Downloaded 590 times

The document is a presentation by Dr. Sanjay P. Sawant Dessai on vouching and verification in financial audits, specifically designed for B.Com students. It covers various components of auditing, including the objectives and procedures of vouching, verification of assets and liabilities, and methods of inventory valuation. Additionally, the presentation discusses internal controls, the auditor's responsibilities, and highlights essential audit procedures with examples of common errors and verification techniques.

Presentation on Vouching and Verification in financial audits for B Com students by Dr. Sanjay P Sawant Dessai.Key contents on vouching, verification, and valuation including objectives and types.

Differences between cash and mercantile accounting, expenses vs payment, profit/loss vs receipt/payment account.

Vouching defined as examination of documentary evidence supporting transactions.

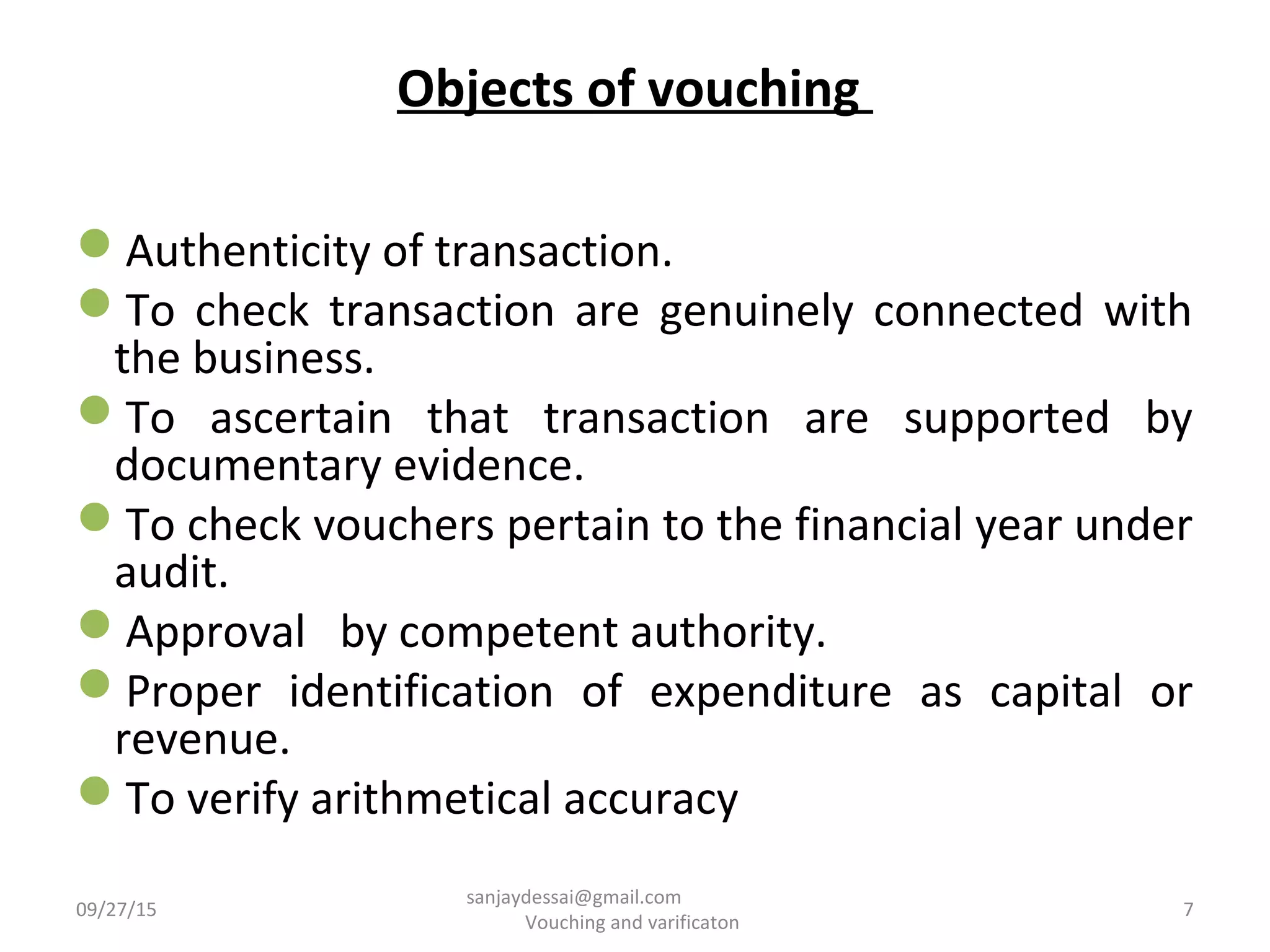

Key objectives include ensuring authenticity, connection to business, documentary support, and checking for accuracy.

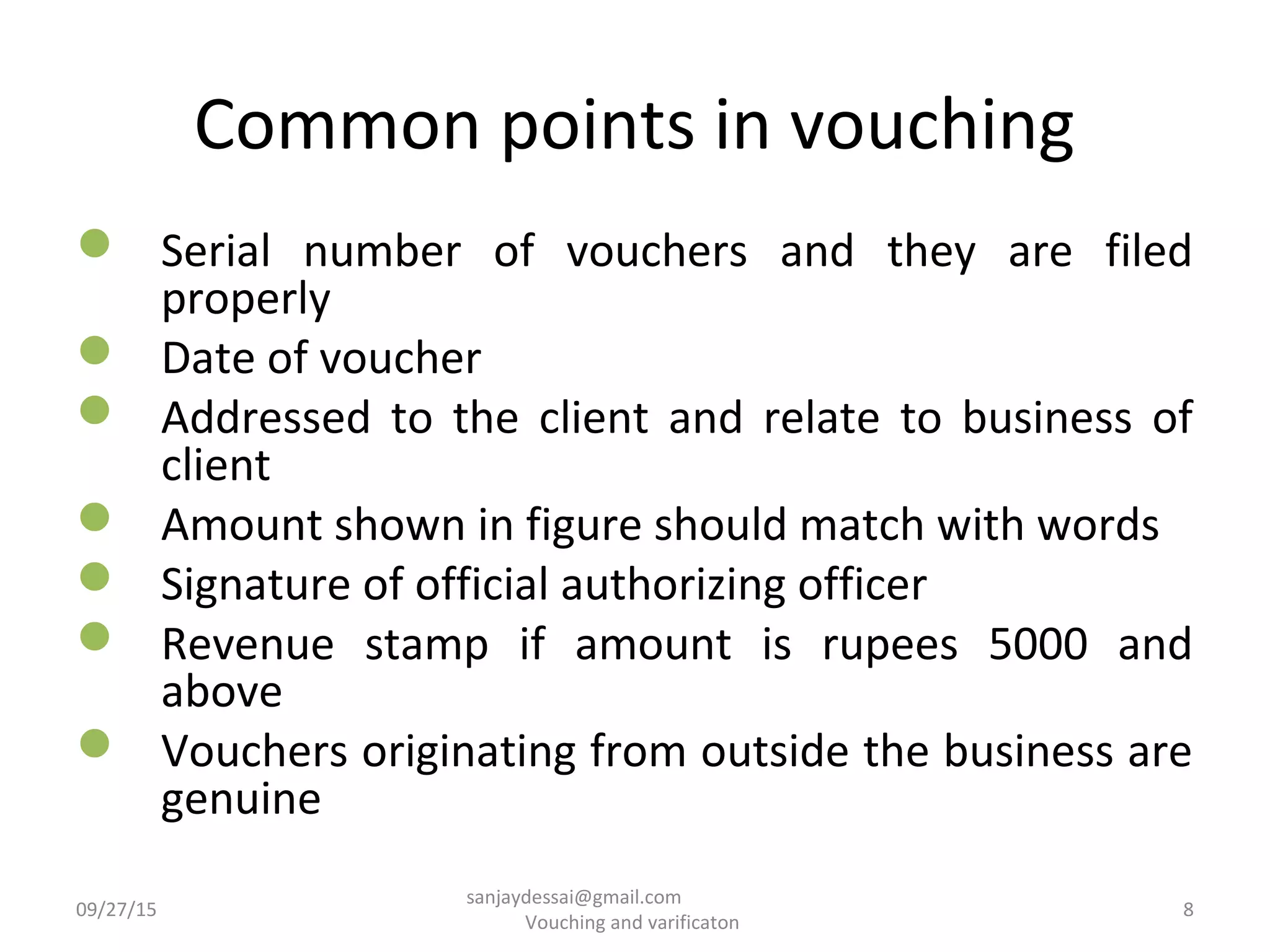

Essential criteria in vouching like voucher serials, signatures, and verification procedures.

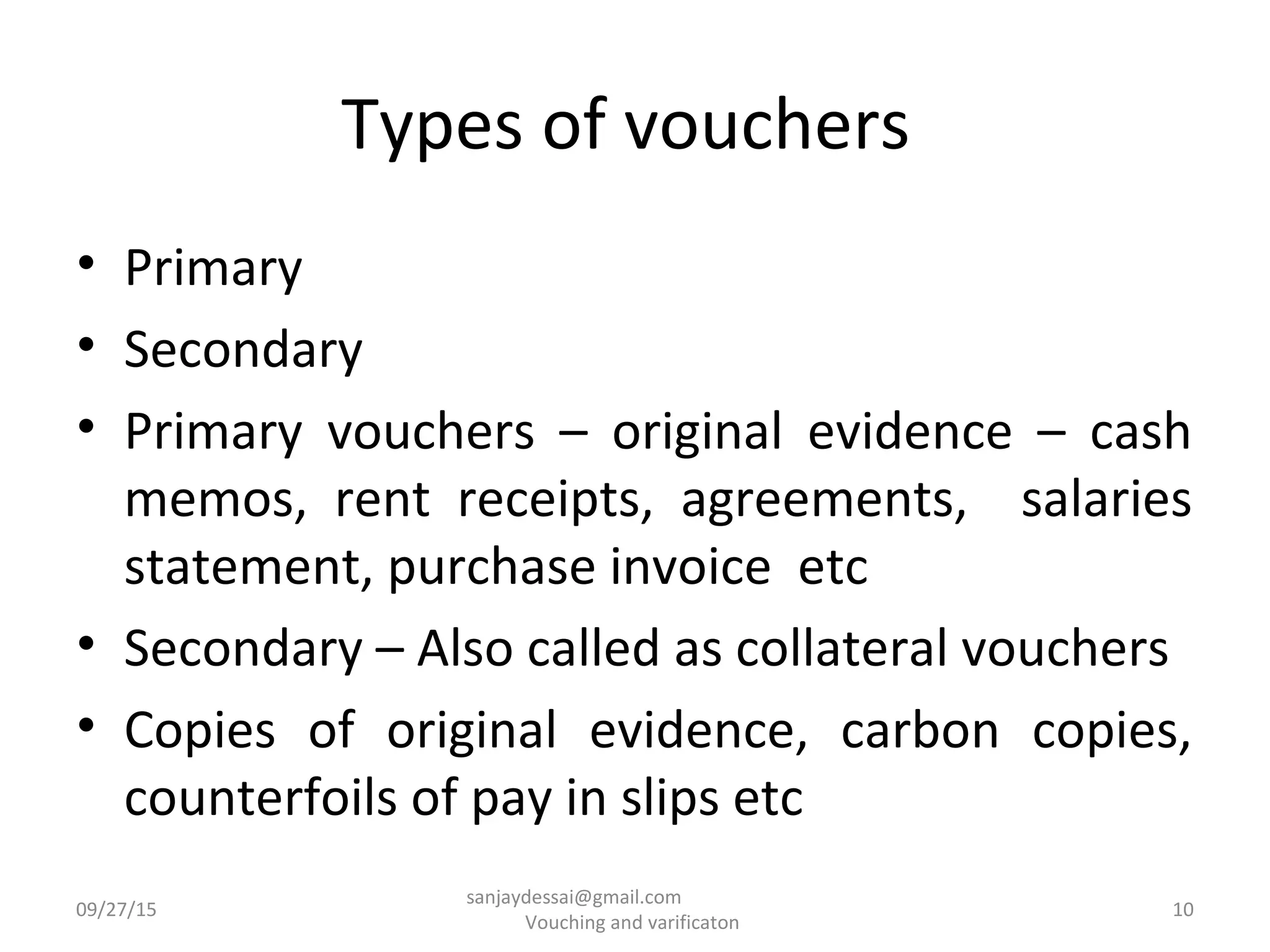

Different types of vouchers including primary (original evidence) and secondary (collateral evidence).

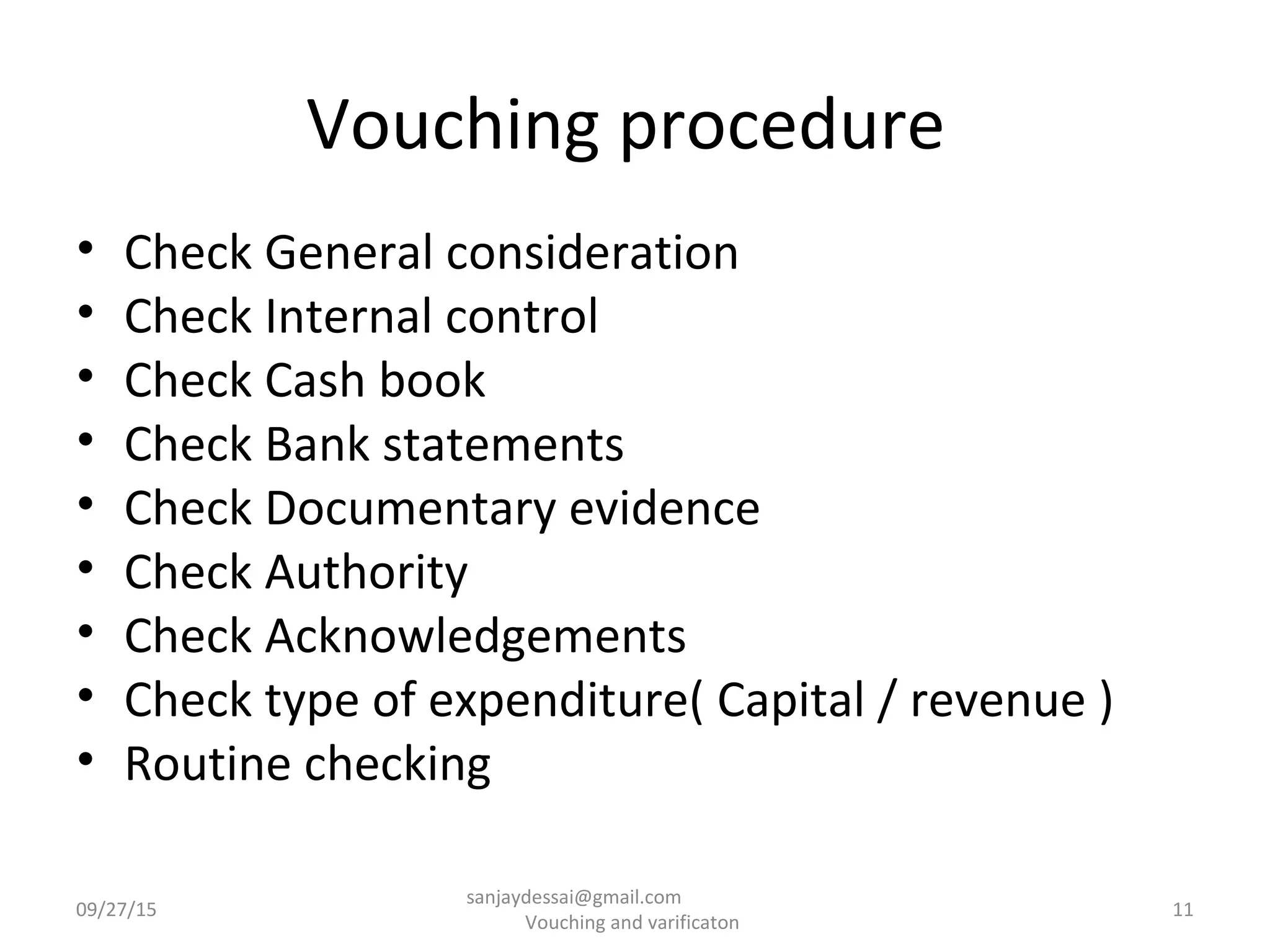

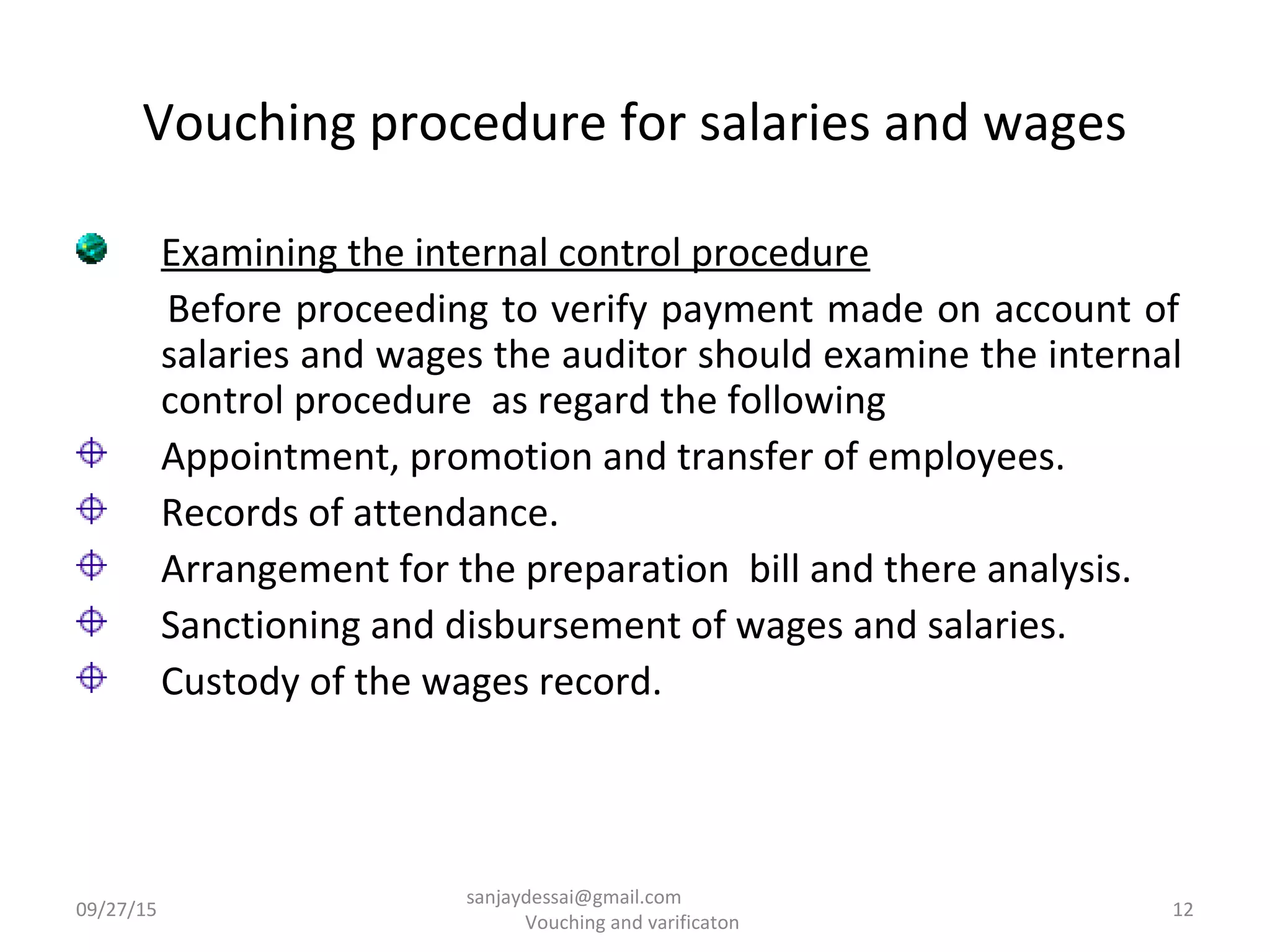

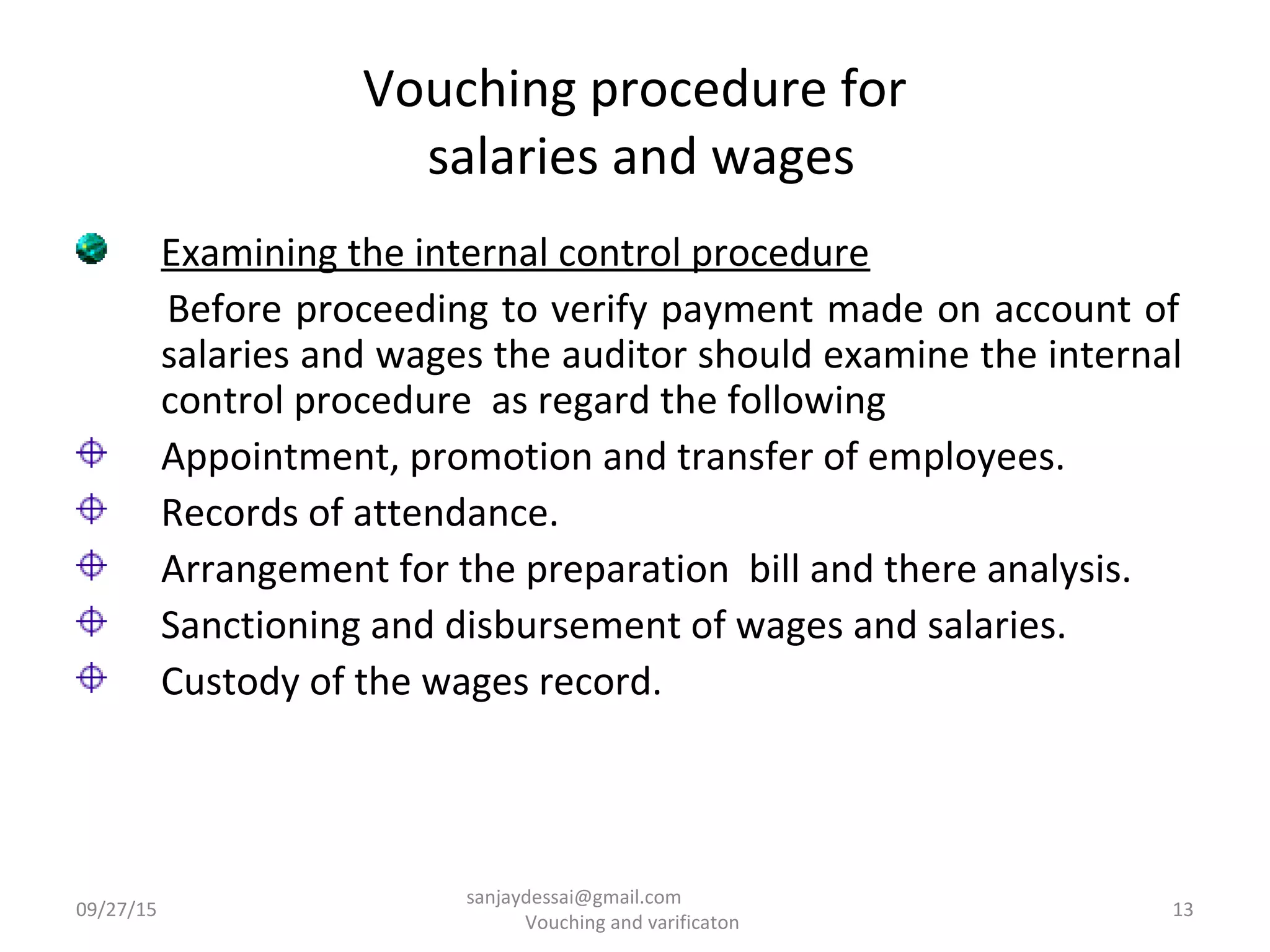

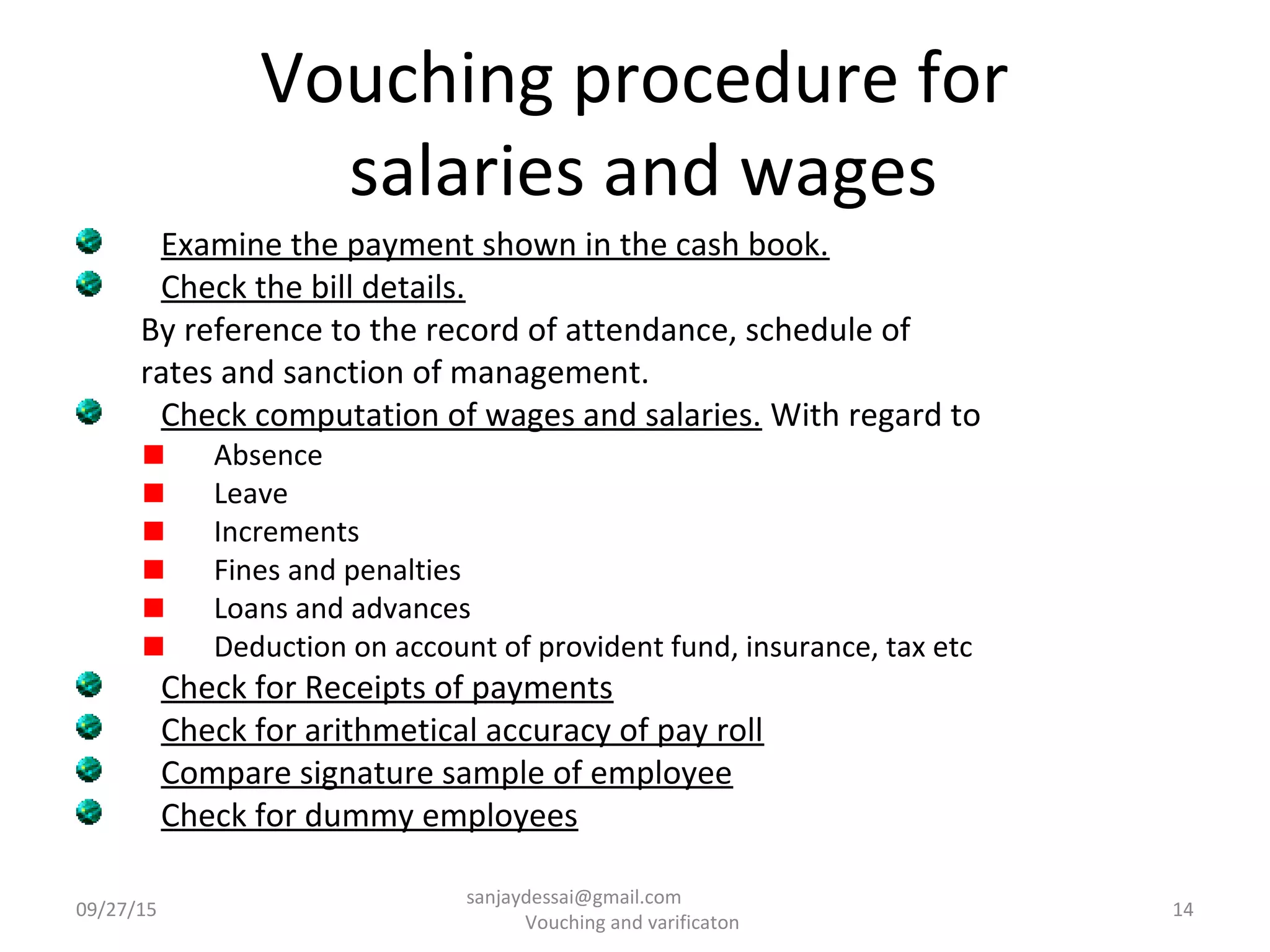

Vouching procedures including examining internal control, salary processing, and verifying payments.

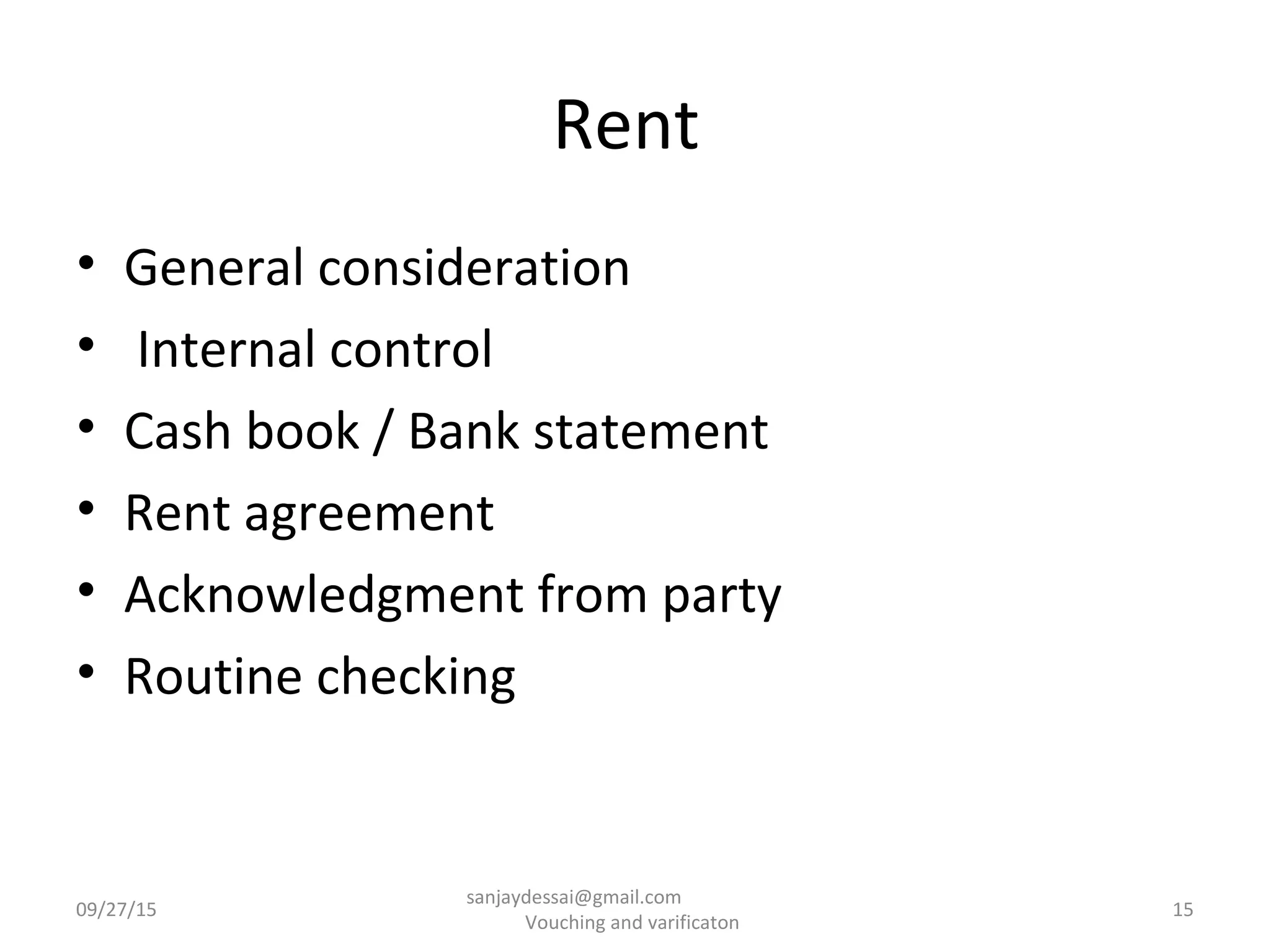

Considerations for rent verification, including internal control and documentation.

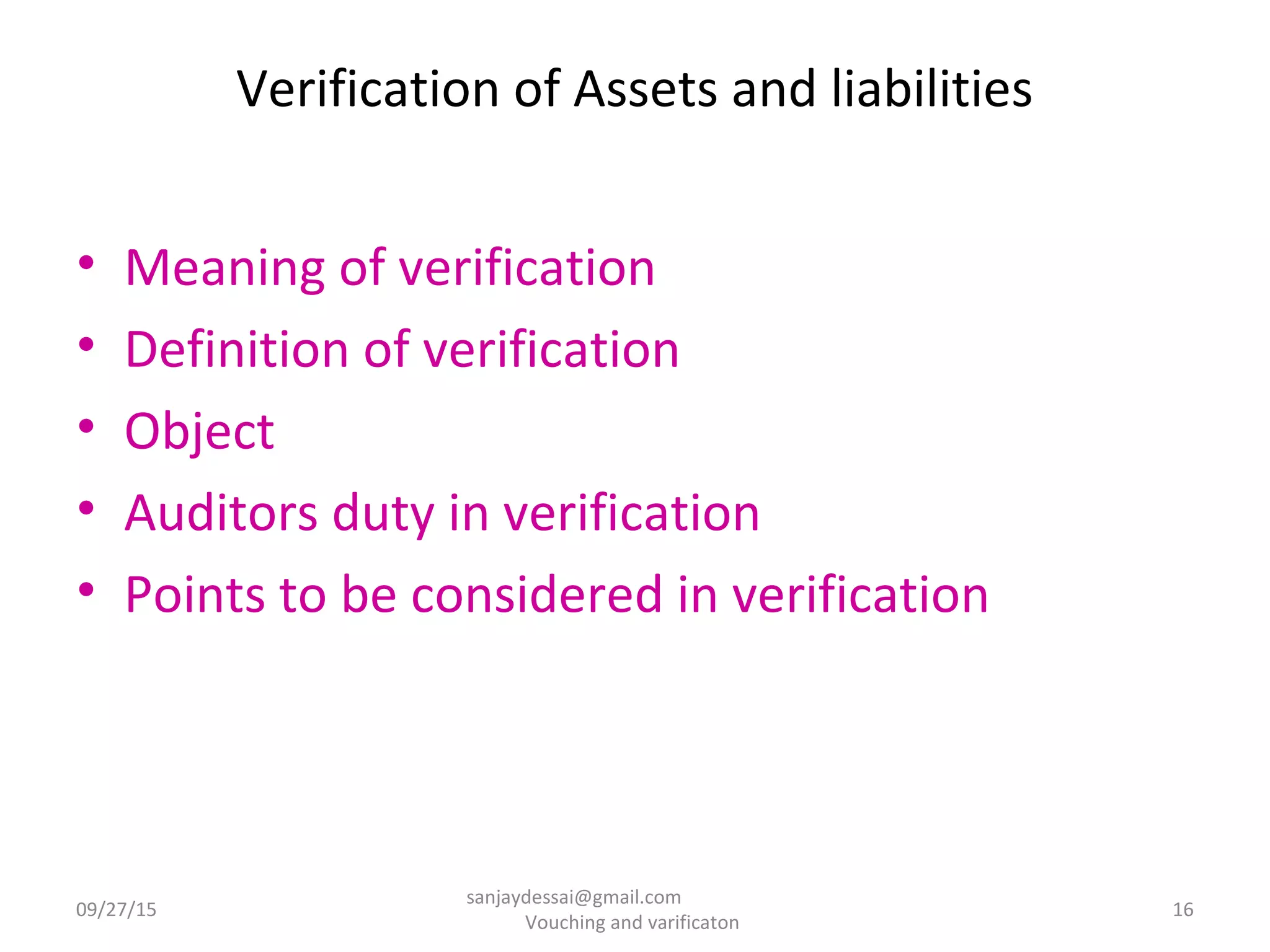

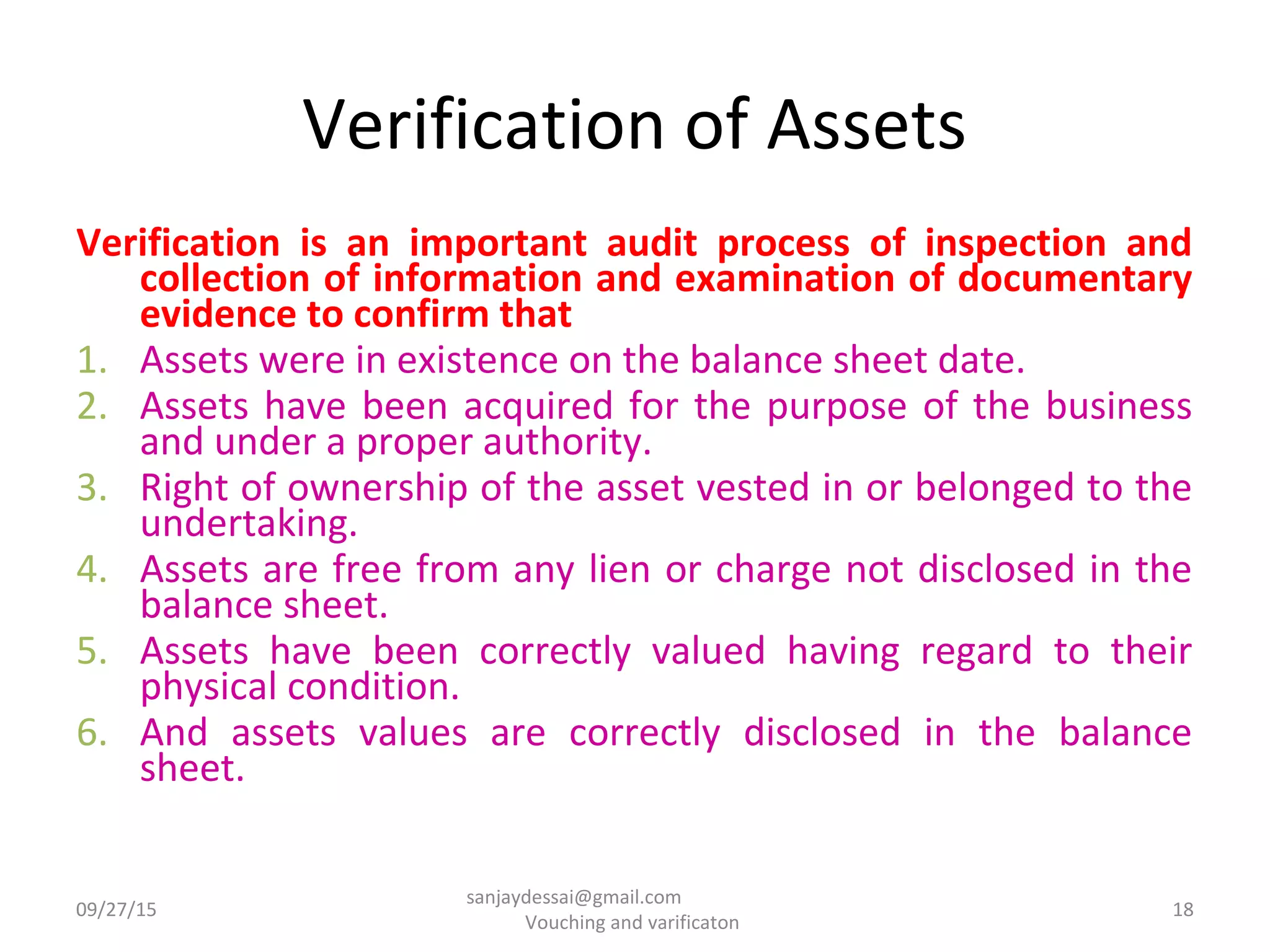

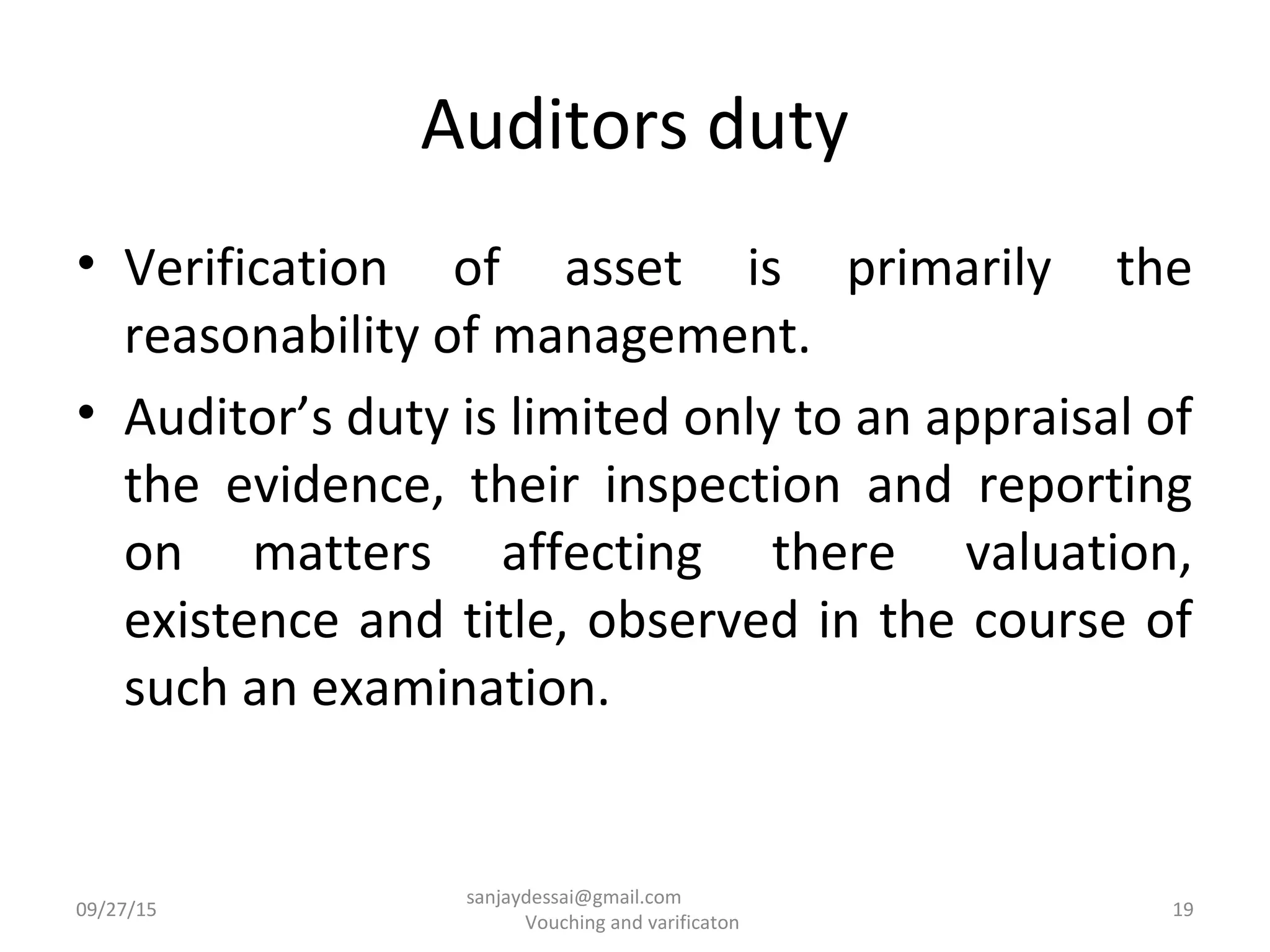

Meaning of verification, auditor duties, and definition including asset value inquiry.

Verification steps for assessing asset existence, acquisition, and proper ownership.

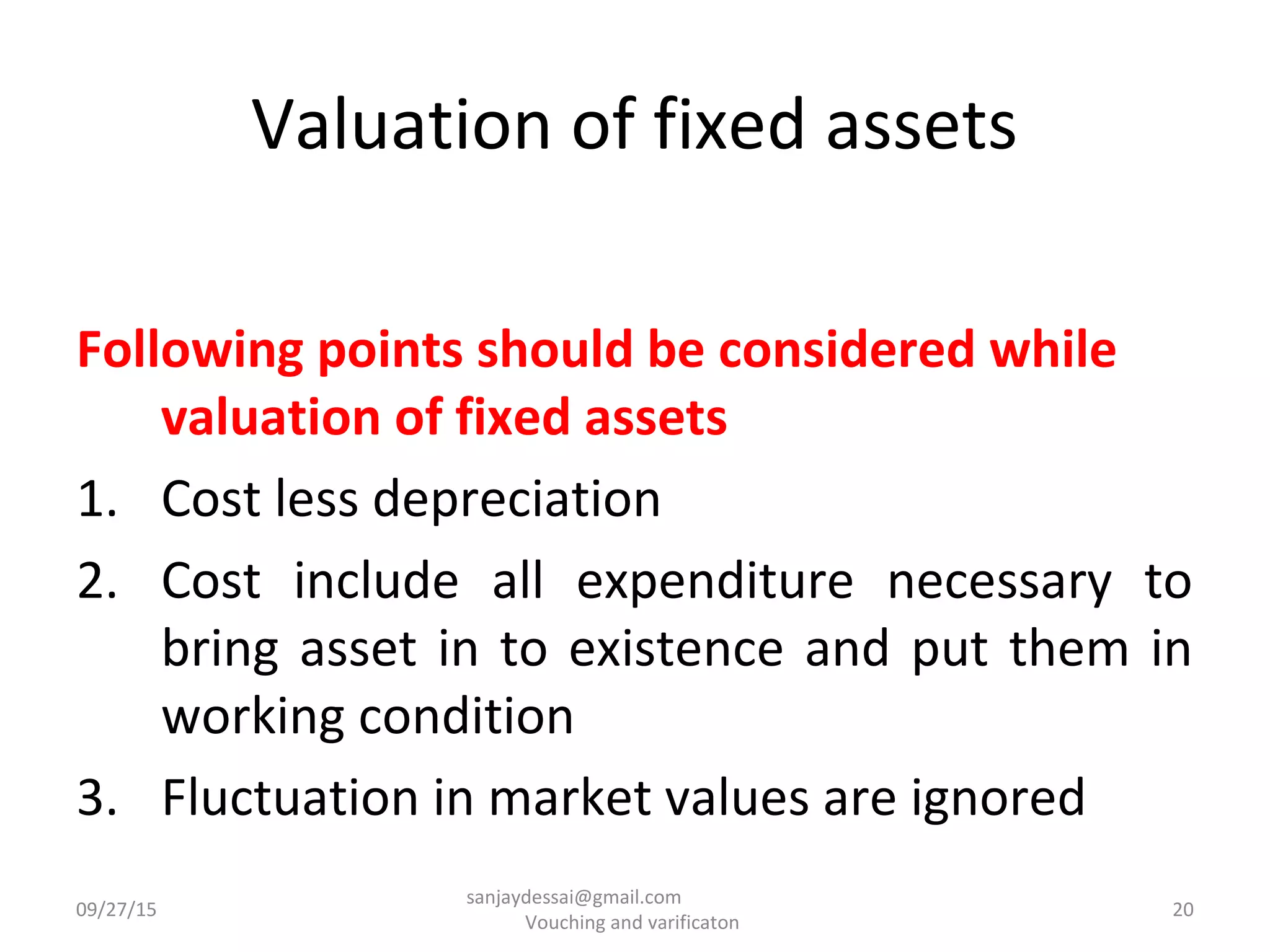

Key considerations for fixed assets valuation, including costs and depreciation.

Verification of plant and machinery including inspection of registers and proper valuation.

Audit procedures for verifying preliminary expenses like document scrutiny and amortization.

Process for obtaining creditor schedules and verifying payments and liabilities.

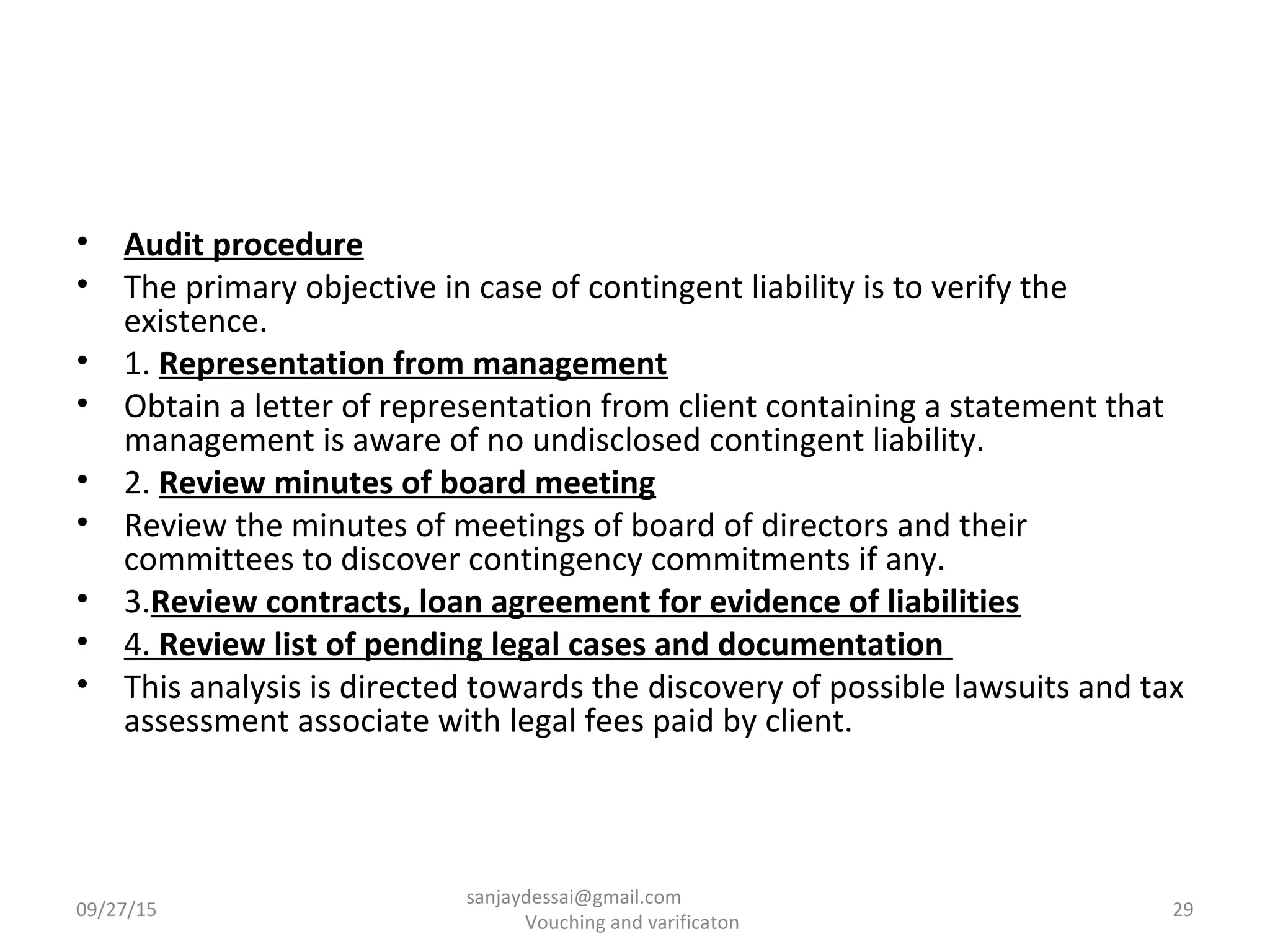

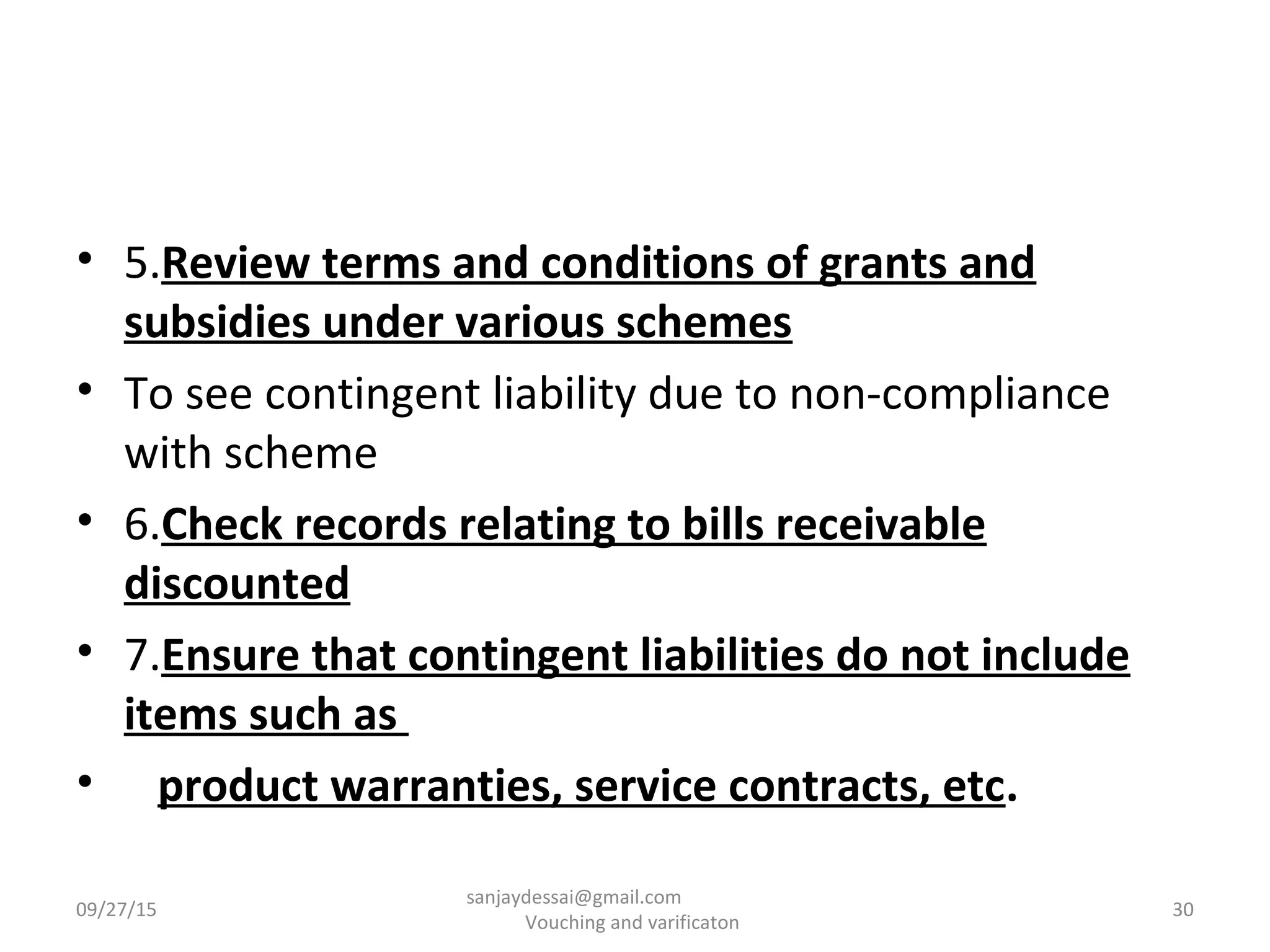

Identification and verification of contingent liabilities through management representation.

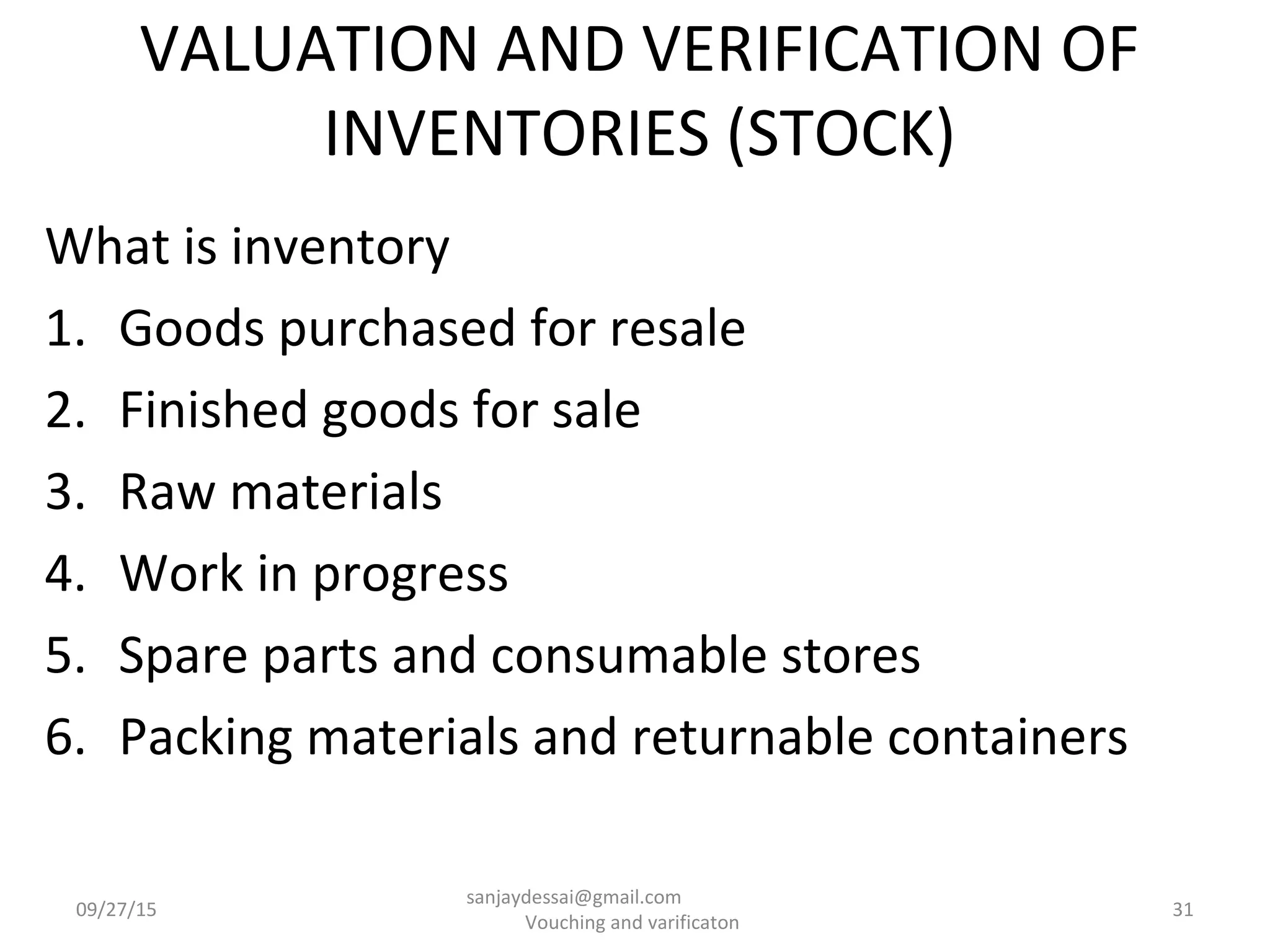

Definition and types of inventory related to auditing context.

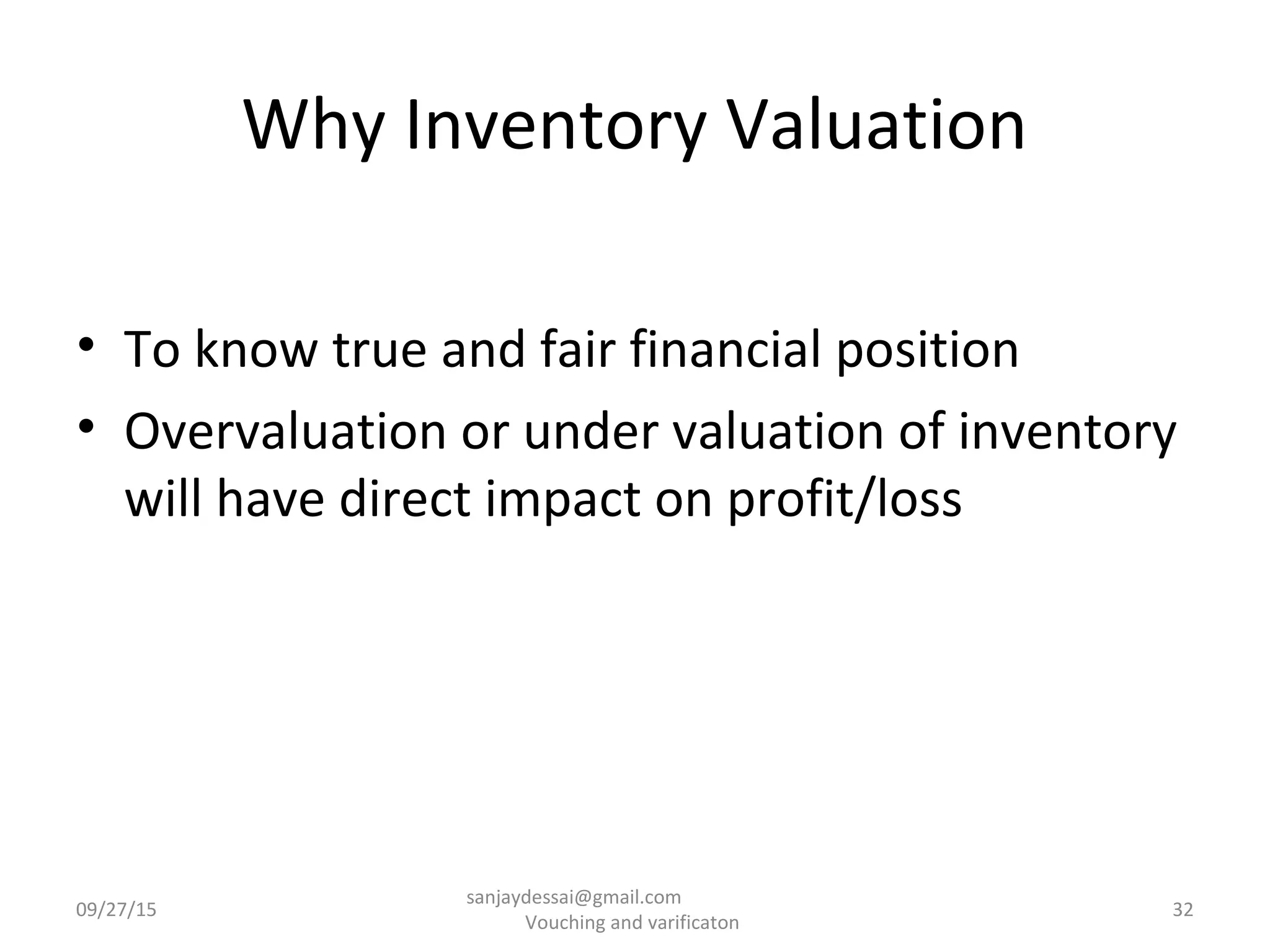

Understanding inventory valuation impact on true financial positions.

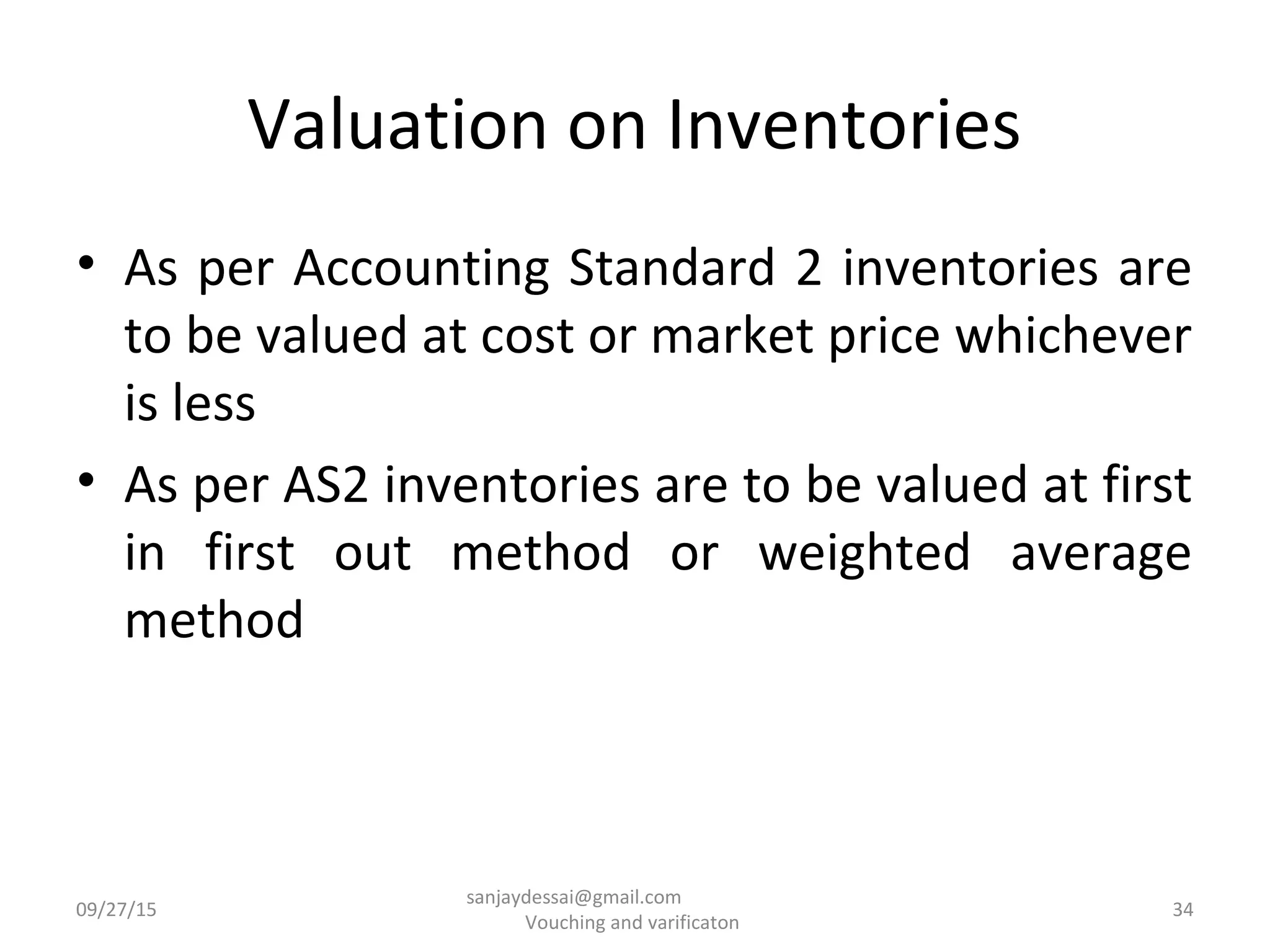

Different methods for inventory valuation, including cost and accounting standards compliance.

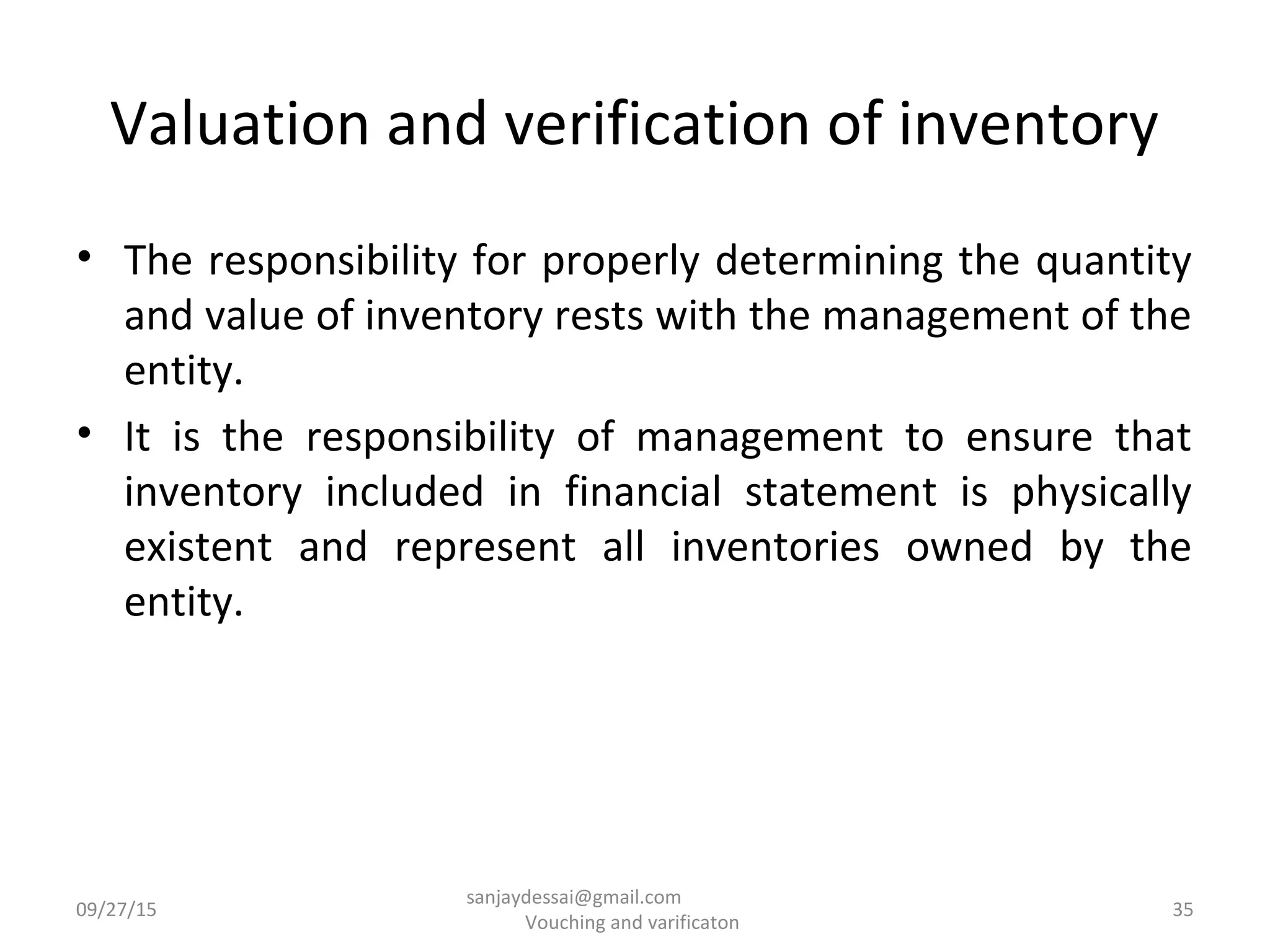

Management's duty to ensure accurate representation of inventory in financial statements.

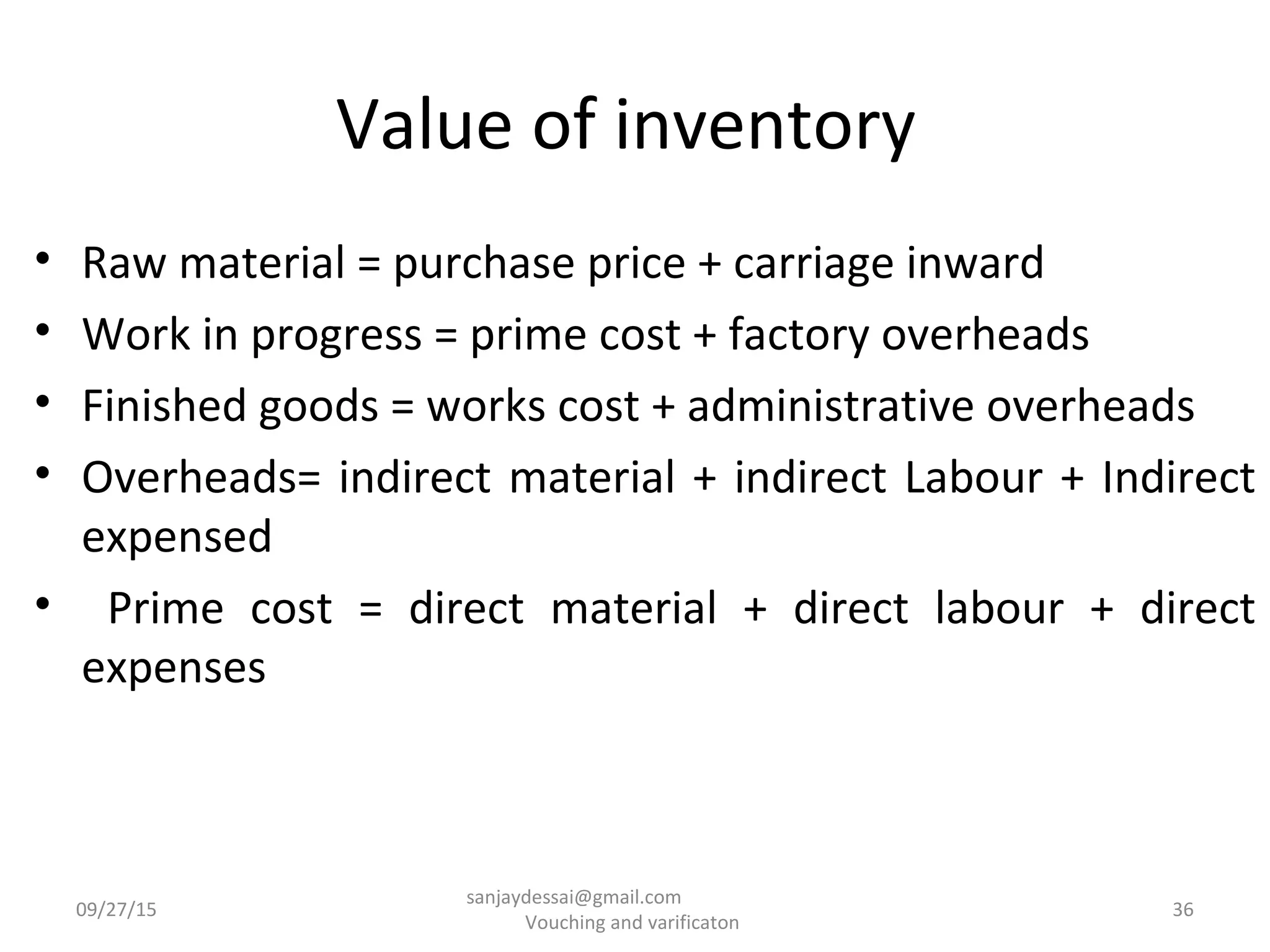

Components of inventory valuation including raw materials, WIP, and administrative overheads.

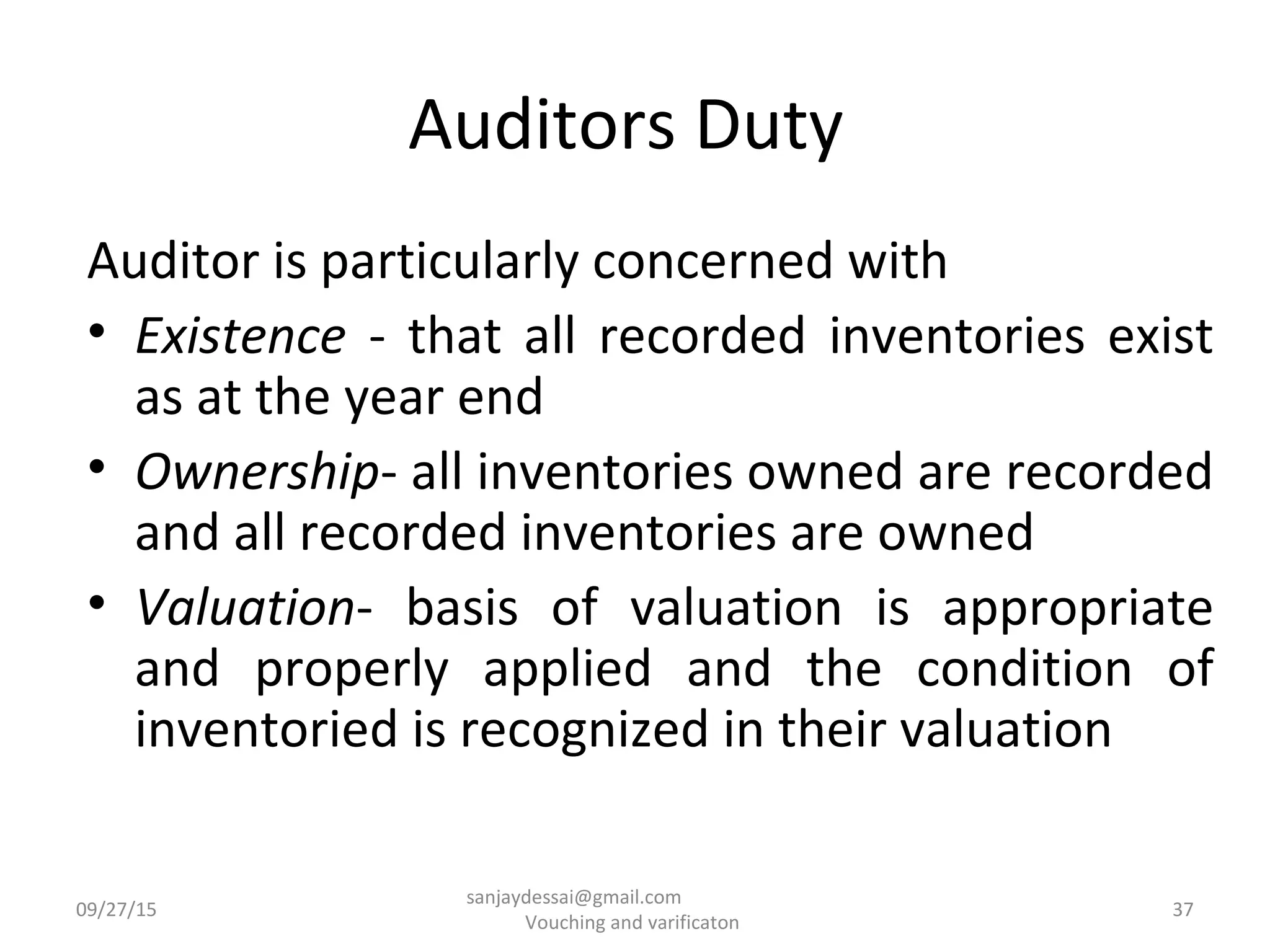

Auditors concerned with existence, ownership, and valuation of inventory.

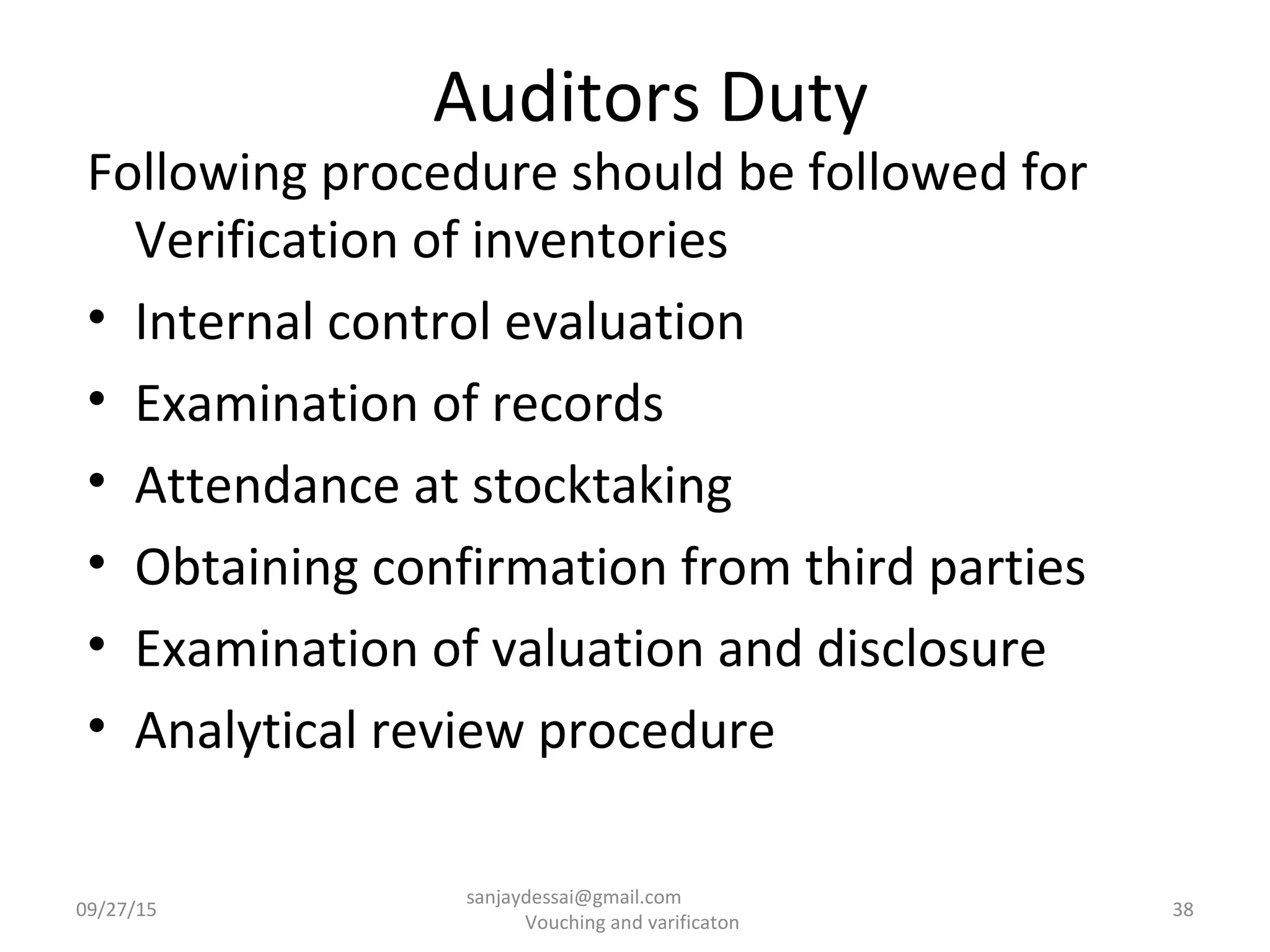

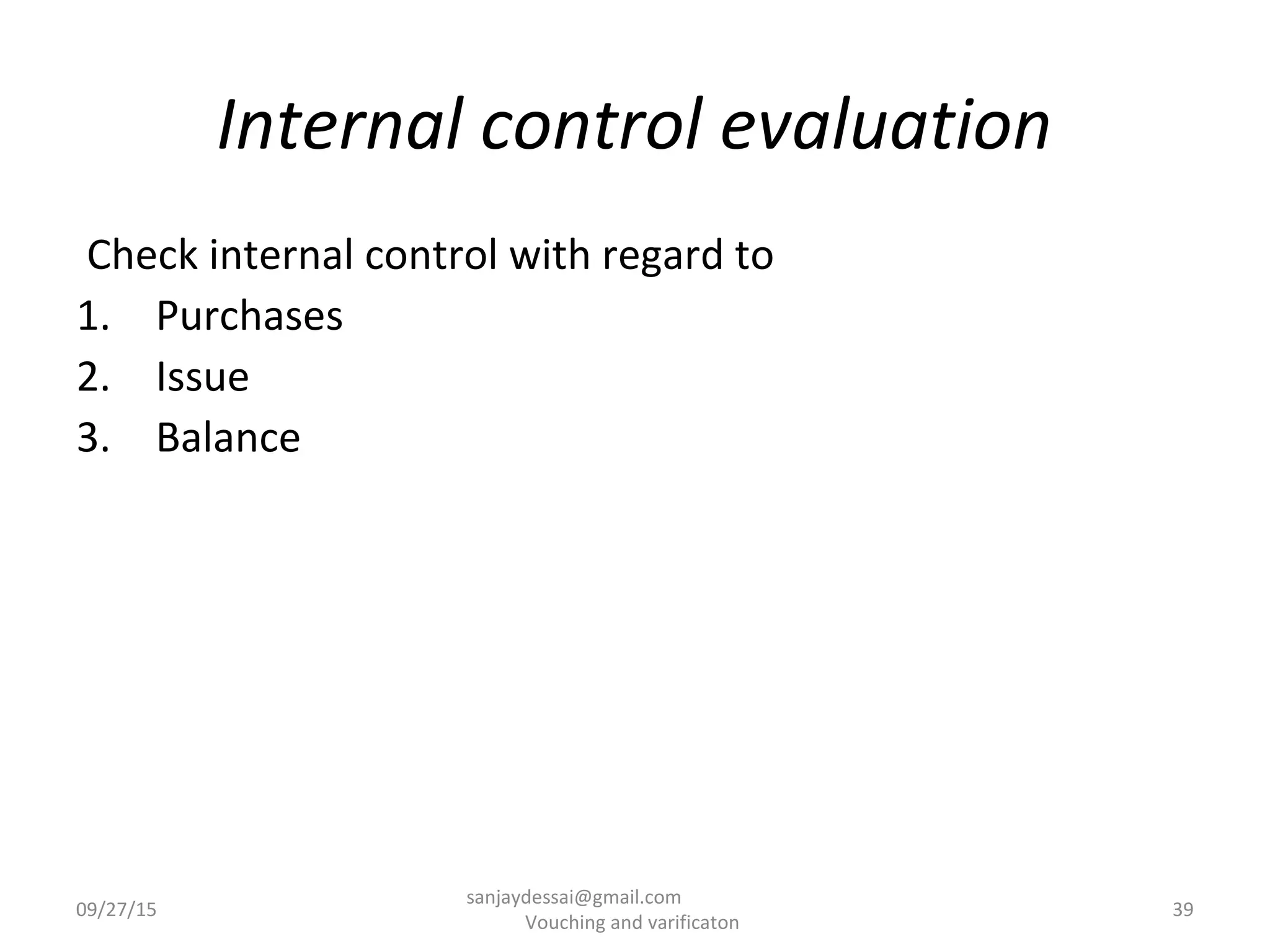

Internal control checks on inventory processes including purchases and issues.

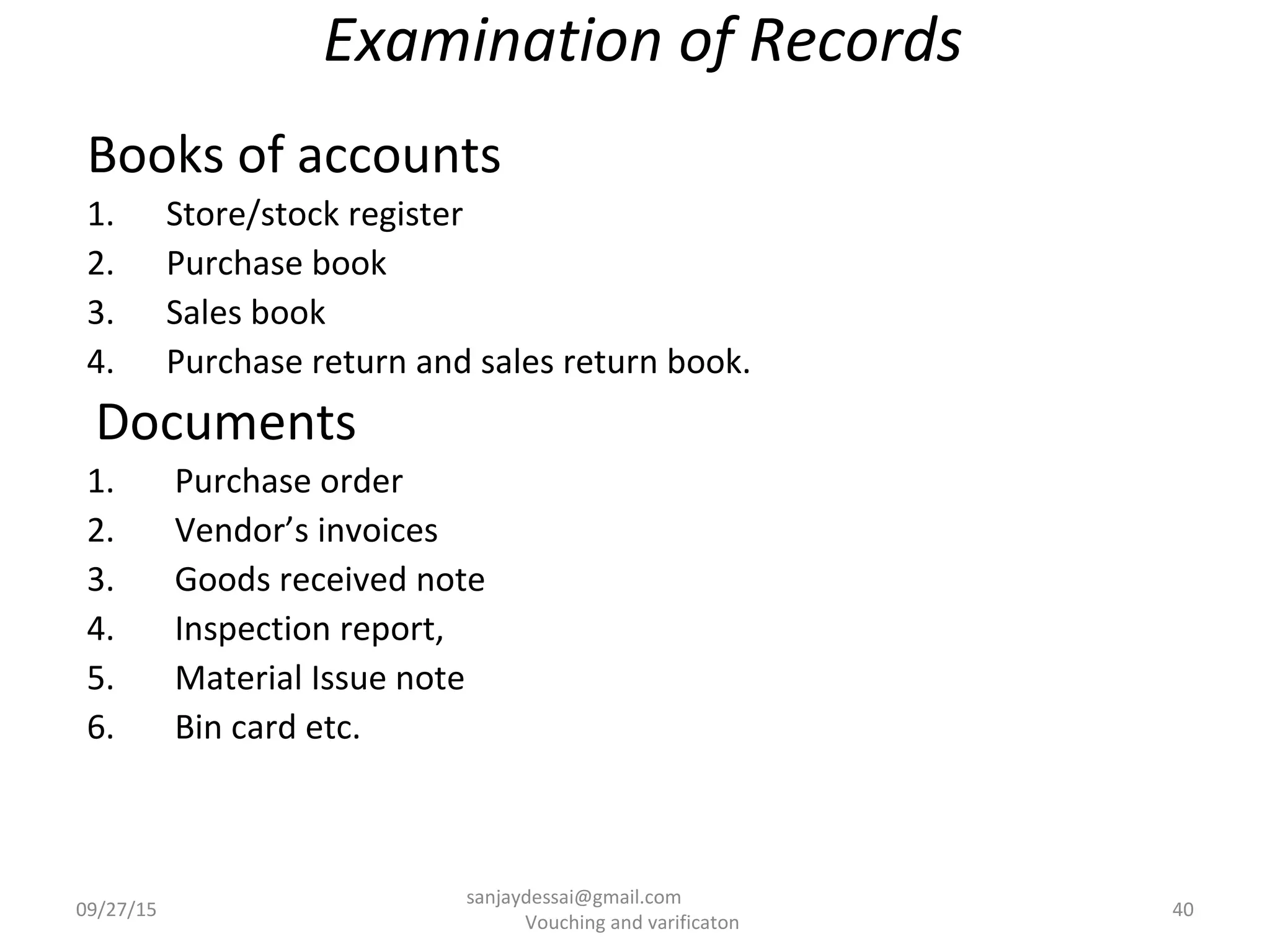

Required documentation for inventory verification including purchasing and stock records.

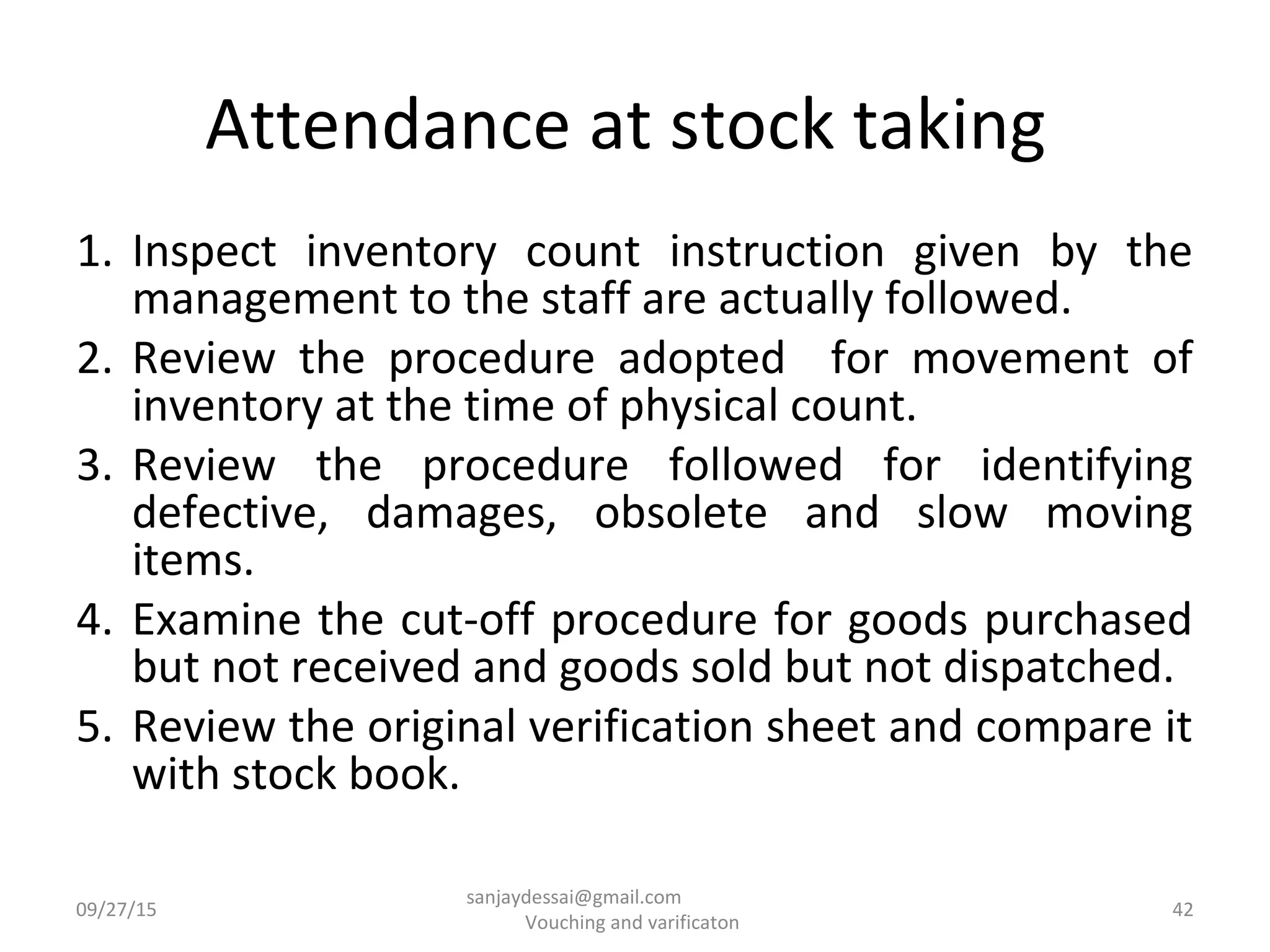

Procedures for auditors during physical counts of inventory to ensure accuracy.

Obtaining confirmations from third parties holding inventory.

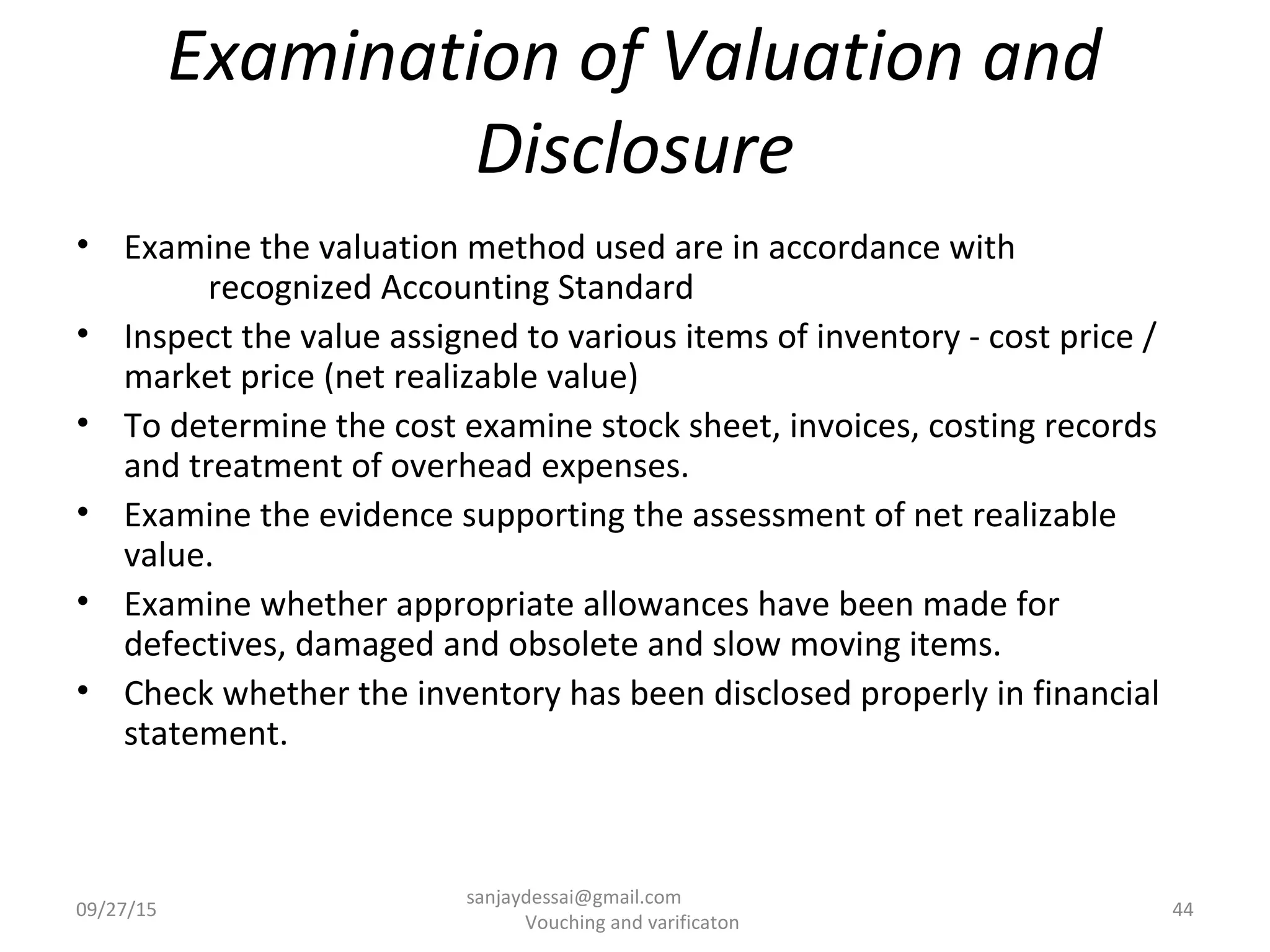

Examination of inventory valuation methods and their compliance with accounting standards.

Methods of reconciling inventory figures and assessing performance metrics.

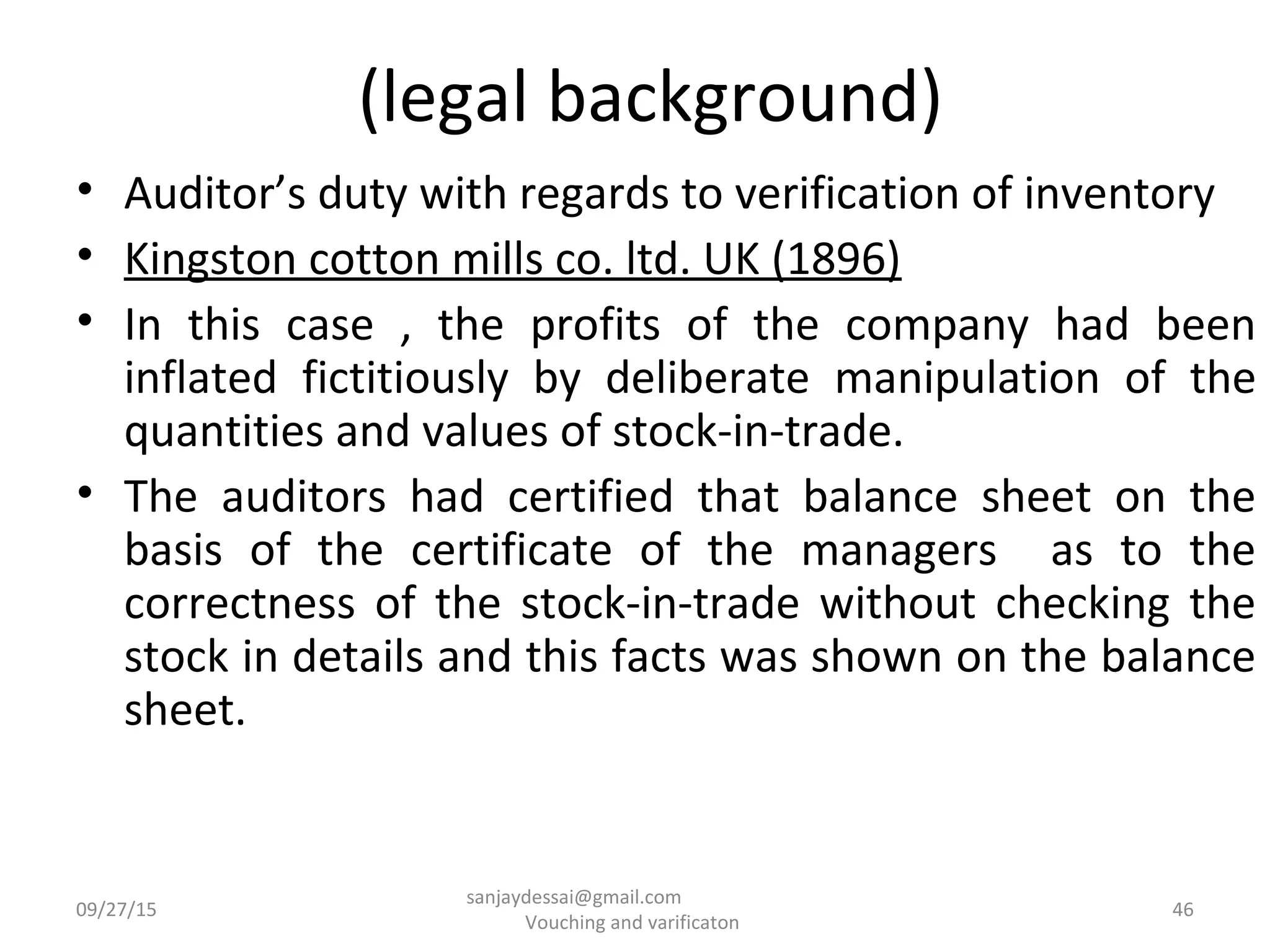

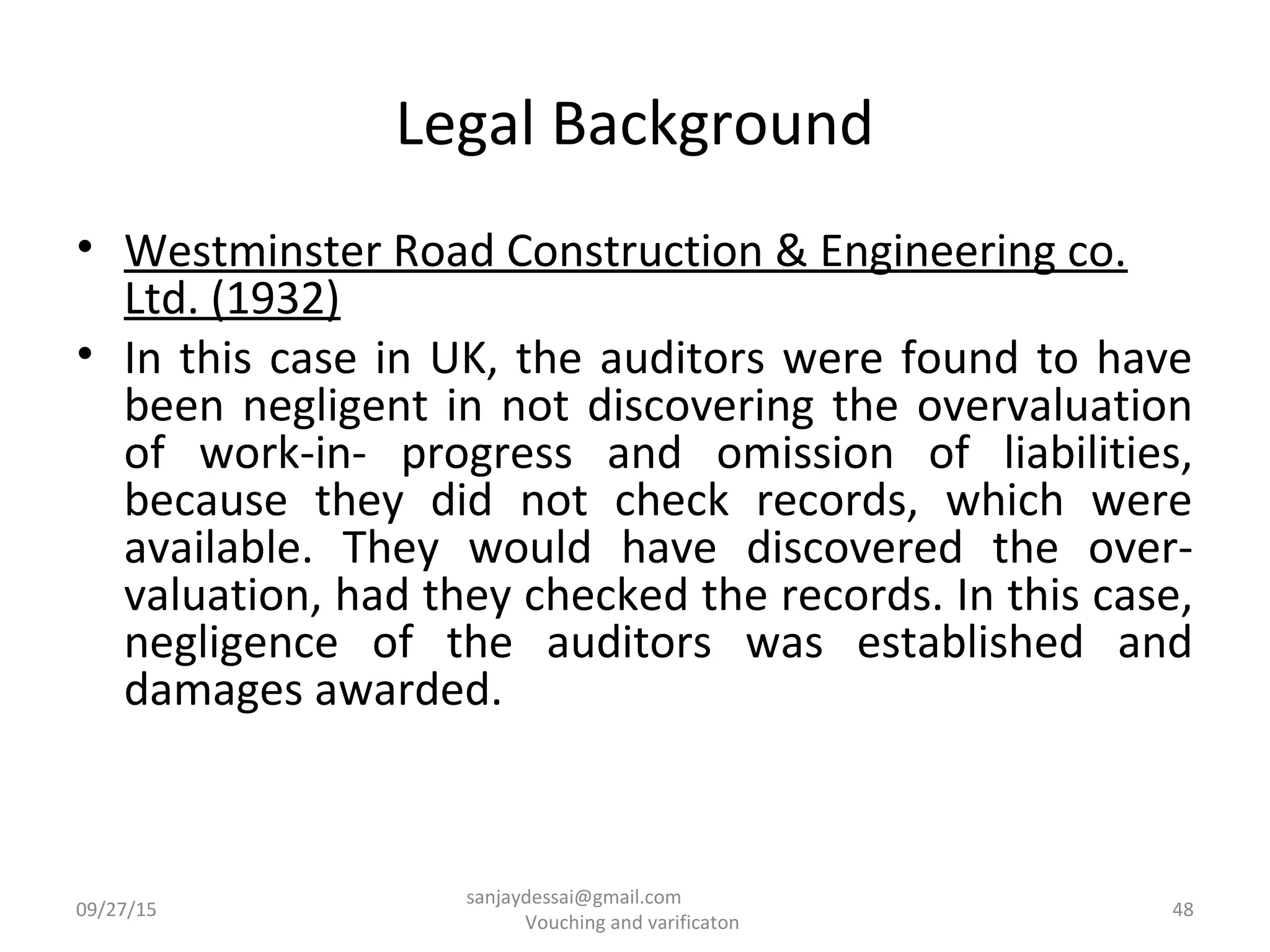

Legal precedents regarding auditor responsibilities in inventory verification.

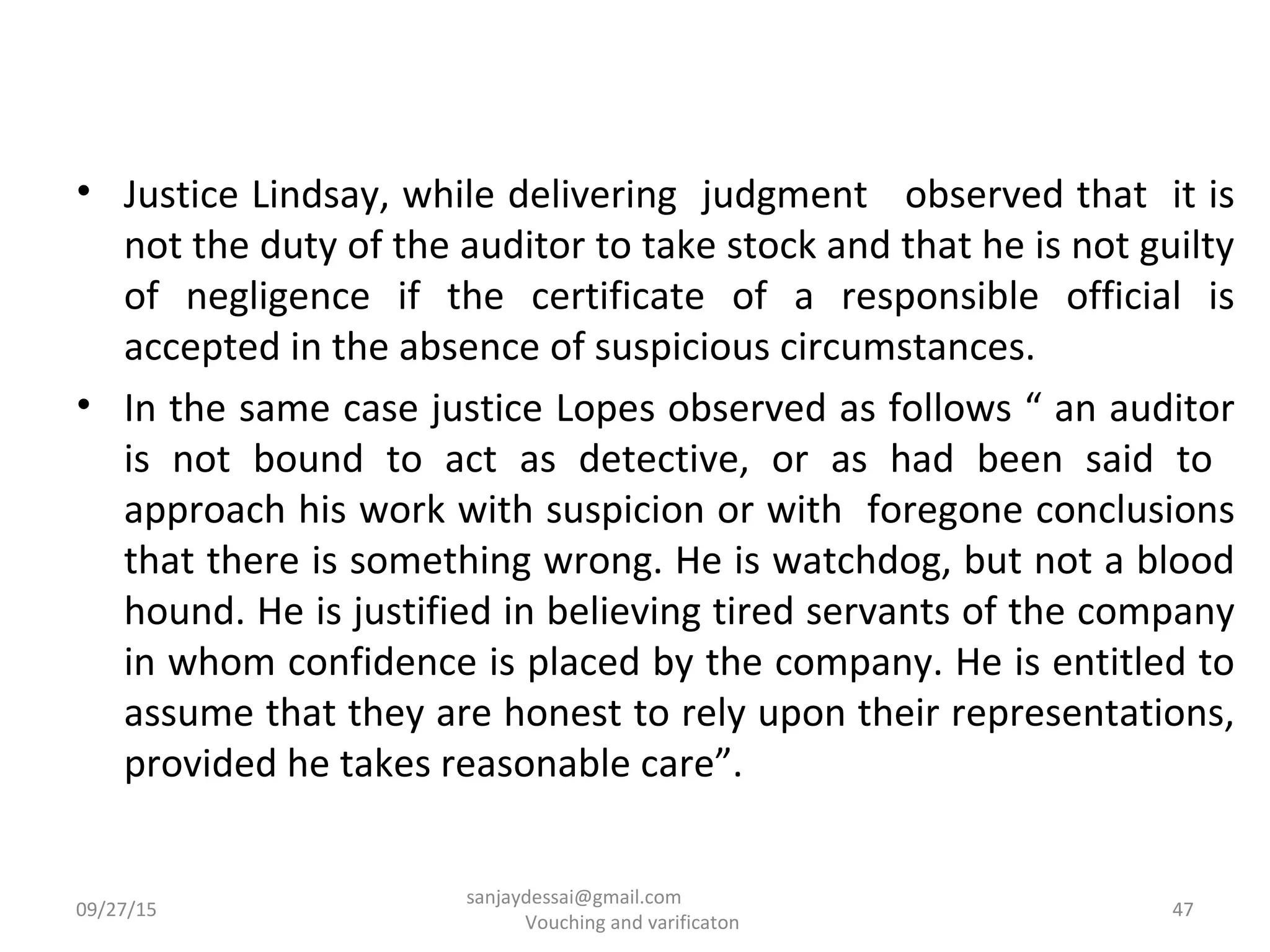

Guidelines on auditor's responsibility for stock verification and reliance on management statements.