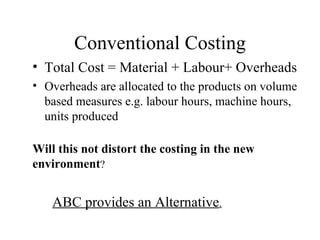

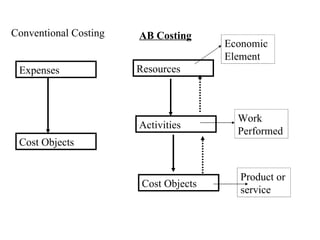

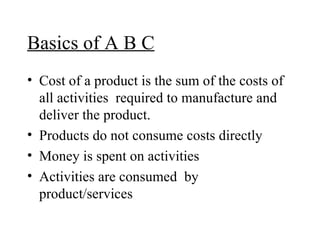

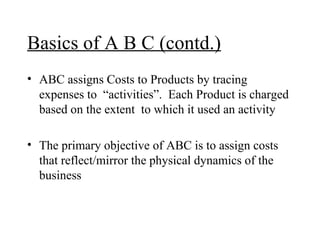

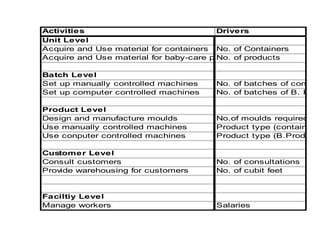

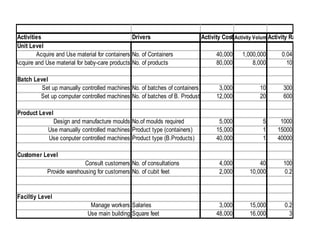

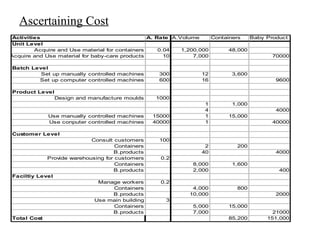

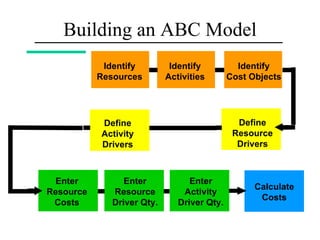

Activity Based Costing (ABC) is an alternative to conventional costing systems that allocates overhead costs to products based on their use of activities rather than volume-based measures. ABC assigns costs to products by tracing expenses to activities and then charging each product based on the extent to which it uses each activity. The primary objective of ABC is to assign costs in a way that reflects the physical dynamics of the business. ABC helps answer questions about what activities are performed, how much activities cost, why activities are needed, and how much of each activity is required for products, services, and customers.