Downloaded 1,570 times

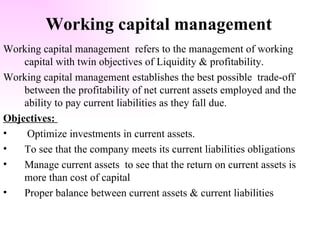

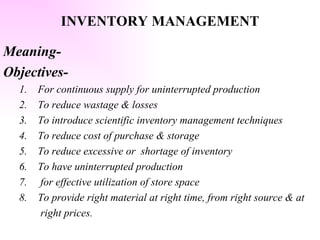

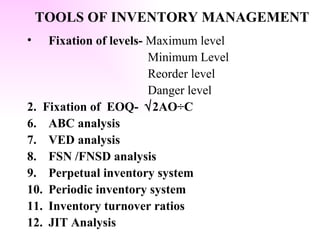

Working capital management refers to managing current assets and current liabilities to balance liquidity and profitability. It involves inventory management, cash management, and receivables management. Inventory management techniques include determining optimum inventory levels and economic order quantities. Cash management strategies include cash planning, managing cash flows, determining the optimum cash balance, and investing idle cash. Receivables management includes establishing credit policies, executing collection policies, and using tools like credit ratings and aging schedules.