Download to read offline

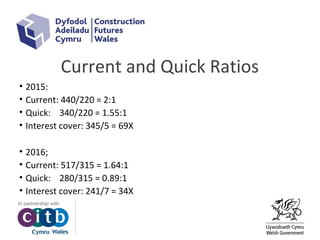

This document discusses the importance of managing cash flow and working capital for businesses. It provides guidance on developing cash flow forecasts and budgets. Key points include: - Cash flow and profit can differ, so cash flow forecasts are essential to evaluate a business's liquidity. - Working capital management, which involves managing inventory levels, accounts receivable, and accounts payable, is important to ensure sufficient cash flow. - Cash flow forecasts, along with balance sheets and income statements, allow businesses to anticipate liquidity needs and plan accordingly. - Metrics like current and quick ratios can help evaluate a business's vulnerability from a cash flow perspective.