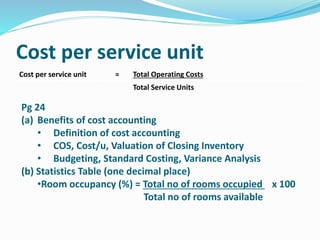

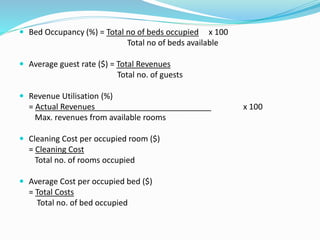

This document discusses cost accounting methods used in service industries. It defines cost accounting as a method used to calculate the cost per unit of service provided. It then lists several examples of service industries and service activities within businesses that would use cost accounting methods. Finally, it outlines some key terms and statistics used in cost accounting for the hotel service industry.