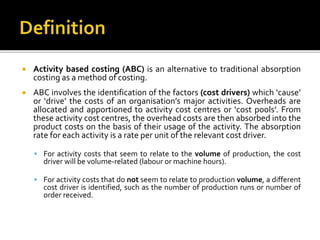

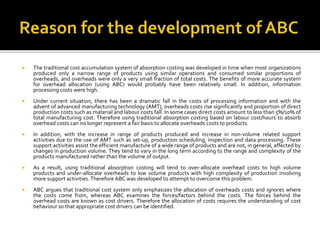

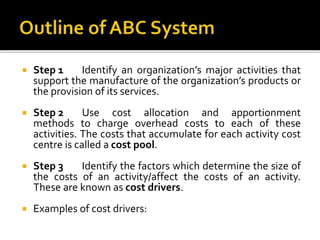

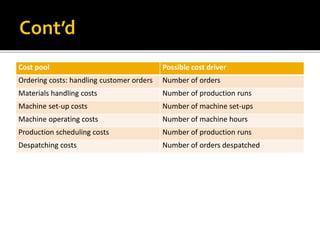

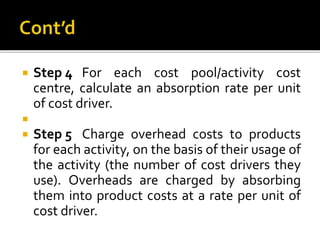

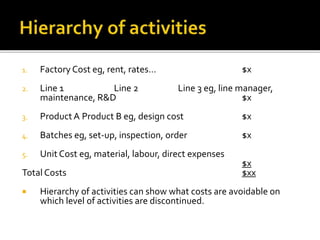

This document provides an overview of activity-based costing (ABC). It explains that ABC identifies cost drivers that cause overhead costs and allocates those costs to products based on their usage of activities. Traditional absorption costing allocated overhead based solely on direct costs like labor hours. ABC is more accurate when products have different levels of overhead usage and direct costs make up a small portion of total costs. The document outlines the steps of ABC, including identifying activities, assigning costs to cost pools, determining cost drivers, calculating absorption rates, and charging overhead to products.