This document discusses internal controls, internal checks, internal audits, and the differences between them. It provides advantages and limitations of each. Internal controls help ensure organizational objectives are achieved. Internal checks involve separating duties so employees check each other's work. Internal audits continuously review financial and operational matters to detect errors and fraud. Key differences include internal checks focusing on transaction processing while internal controls ensure policy compliance, and internal audits are appointed by management for early error detection versus statutory audits appointed by shareholders.

Advantages

Accurate andreliable data.

It ensures that the policies and procedures prescribed

by the management are followed by the employees.

It promotes operational efficiency.

It helps the organization to attain its goal effectively.

It safeguards the assets and the records of the

business.

4.

limitations

As long aspeople perform control procedures,

an internal control system will be vulnerable to

human error.

Errors can arise from misunderstandings,

mistakes in judgment, carelessness, distraction, or

fatigue.

Separation of duties can be defeated through

collusion by employees who secretly agree to deceive a

company.

6.

INTERNALCHECK

Internal check isan accounting procedure whereby

routine entries for transactions are handled by more

than one employee in such a manner that the work of

one employee is automatically checked against the work

of another.

7.

ObjectivesOf Internal Check

Divisionof work – It is based on individual’s ability.

Use of devices – An organization should use various

devices which helps to make work of internal check

easier.

Minimization of errors and frauds – The work

performed by each individual is checked by another

individual.

Reliability – If the internal check is very good then

the auditor will rely upon the books of accounts.

Preparation of final accounts – With an effective

internal check system the final accounts can be

prepared safely.

8.

ADVANTAGES

Fixation of responsibility– A Proper internal check

system will ensure accountability and responsibility

of the employees.

Prevention of Errors and Frauds – Under this system

no one employee is allowed to record more than 1 aspect

of the transaction.

Increase the efficiency of clerks – The work is

divided among the employees according to their

Qualification and experience.

9.

Reliability of information– The aim of this system is

to have an accurate record of all the transactions.

Reduces the workload of auditor – In relation to the

extent of audit procedures followed or adopted.

Increases the overall efficiency of the business –

By preventing occurrence of the frauds, proper

segregation of duties which will increase the efficiency.

10.

limitations

Expensive – Itis applicable only for large business

concerns.

Does not reduce the liability – It will help the

auditor in reducing his work but it will never reduce

the liability.

Carelessness – Sometimes employees may become

less serious towards the work.

11.

Duties of anAuditor as Regards

Internal Check System

Examination -

First of all an auditor should satisfy himself about the

working of proper internal control system.

In Case Of Satisfactory System -

If the auditor is satisfied about the effectiveness of internal

control then he should check the efficiency and its existence

by checking various items from different place.

Unsatisfactory Case -

If the auditor feels that internal control system is not

satisfactory then he should check those accounts where

errors are likely to exist.

12.

Some Sections AreInadequate -

If auditor feels that over all system is satisfactory but

certain sections of the system appears to be

inadequate then he should inform the client about the

dangers.

Suggestions -

Auditor should also give suggestions that how

weaknesses can be removed if he is asked by the client.

RELATION TO RECEIPTSOF

CASH

Receipts of a cash must be handled by a separate clerk

known as cashier.

Bank reconciliation statement should be prepared by

the cashier to reconcile bank and cash balance.

All debtors or customers requested to make payments

by crossed cheques.

Automatic bills or cash registers are useful for checking

receipts.

The counter-foils of all the receipts issued should be

properly maintained.

15.

RELATION TO PAYMENTSOF

CASH

All payments should be made by cheques.

Petty cash payment should be handled by the petty

cashier.

Names, numbers and the status of persons authorized

to sign cheques must be decided.

Confirmation of accounts with creditors should be

made to maintain up-to-date records.

A proper system must be adopted for controlling the

supply and issue of cheques.

16.

RELATION TO CASHSALES

Separate salesman should be appointed to carry out

sales at different counters.

The salesman should prepare sales invoice into four

copies.

The accountant must make the entries in cash book.

Salesman should prepare a summary showing cash

sales.

Copies of the sales summary sheet should be sent to

the officer-in-charge of the trading house.

Advantages

Accounting remainscorrect - Staffs remain alert

because their work shall be checked by the internal

auditor.

Helps to detect errors and frauds - Provides

suggestions to improve them which helps the

management to take corrective action.

Detects the misuse of resources - Which helps to

reduce unnecessary expenses.

21.

Checks theefficiency of staffs - Which helps to

increase the efficiency of them.

Makes work easier - Checks the books of accounts,

detects errors and frauds and helps in its correction

which makes the act of final auditor easier.

Increases the morale of honest staff – It is

because evaluation of performance of any staffs will be

made at any time.

22.

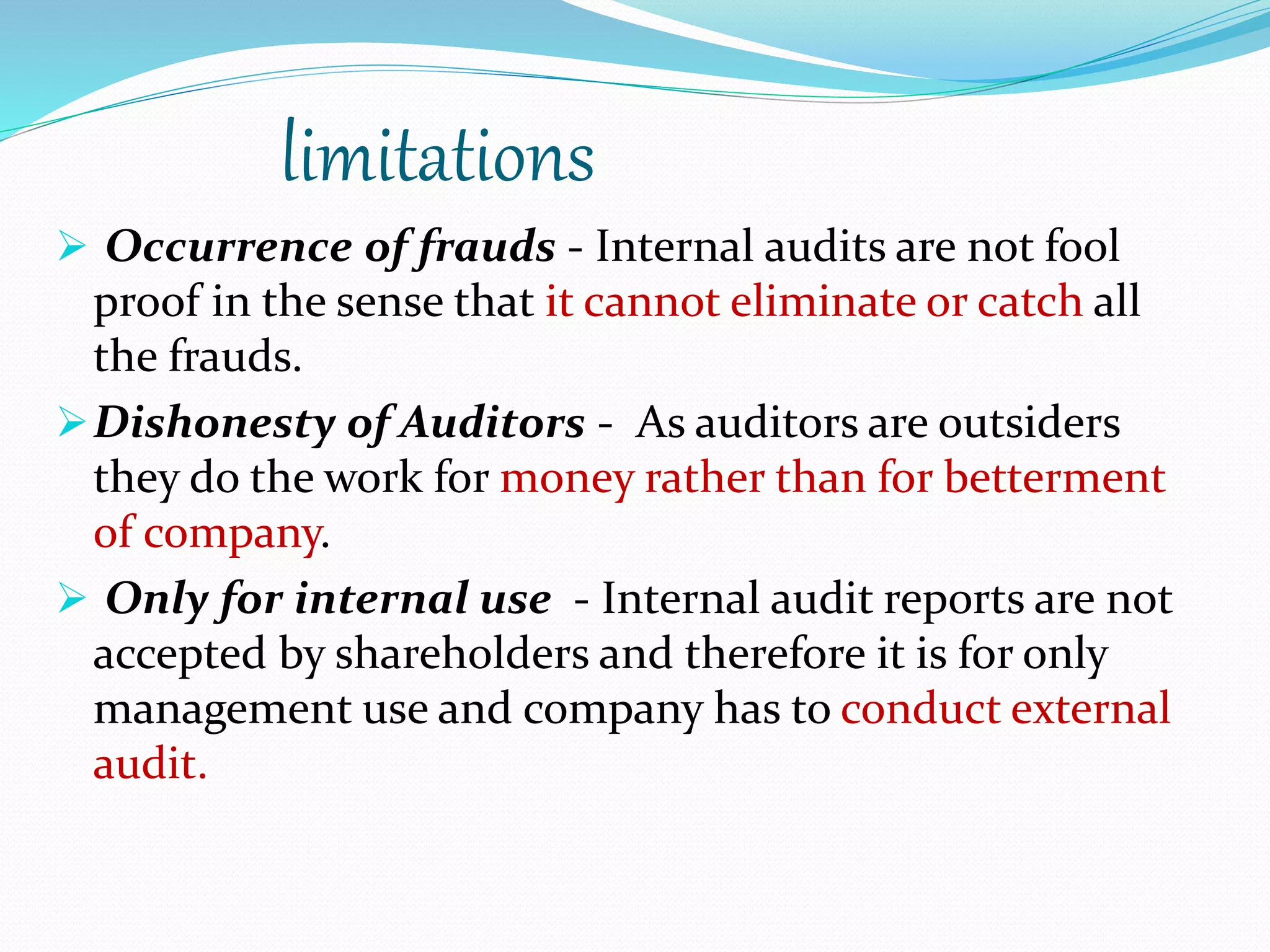

limitations

Occurrence offrauds - Internal audits are not fool

proof in the sense that it cannot eliminate or catch all

the frauds.

Dishonesty of Auditors - As auditors are outsiders

they do the work for money rather than for betterment

of company.

Only for internal use - Internal audit reports are not

accepted by shareholders and therefore it is for only

management use and company has to conduct external

audit.

23.

Difference between internalcheck

and internal control

BASIS INTERNAL CHECK INTERNAL CONTROL

Scope It has narrow scope It comprises of overall

system of control

Objectives Prevent occurrence of

errors and frauds

Ensure compliance of the

various policies and

procedures

Flexibility It is less flexible It is reviewed occasionally

24.

Difference between internalcheck

and internal audit

BASIS INTERNAL CHECK INTERNAL AUDIT

Meaning Arrangement of the

accounting work

It is a review of the

operations

Objective To minimize the

occurrences of errors

and frauds

It is easy detection of

errors and frauds

Nature Work is conducted on

continuous basis

It is post mortem on

work already done

Scope of work It is very limited It is comparatively wide

Involvement A large number of

employees are needed

A small number of

persons are needed

Need for separate staff There is no such

requirement

Separate set off staff is

required

25.

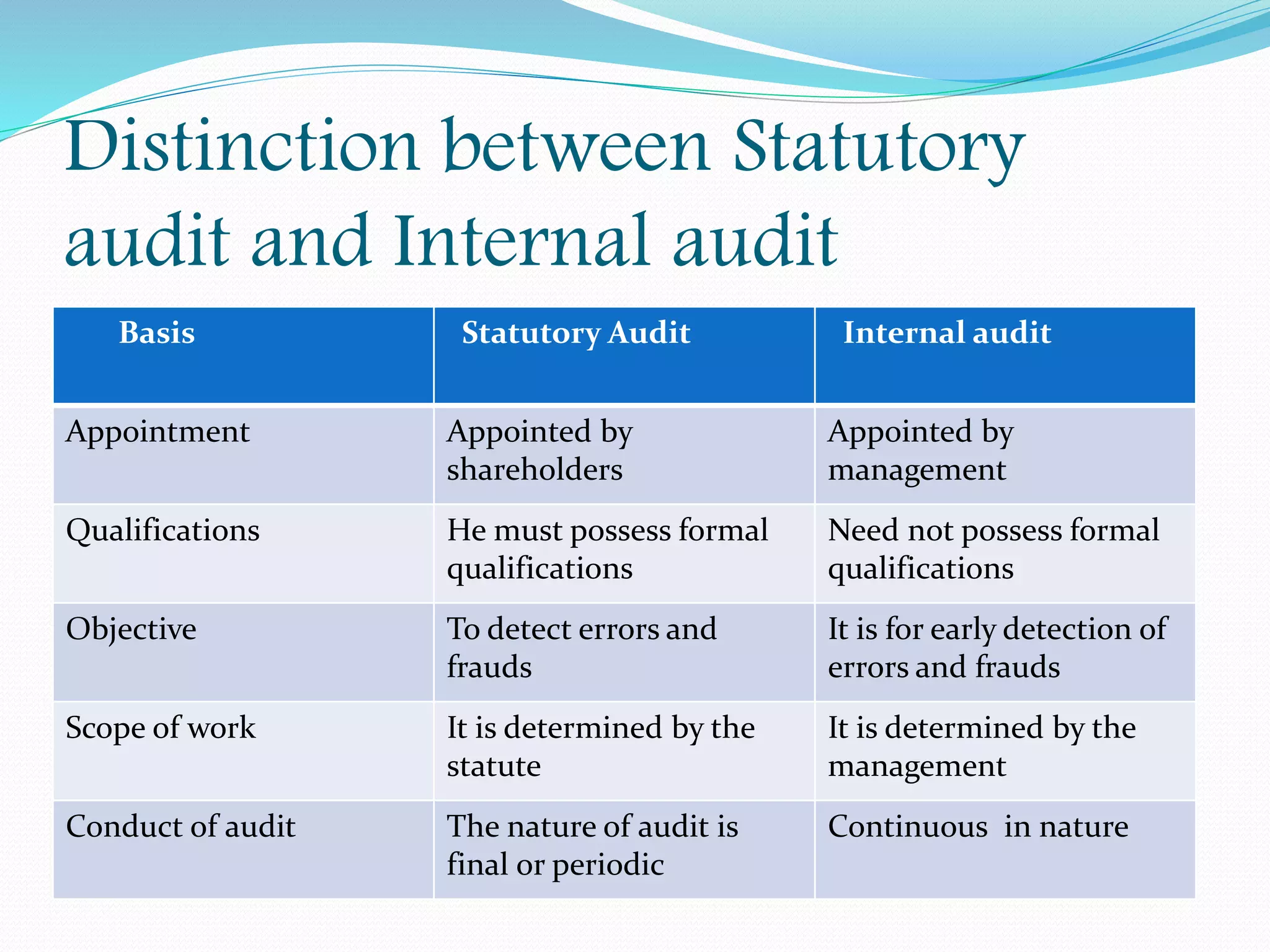

Distinction between Statutory

auditand Internal audit

Basis Statutory Audit Internal audit

Appointment Appointed by

shareholders

Appointed by

management

Qualifications He must possess formal

qualifications

Need not possess formal

qualifications

Objective To detect errors and

frauds

It is for early detection of

errors and frauds

Scope of work It is determined by the

statute

It is determined by the

management

Conduct of audit The nature of audit is

final or periodic

Continuous in nature

26.

Status Independent,

competent personwho

is an outsider

He is an employee of

the concern

Remuneration Fixed by the statute Fixed by the management

Reporting Report submission is

compulsory

It is not compulsory

Suggestions He may or may not give

suggestions

He can give suggestions

Application of Test

checks

Test checks can be

applied

He cannot apply test

checks

Attendance at meetings He has a right to attend He has no right to attend

Applications of

regulation act

Several regulations are

applicable for him

There are no such

regulations applicable

Satisfaction For the satisfaction of the

shareholders

For the satisfaction of the

management

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)