Downloaded 175 times

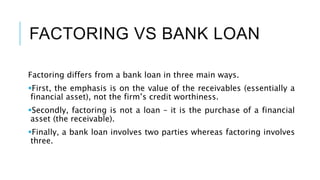

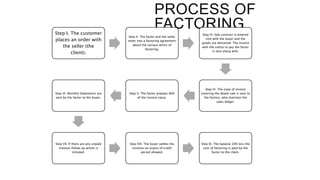

Factoring is a financial transaction where businesses sell their accounts receivable to a third party for immediate cash, distinctly differing from traditional bank loans by focusing on receivables' value rather than the firm's creditworthiness. The process includes several functions such as credit evaluation, debt collection, and risk assumption, along with benefits like improved liquidity and reduced debts, although it poses risks like over-dependence and unsuitability for small firms. In India, the factoring market is growing slowly due to challenges including lack of credit appraisal systems and high costs associated with debt assignments.