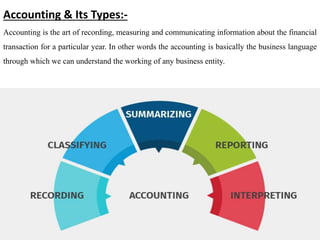

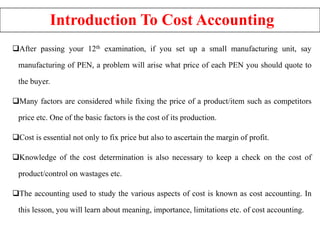

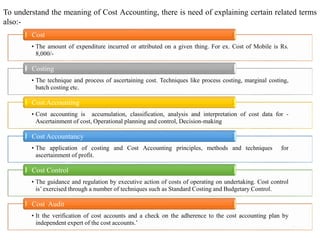

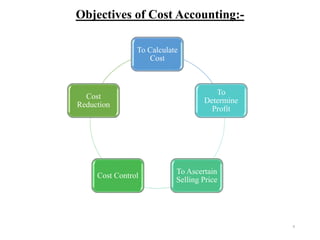

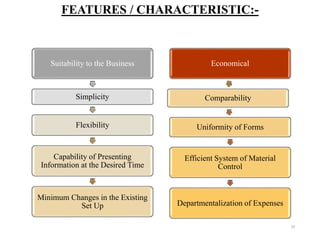

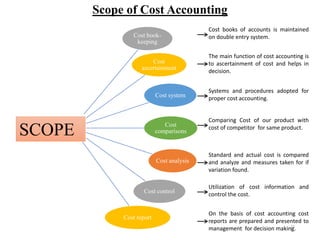

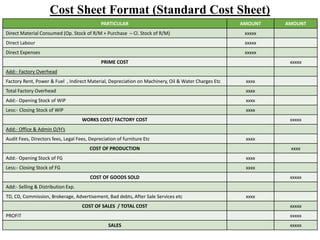

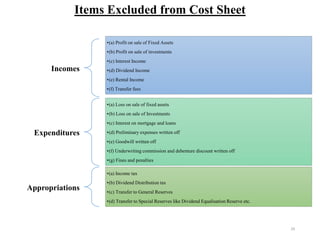

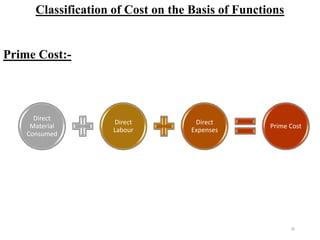

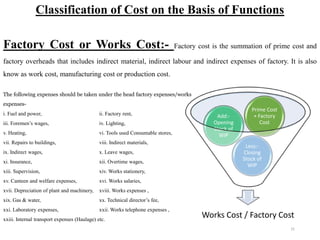

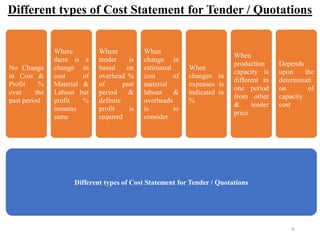

The document provides a comprehensive overview of cost accounting, highlighting its definition, importance, and limitations. It distinguishes between cost accounting, financial accounting, and management accounting, as well as detailing various cost classifications and concepts. Additionally, it examines the objectives of cost accounting, the preparation and significance of a cost sheet, and the considerations for tender quotations.