JOB ORDER COSTINGvs. PROCESS COSTING

Job order costing is a costing

method which is used to determine

the cost of manufacturing each

product. This costing method is

usually adopted when the

manufacturer produces a variety of

products which are different from

one another and needs to calculate

the cost for doing an individual job.

Job costing includes the direct labor,

direct materials, and manufacturing

overhead for that particular job.

Process costing is a way to

track production costs at each stage

of manufacturing. It’s ideal for

businesses that produce goods in

large volumes, like food, chemicals,

or electronics, where processes are

consistent and continuous. This

method allocates expenses for

materials, labor, and overhead

across production stages.

DEFINITION

3.

JOB ORDER COSTINGvs. PROCESS COSTING

Job order costing is a

system for determining the cost

of individual products, perhaps

within a larger manufacturing

job. It is an efficient way to

forecast actual expenses for

materials, labor, and overhead

before production. Armed with a

job cost, you can determine the

advisability of producing that

particular item.

Process costing ensures

clear tracking of costs, making it

easier for businesses to manage

production expenses. Analyzing

materials, labor, and overhead

provides essential insights for

controlling costs and maintaining

profitability.

IMPORTANCE

4.

JOB ORDER COSTING& PROCESS COSTING

• Both job and process cost systems have the same

goal: to determine the cost of products.

• Both job and process cost systems have the same

cost flows. Accountants record production in separate

accounts for materials inventory, labor, and overhead.

Then, they transfer the costs to a Work in Process

Inventory account.

• Both job and process cost systems use

predetermined overhead rates to apply overhead.

SIMILARITIES

5.

JOB ORDER COSTING& PROCESS COSTING

• Types of products produced.

• Cost accumulation procedures.

• Work in Process Inventory accounts.

DIFFERENCES

6.

JOB ORDER COSTING

1.Identifying the Job

2. Calculating the Costs

3. Choosing the Allocation Base

4. Receiving the Order

5. Maintaining Job Cost Sheets

6. Revising the Costs

HOW TO CALCULATE JOC?

7.

PROCESS COSTING

1. AnalyzingInventory

2. Calculating Equivalent Units

3. Determining Total Costs

4. Calculating Cost Per Unit

5. Allocating Costs for Completed and

Incomplete Products

STEPS IN PROCESS COSTING

8.

JOB ORDER COSTINGvs. PROCESS COSTING

ILLUSTRATION

HETOGENEOUS PRODUCT HOMOGENEOUS PRODUCT

ORDERS

(ONLY ONE WIP ACCOUNT)

PROCESS

(WIP ACCOUNTS FOR

EVERY SINGLE

DEPARTMENTS)

JOB COST SHEET PRODUCTION COST REPORT

Activity-based costing

(ABC) isa costing method that

assigns overhead and

indirect costs to related

products and services.

WHAT IS ACTIVITY-BASED

COSTING?

11.

Activity-based costing (ABC)is mostly used in the

manufacturing industry. It enhances the reliability of cost data,

hence producing nearly true costs and better classifying the

costs incurred by the company during its production process.

This costing system is used in target costing, product

costing, product line profitability analysis, customer profitability

analysis, and service pricing. Activity-based costing is used to get

a better grasp on costs, allowing companies to form a more

appropriate pricing strategy.

The formula for activity-based costing is the cost pool total

divided by the cost driver, which yields the cost driver rate. The

cost driver rate is used in activity-based costing to calculate the

amount of overhead and indirect costs related to a particular

activity.

How Activity-Based

Costing (ABC) Works?

12.

1. Identify allthe activities required to create the product.

2. Divide the activities into cost pools, which include all the

individual costs related to an activity. Calculate the total

overhead of each cost pool.

3. Assign each cost pool activity cost drivers, such as

hours or units.

4. Calculate the cost driver rate by dividing the total

overhead in each cost pool by the total cost drivers.

5. Multiply the cost driver rate by the number of cost

drivers.

The ABC calculation is

as follows:

13.

As an activity-basedcosting example, consider

Company ABC, which has a P50,000 per year electricity

bill. The number of labor hours has a direct impact on

the electric bill. For the year, there were 2,500 labor

hours worked; in this example, this is the cost driver.

Calculating the cost driver rate is done by dividing the

P50,000 a year electric bill by the 2,500 hours, yielding

a cost driver rate of P20. For Product XYZ, the company

uses electricity for 10 hours. The overhead costs for the

product are P200, or P20 times 10.

EXAMPLE

14.

The ABC systemof cost accounting is based on activities, which are any events, units

of work, or tasks with a specific goal—such as setting up machines for production,

designing products, distributing finished goods, or operating machines. Activities

consume overhead resources and are considered cost objects.

Under the ABC system, an activity can also be considered as any transaction or event

that is a cost driver. A cost driver, also known as an activity driver, is used to refer to an

allocation base. Examples of cost drivers include machine setups, maintenance

requests, consumed power, purchase orders, quality inspections, or production orders.

There are two categories of activity measures: transaction drivers, which involve

counting how many times an activity occurs, and duration drivers, which measure how

long an activity takes to complete.

Unlike traditional cost measurement systems that depend on volume count, such as

machine hours and/or direct labor hours, to allocate indirect or overhead costs to

products, the ABC system classifies five broad levels of activity that are, to a certain

extent, unrelated to how many units are produced. These levels include batch-level

activity, unit-level activity, customer-level activity, organization-sustaining activity, and

product-level activity.

Requirements for

Activity-Based Costing

(ABC)

15.

Activity-based costing (ABC)enhances the costing process in

three ways. First, it expands the number of cost pools that can be

used to assemble overhead costs. Instead of accumulating all costs

in one company-wide pool, it pools costs by activity.

Second, it creates new bases for assigning overhead costs to

items, so costs are allocated based on the activities that generate

costs, instead of on volume measures—such as machine hours or

direct labor costs.

Finally, ABC alters the nature of several indirect costs, making

costs previously considered indirect—such as depreciation,

utilities, or salaries—traceable to certain activities. Alternatively,

ABC transfers overhead costs from high-volume products to low-

volume products, raising the unit cost of low-volume products.

Benefits of Activity-

Based Costing (ABC)

16.

There are fivelevels of activity in ABC costing: unit-level activities, batch-

level activities, product-level activities, customer-level activities, and

organization-sustaining activities. Unit-level activities are performed each

time a unit is produced. (For example, providing power for a piece of equipment

is a unit-level cost.) Batch-level activities are performed each time a batch is

processed, regardless of the number of units in the batch. Coordinating

shipments to customers is an example of a batch-level activity.

Product-level activities are related to specific products; product-level

activities must be carried out regardless of how many units of product are

made and sold. (For example, designing a product is a product-level activity.)

Customer-level activities relate to specific customers. An example of a

customer-level activity is general technical product support. The final level of

activity, organization-sustaining activity, refers to activities that must be

completed regardless of the products being produced, how many batches are

run, or how many units are made.

What Are the Five Levels

of Activity in ABC

Costing?

17.

The goal ofABC costing is to

optimize business activities and

processes to enhance efficiency

and reduce costs. It seeks to

identify the highest cost drivers: the

activities and processes that

consume the most of a company's

resources.

What Does Activity-

Based Costing Seek to

Identify?

18.

ABC costing iscalculated by finding

the total cost pool and dividing it by the

cost driver. The cost pool is an aggregate

of all the costs associated with

performing a particular business task,

such as making a particular product.

Cost drivers are labor hours, machine

hours, and customer contacts.

How Do You Calculate

ABC Costing?

A variable costis an expense that

changes in proportion to how much a

company produces or sells. Variable

costs increase or decrease depending

on a company's production or sales

volume—they rise as production

increases and fall as production

decreases.

What Is a Variable Cost?

21.

Examples of variablecosts include a

manufacturing company's costs of raw

materials and packaging—or a retail

company's credit card transaction fees or

shipping expenses, which rise or fall with

sales. A variable cost can be contrasted with

a fixed cost. Aside from that, some other

variable costs are sales commissions, direct

labor costs, cost of raw materials used in

production, and utility costs.

ILLUSTRATION

23.

The total expensesincurred by any

business consist of variable and fixed costs.

Variable costs are dependent on production

output or sales. The variable cost of

production is a constant amount per unit

produced. As the volume of production and

output increases, variable costs will also

increase. Conversely, when fewer products

are produced, the variable costs associated

with production will consequently decrease.

Understanding Variable

Costs

24.

The total variablecost is simply the quantity of

output multiplied by the variable cost per unit of output:

Total Variable Cost = Total Quantity of Output x Variable

Cost Per Unit of Output

The variable cost per unit will vary across profits.

In general, it can often be specifically calculated as the

sum of the types of variable costs discussed below.

Variable costs may need to be allocated across goods if

they are incurred in batches (i.e. 100 pounds of raw

materials are purchased to manufacture 10,000

finished goods).

Formula and Calculation

of Variable Costs

25.

Along the manufacturingprocess,

there are specific items that are usually

variable costs. For the examples of these

variable costs below, consider the

manufacturing and distribution

processes for a major athletic apparel

producer.

Types of Variable Costs

26.

Raw materials arethe direct goods

purchased that are eventually turned into a

final product. If the athletic brand doesn't

make the shoes, it won't incur the cost of

leather, synthetic mesh, canvas, or other raw

materials. In general, a company should

spend roughly the same amount on raw

materials for every unit produced assuming

no major differences in manufacturing one

unit versus another.

Raw Materials

27.

Direct labor willalso vary depending on the units

produced. For example, if no units are produced, there will

be no direct labor cost. The more units produced, the more

need for direct labor costs. Some labor costs, however, will

still be required even if no units are produced. Certain

positions may be salaried whether output is 100,000 units

or 0 units, such as an accountant or lawyer of the firm.

These employees will receive the same amount of

compensation regardless of the number of units produced.

For others who are tied to an hourly job, putting in more

direct labor hours results in a higher paycheck.

Direct Labor

28.

Commissions are oftena percentage of a

sale's proceeds that are awarded to a company

as additional compensation. If no sales are

executed, there is no commission expense.

Because commissions rise and fall in line with

whatever underlying qualification the

salesperson must hit, the expense varies (i.e. is

variable) with different activity levels.

Commissions

29.

When the manufacturingline turns on

equipment and ramps up production, it begins to

consume energy. When it's time to wrap up

production and shut everything down, utilities

are often no longer consumed. In this example,

utilities usually vary with production. As a

company strives to produce more output, it is

likely this additional effort will require

additional power or energy, resulting in

increased variable utility costs.

Utilities

30.

The cost topackage or ship a product will

only occur if a certain activity is performed.

Therefore, the cost of shipping a finished good

varies (i.e. is variable) depending on the

quantity of units shipped. Though there may be

fixed cost components to shipping (i.e. an in-

house mail distribution network with a

personalized weighing and packaging product

line), many of the ancillary costs are variable.

Shipping/Freight

31.

• Variable costingdata can be used in a variety of ways to

analyze expenses, pricing, and profitability. Variable cost analysis is

important for the following reasons:

• Variable costs help determine pricing. A company usually

strives to competitively price its goods to recover the cost of

manufacturing the goods. By performing variable cost analysis, a

company will better grasp the inputs for its products and what it

needs to collect in revenue per unit to make sure it is earning money.

• Variable costs are an integral part of budgeting and planning. A

company may plan to double its output next year in an attempt to

scale revenue. To do so, it must be aware that variable costs will also

proportionally increase. Any strategic plans relating to growth,

contraction, or expansion to new products will likely incur changes to

variable costs.

Importance of

Variable Cost

Analysis

32.

• Variable costsdetermine the break-even point. A company's break-even

point is calculated as fixed costs divided by contribution margin, and

contribution margin is calculated as revenue - variable costs. A company can

leverage variable cost analysis to calculate exactly how many items it needs

to see to break even as well as how many units it needs to sell to make a

specific amount of money.

• Variable costs determine margins and net income. Gross margin, profit

margin, and net income calculations are often calculated with a combination

of fixed and variable costs. By performing variable cost analysis, a company

can easily identify how scaling or decreasing output can impact profit

calculations.

• Variable costs impact a company's expense structure. Imagine a

company that wants to rent a piece of equipment. It can choose between

paying $1,000 (fixed cost) or $0.05 for every item manufactured. This decision

will have a direct impact on the profitability and earning potential of a

company since a company's expense structure determines its leverage.

33.

Variable cost andaverage variable cost

may sound similar, but each describes an

entirely different value of expenses. While

variable cost is usually used to describe the

variable cost for a single product, average

variable cost often analyzes production over

time and compares variable costs to what

has been produced.

Variable Cost vs.

Average Variable Cost

34.

1. Average VariableCost =

Total Variable Costs / Total

Output

2. Variable Costs vs. Fixed

Costs

The average variable

can be calculated as:

35.

In general, companieswith a

high proportion of variable costs

relative to fixed costs are

considered to be less volatile, as

their profits are more dependent

on the success of their sales.

Note

Variable costs area direct input in the

calculation of contribution margin, the amount of

proceeds a company collects after using sale

proceeds to cover variable costs. Every dollar of

contribution margin goes directly to paying for fixed

costs; once all fixed costs have been paid for, every

dollar of contribution margin contributes to profit.

For this reason, variable costs are a required

item for companies trying to determine their break-

even point. In addition, variable costs are necessary

to determine sale targets for a specific profit target.

Contribution Margin

38.

EXAMPLE OF VARIABLE

COST

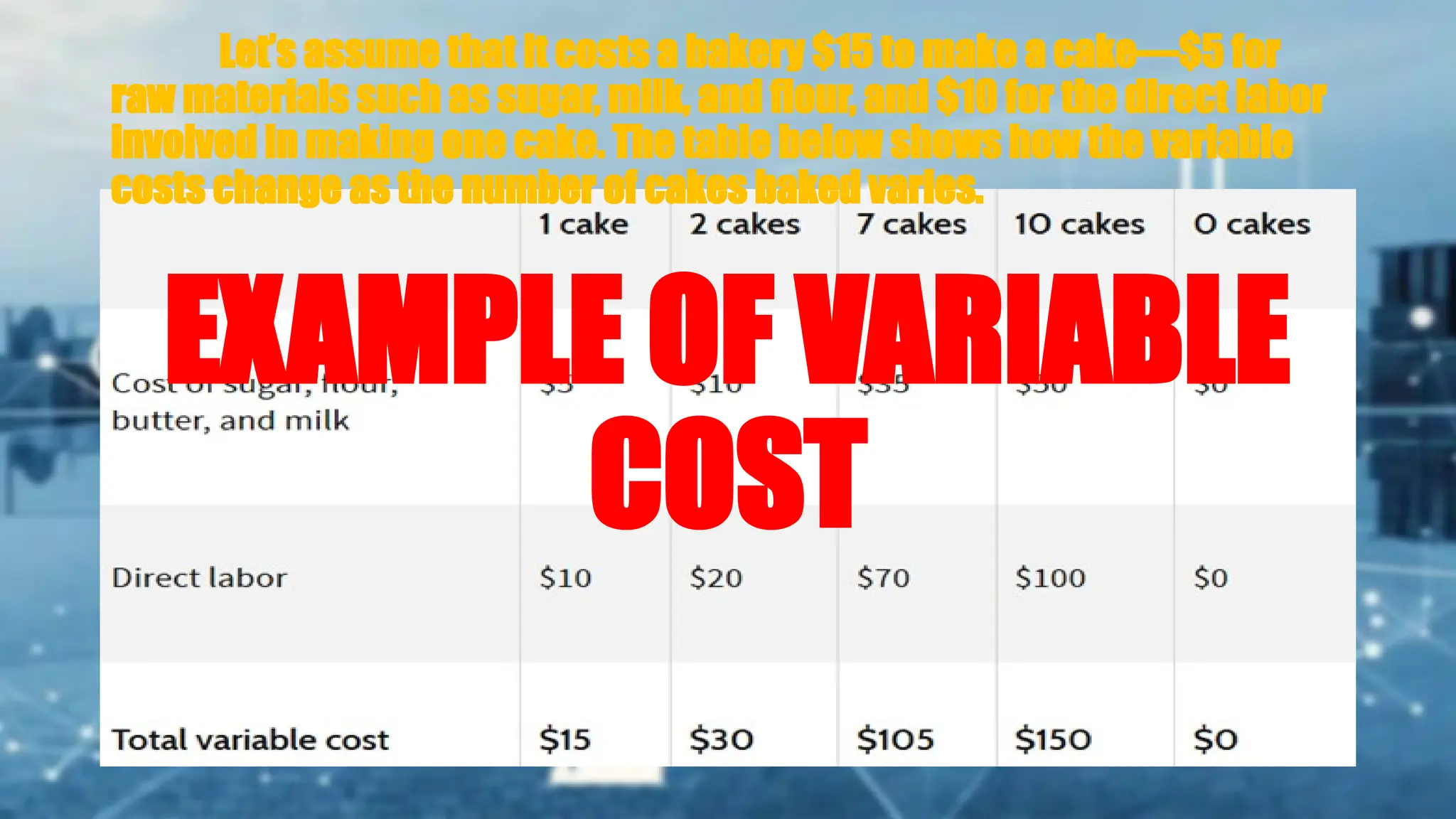

Let’sassume that it costs a bakery $15 to make a cake—$5 for

raw materials such as sugar, milk, and flour, and $10 for the direct labor

involved in making one cake. The table below shows how the variable

costs change as the number of cakes baked varies.

39.

As the productionoutput of cakes increases, the bakery’s

variable costs also increase. When the bakery does not make

any cake, its variable costs drop to zero.

Fixed costs and variable costs comprise the total cost.

Total cost is a determinant of a company’s profits, which is

calculated as:

Profits=Sales−Total Costs Profits=Sales−Total Costs

A company can increase its profits by decreasing its total

costs. Since fixed costs are more challenging to bring down

(for example, reducing rent may entail the company moving to

a cheaper location), most businesses seek to reduce their

variable costs. Decreasing costs usually means decreasing

variable costs.

40.

If the bakerysells each cake for $35, its gross profit per cake will be $35 -

$15 = $20. To calculate the net profit, the fixed costs have to be subtracted from

the gross profit. Assuming the bakery incurs monthly fixed costs of $900, which

includes utilities, rent, and insurance, its monthly profit will look like this:

41.

A business incursa loss when fixed costs are higher than

gross profits. In the bakery’s case, it has gross profits of $700 -

$300 = $400 when it sells only 20 cakes a month. Since its fixed

cost of $900 is higher than $400, it would lose $500 in sales. The

break-even point occurs when fixed costs equal the gross margin,

resulting in no profits or losses. In this case, when the bakery sells

45 cakes for a total variable cost of $675, it breaks even.

A company that seeks to increase its profit by decreasing

variable costs may need to cut down on fluctuating costs for raw

materials, direct labor, and advertising. However, the cost cut

should not affect product or service quality as this would have an

adverse effect on sales. By reducing its variable costs, a business

increases its gross profit margin or contribution margin.

42.

The contribution marginallows management to

determine how much revenue and profit can be earned from

each unit of product sold. The contribution margin is

calculated as:

The contribution margin for the bakery is ($35 - $15) / $35 =

0.5714, or 57.14%. If the bakery reduces its variable costs to $10, its

contribution margin will increase to ($35 - $10) / $35 = 71.43%.

Profits increase when the contribution margin increases. If the

bakery reduces its variable cost by $5, it would earn $0.71 for every

dollar in sales.

43.

Common examples ofvariable costs

include costs of goods sold (COGS; Cost of

Goods Sold; include raw materials, direct

labor, and manufacturing overhead costs,

and certain utilities (for example, electricity

or gas costs that increase with production

capacity).

What Are Some Examples of

Variable Costs?

44.

Variable costs aredirectly related to the cost of

production of goods or services, while fixed costs do

not vary with the level of production. Variable costs

are commonly designated as COGS, whereas fixed

costs are not usually included in COGS. Fluctuations

in sales and production levels can affect variable

costs if factors such as sales commissions are

included in per-unit production costs. Meanwhile,

fixed costs must still be paid even if production slows

down significantly.

How Do Fixed Costs Differ

from Variable Costs?

45.

If companies rampup production to meet

demand, their variable costs will increase as well. If

these costs increase at a rate that exceeds the

profits generated from new units produced, it may

not make sense to expand. A company in such a case

will need to evaluate why it cannot achieve

economies of scale. In economies of scale, variable

costs as a percentage of overall cost per unit

decrease as the scale of production ramps up.

How Can Variable Costs

Impact Growth and

Profitability?