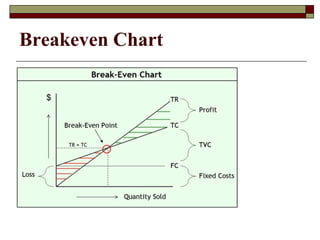

Breakeven analysis examines the relationship between changes in sales volume, revenue, expenses, and profit. It is used for short-term planning and decision making. Key calculations include determining the breakeven point in units or sales to cover fixed costs, and the margin of safety which is the difference between budgeted sales and breakeven sales. The breakeven formula divides fixed costs by the contribution margin per unit to find the breakeven point in units. Breakeven charts can also be used to visualize these relationships.

![Breakeven_Analysis_0[1].ppt](https://image.slidesharecdn.com/breakevenanalysis01-220916071656-ab750b6d/85/Breakeven_Analysis_0-1-ppt-16-320.jpg)