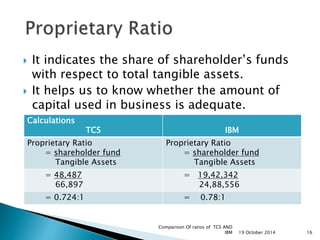

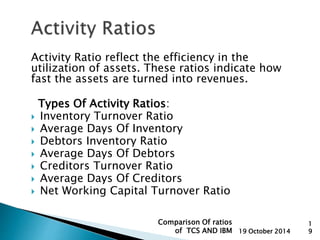

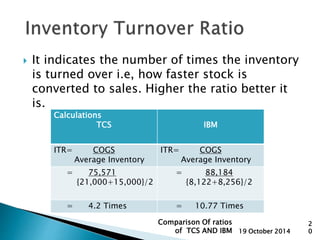

The document presents a detailed comparison of key financial ratios between Tata Consultancy Services (TCS) and International Business Machines (IBM) as of October 2014. It covers various categories of ratios including profitability, liquidity, leverage, activity, and market ratios, providing specific calculations and results for each. The analysis highlights the financial health and performance of both companies using different metrics such as gross profit margin, current ratio, and return on equity.