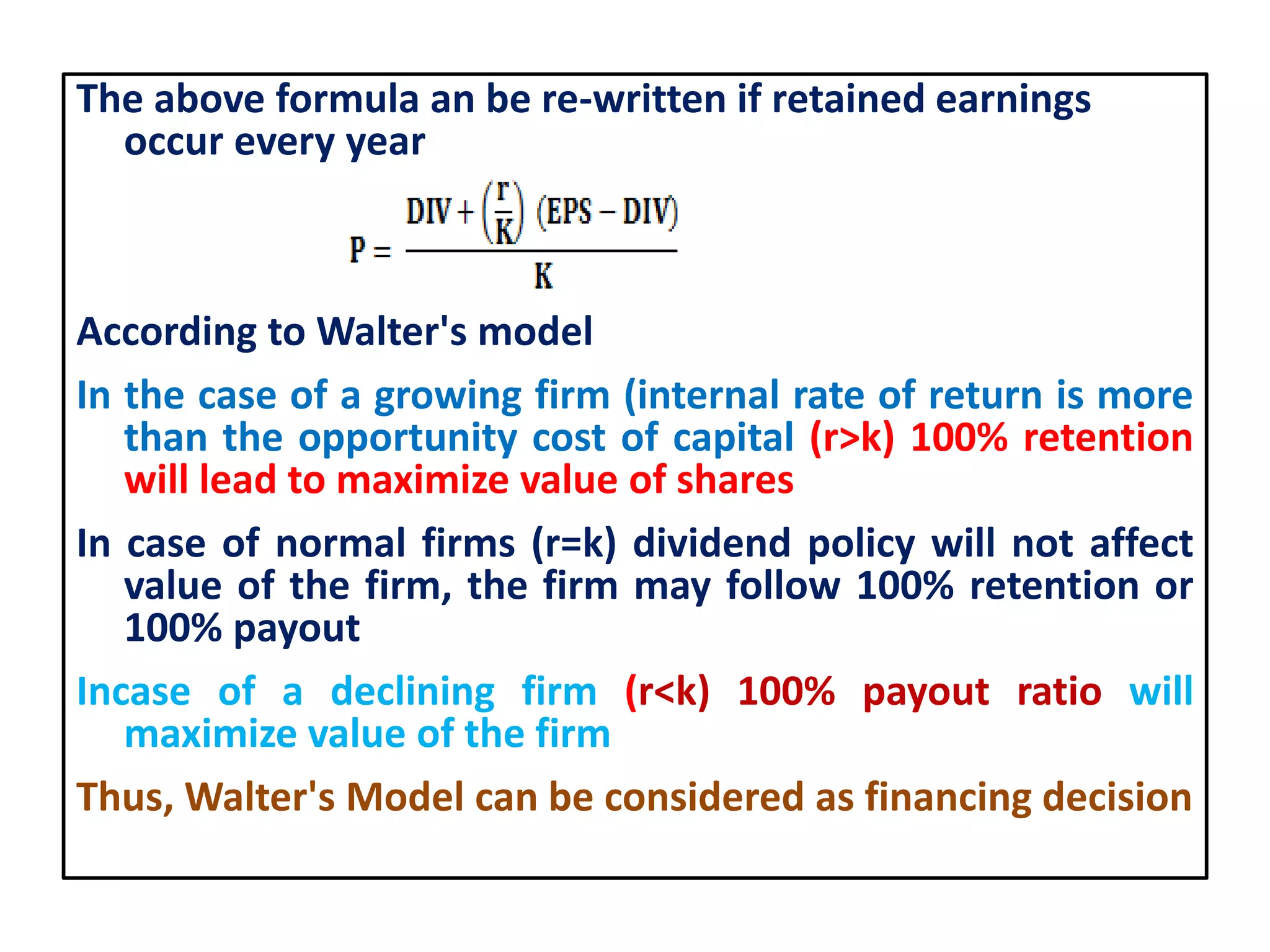

This document discusses theories related to corporate dividend decisions and their impact on firm value. It outlines two broad categories of theories: theories of irrelevance, which argue dividend decisions do not affect firm value, and theories of relevance, which argue they do. Key theories discussed include the residual approach, Modigliani-Miller approach, Walter's model, and Gordon's model. The document analyzes the assumptions and conclusions of each theory regarding how different dividend policies impact firm value under varying conditions.