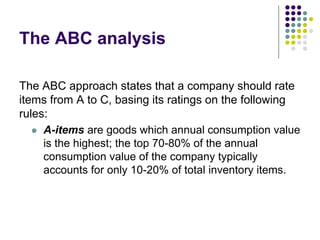

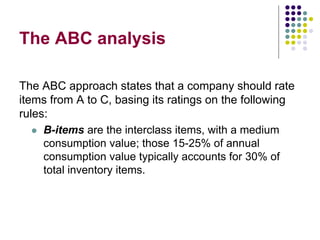

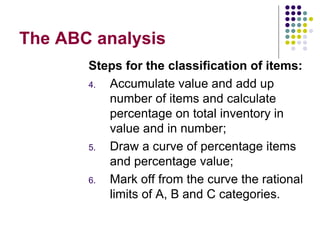

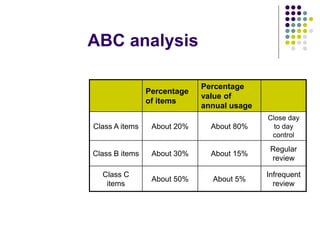

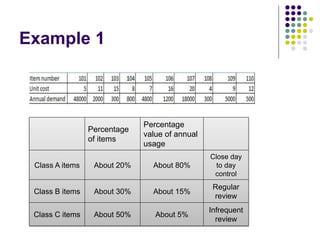

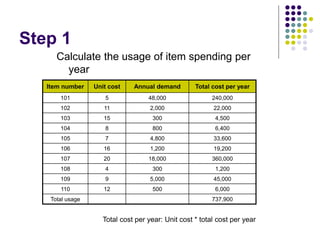

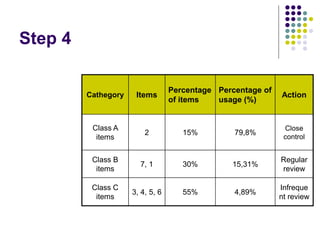

The document discusses ABC analysis, an inventory categorization method that divides items into categories A, B, and C based on their value to the company. Category A items are the most valuable, accounting for 10-20% of inventory items but 70-80% of total value. Category B items are of medium value, accounting for 15-25% of value with 30% of items. Category C items are the least valuable, accounting for 5% of value but 50% of items. The analysis aims to focus management attention on the critical few high-value items rather than the many low-value items.