Downloaded 45 times

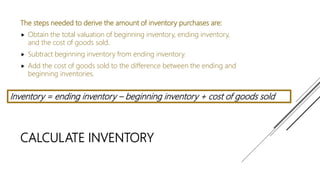

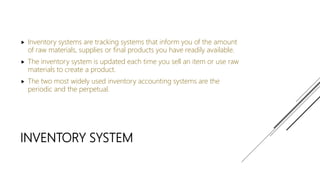

The document explains the importance of inventory valuation for businesses, outlining how inventory, considered a significant asset, must be accurately measured for proper financial reporting and decision-making. It describes two main inventory accounting systems—periodic and perpetual—each with its own method for tracking stock and calculating costs of goods sold. Various inventory valuation methods, including FIFO, LIFO, HIFO, and average cost, are also discussed, emphasizing the need for meticulous record-keeping to support revenue generation.