Download to read offline

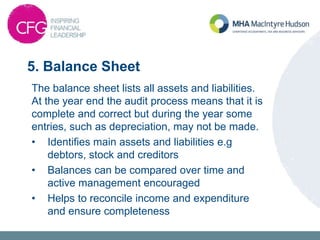

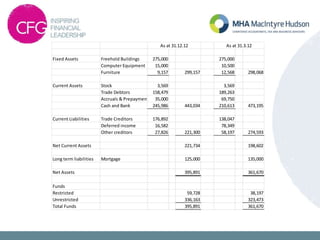

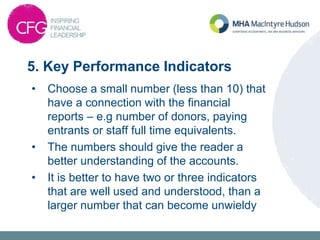

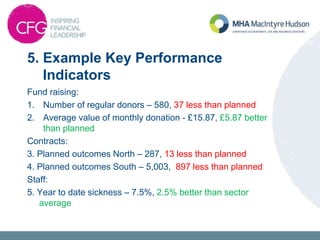

The document discusses improving financial management for charities through providing concise and timely financial reports. It recommends including budgets, actual spending, variances, forecasts, cashflow statements and key performance indicators in monthly or quarterly reports. Integrating financial and operational data helps ensure resources are applied effectively and that legal obligations are met. Good financial oversight can help strengthen donor confidence and achieve charitable goals.