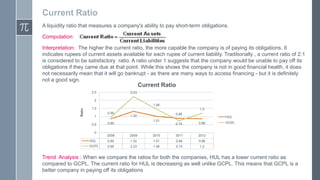

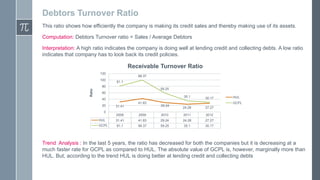

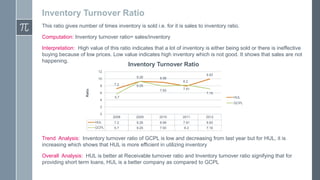

Downloaded 87 times

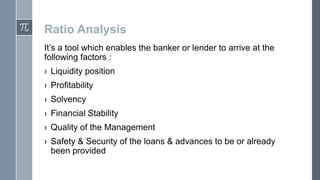

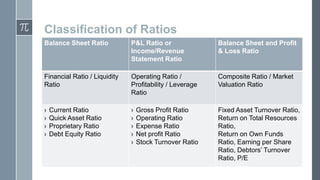

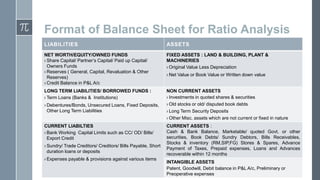

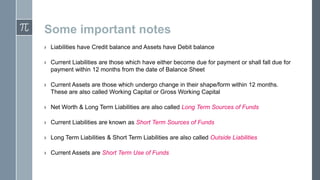

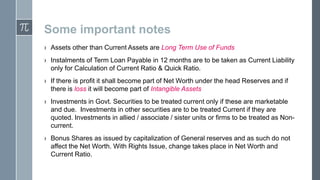

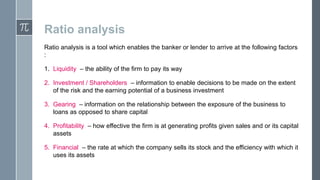

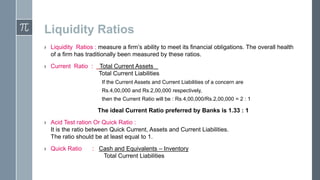

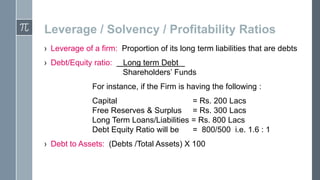

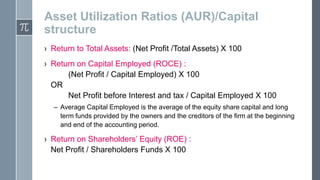

Ratio analysis is a tool used to analyze financial statements and determine a firm's liquidity, profitability, and financial stability. It involves calculating various ratios using data from the income statement and balance sheet, and comparing them over time and against industry benchmarks. The document discusses various types of ratios like liquidity, leverage, asset utilization, and market valuation ratios. It also provides the formulas to calculate important ratios like current ratio, debt-to-equity, return on equity, and earnings per share. The document is intended to explain the concept of ratio analysis and its importance for financial statement evaluation.