Downloaded 52 times

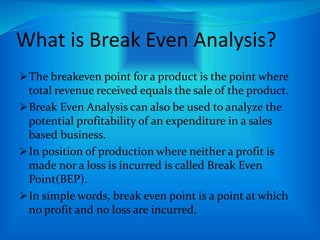

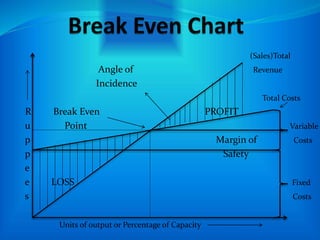

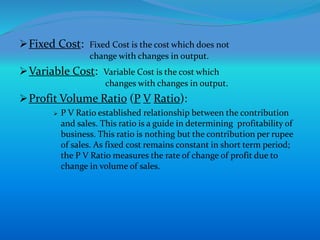

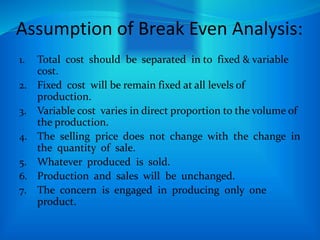

This document provides an overview of break even analysis. It defines break even point as the point where total revenue equals total costs, meaning no profit or loss. It explains the components of break even analysis including fixed costs, variable costs, contribution, and profit volume ratio. The document also lists the key assumptions of break even analysis, such as fixed costs remaining constant, variable costs changing proportionally with production, price remaining constant, all production being sold, and production and sales remaining unchanged.