Downloaded 19 times

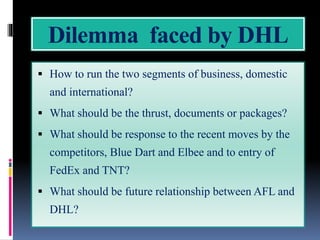

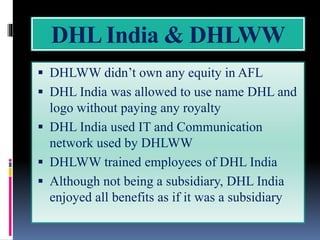

DHL India faces a dilemma on how to manage its domestic and international business segments and whether to focus on documents or packages. Increased competition from players like Blue Dart and the entry of FedEx and TNT into the Indian market have added challenges. DHL India enjoys benefits from its relationship with DHL Worldwide like brand recognition, but it is not a subsidiary. It aims to strengthen its position with ISO certification and alliances while improving delivery and repositioning as a total logistics provider.