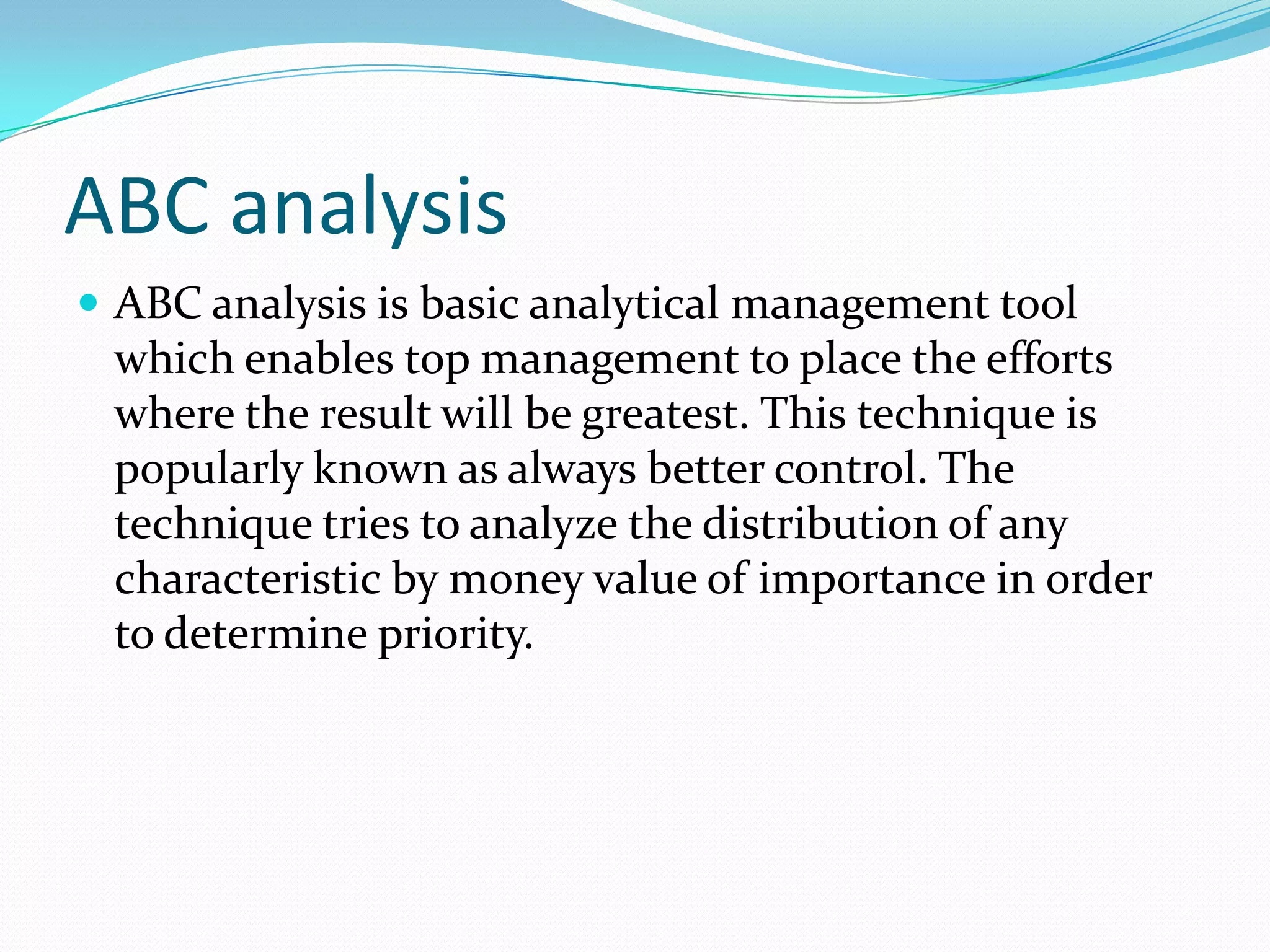

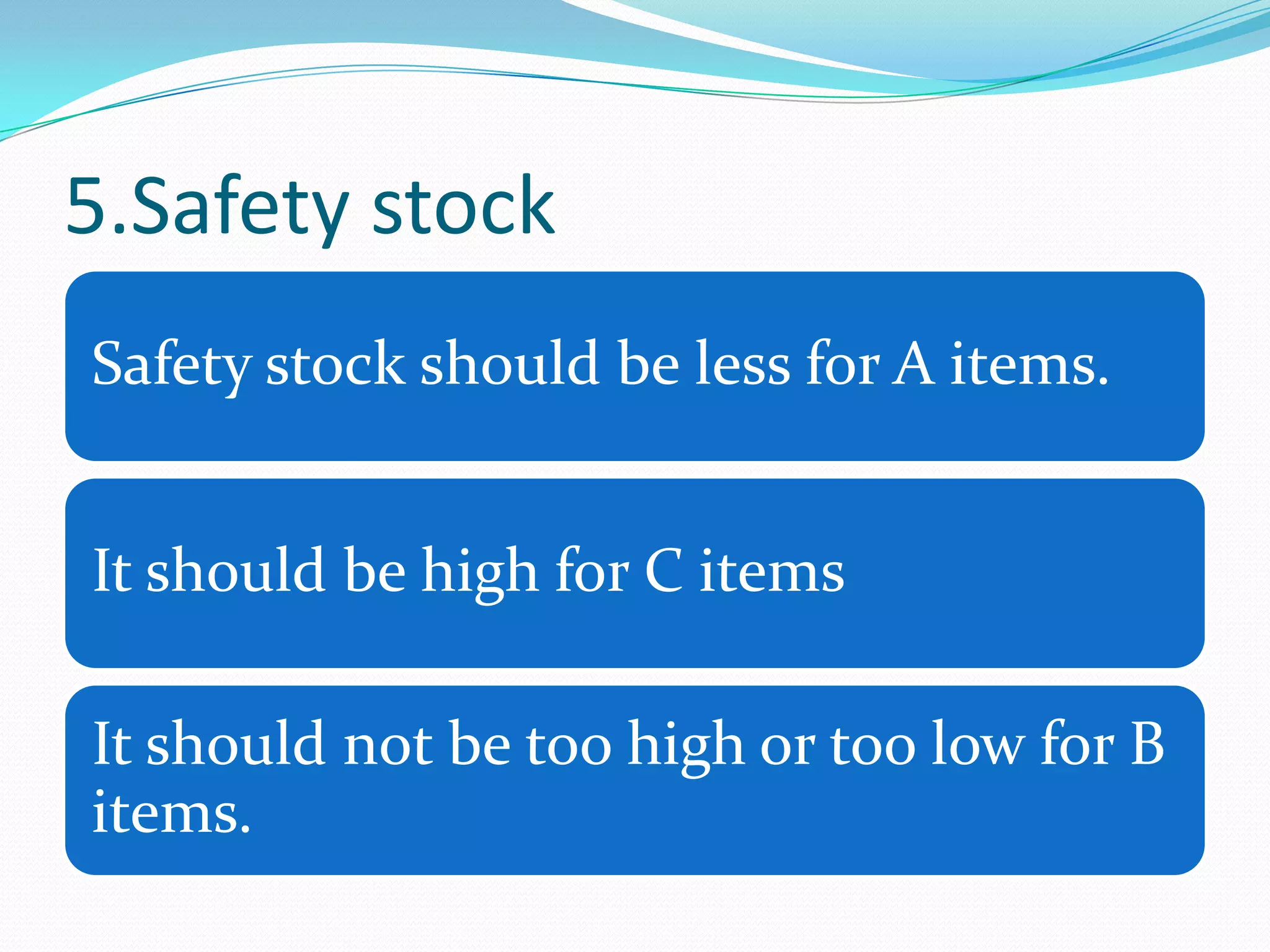

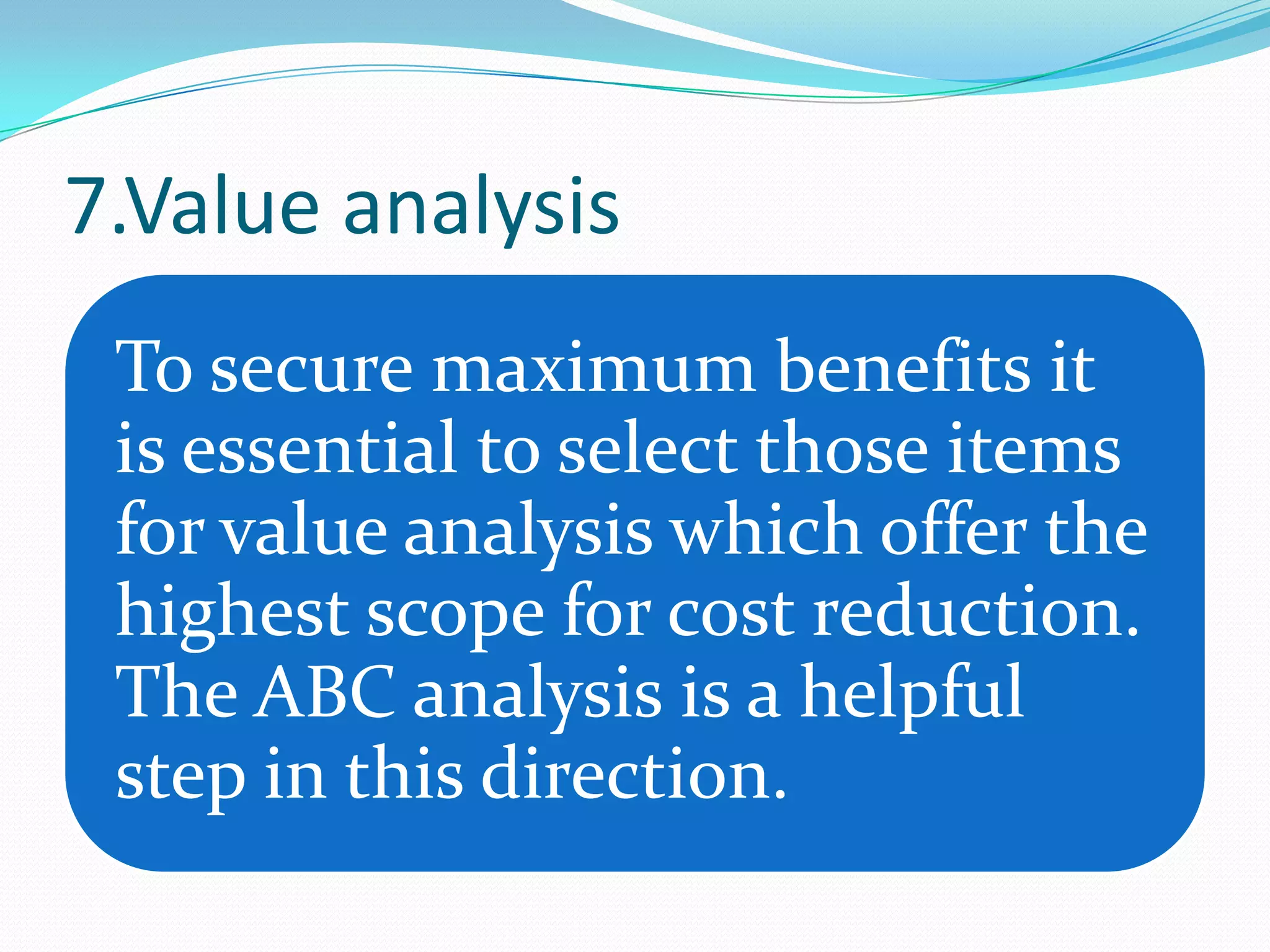

ABC analysis is a technique used to categorize inventory items into three categories - A, B and C - based on their annual usage value. Category A items have the highest value and make up around 10-20% of total items but account for around 70-80% of total usage value. Category C items are the opposite, making up 70-80% of total items but only around 10-20% of total usage value. Category B items fall in between. ABC analysis is used to prioritize inventory management efforts - strict controls are applied to A items while low controls can be used for C items. The analysis helps optimize resources by focusing on the most important items.