Downloaded 83 times

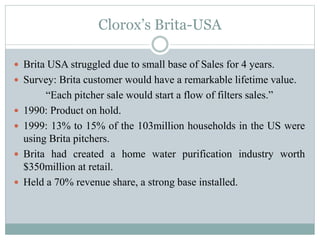

- The document discusses Brita, a water filtration company that was acquired by Clorox in 1988. It summarizes Brita's history, products, marketing strategies, and competition. - Brita struggled initially in the US but grew rapidly after Clorox implemented new marketing campaigns focusing on the taste benefits of filtered water. Brita captured 70% of the home water filtration market by 1999. - Brita's main competitor was PUR, which had technological advantages in its faucet-mounted filters and spent heavily on advertising. The document analyzes Brita's options in response to the growing faucet filter segment and increased competition from PUR and other companies.