Download to read offline

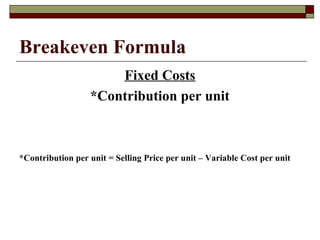

Breakeven analysis examines the relationship between changes in volume, total sales revenue, expenses, and net profit. It is also known as cost-volume-profit (CVP) analysis. Breakeven analysis is used for short-term planning and decision making by looking at how costs, revenue, output levels, and profit relate. It determines the break even point where a company makes no profit or loss and calculates the margin of safety.

![Breakeven_Analysis_0[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/breakevenanalysis01-220916071656-ab750b6d-thumbnail.jpg?width=640&height=640&fit=bounds)