Tutorial 4 eps_question

•Download as DOC, PDF•

0 likes•1,352 views

Cerdas Berhad issued additional shares and bought back shares during 2013. Their net profit for 2013 was RM83,500,000. The document provides information needed to calculate basic EPS for Cerdas Berhad for 2013. The document also provides MBM Berhad's capital structure, earnings information, and additional details needed to calculate basic and diluted EPS for MBM Berhad for 2013. Legasi Bhd reported net income of RM2,000,000 for 2013. The document provides details of Legasi Bhd's share transactions and convertible instruments to enable calculation of basic and diluted EPS for Legasi Bhd for 2013.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (12)

Similar to Tutorial 4 eps_question

Similar to Tutorial 4 eps_question (20)

More from kim rae KI

Recently uploaded

Recently uploaded (20)

Tutorial 4 eps_question

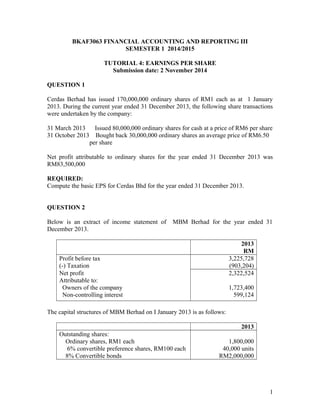

- 1. BKAF3063 FINANCIAL ACCOUNTING AND REPORTING III SEMESTER 1 2014/2015 TUTORIAL 4: EARNINGS PER SHARE Submission date: 2 November 2014 QUESTION 1 Cerdas Berhad has issued 170,000,000 ordinary shares of RM1 each as at 1 January 2013. During the current year ended 31 December 2013, the following share transactions were undertaken by the company: 31 March 2013 Issued 80,000,000 ordinary shares for cash at a price of RM6 per share 31 October 2013 Bought back 30,000,000 ordinary shares an average price of RM6.50 per share Net profit attributable to ordinary shares for the year ended 31 December 2013 was RM83,500,000 REQUIRED: Compute the basic EPS for Cerdas Bhd for the year ended 31 December 2013. QUESTION 2 Below is an extract of income statement of MBM Berhad for the year ended 31 December 2013. 2013 RM Profit before tax 3,225,728 (-) Taxation (903,204) Net profit 2,322,524 Attributable to: Owners of the company Non-controlling interest 1,723,400 599,124 The capital structures of MBM Berhad on I January 2013 is as follows: 2013 Outstanding shares: Ordinary shares, RM1 each 1,800,000 6% convertible preference shares, RM100 each 40,000 units 8% Convertible bonds RM2,000,000 1

- 2. Additional information: 1. The 6% convertible preference shares are cumulative preference shares and each unit is convertible into 15 units of ordinary shares. 2. The 8% convertible bonds is convertible into 300 units of the ordinary shares for each RM1,000 bonds. On 1 April 2013, RM200,000 were converted into ordinary shares. 3. In early 2012, the company granted options to its employees to buy the ordinary shares totaled 120,000 units for RM20.00 each. No option has been exercised so far and the exercise date dues on 31 December 2015. 4. The company declared a 1 for 1 bonus issue on 1 July 2014. 5. On 1 October 2013, the company issued additional 100,000 units of ordinary shares. 6. The average price of ordinary shares for the year 2013 was RM24.00 each share. 7. The tax rate for the year 2013 was 25%. REQUIRED: (Round your answer to the nearest cent). (a) Determine the weighted average of outstanding shares used for calculating the basic earnings per share for the year 2013. (b) Calculate the basic earnings per share for the year 2013. (c) Calculate the diluted earnings per share for the year 2013 (support with calculations). 2

- 3. QUESTION 3 Legasi Bhd which was incorporated in 2010 has reported net income of RM2,000,000 for the year ended 31 December 2013. The tax rate is 25%. Its capital structure included: Ordinary Shares 1 January 2013 4,000,000 ordinary shares outstanding 1 July 2013 1,500,000 new shares issued 1 October 2013 1,000,000 shares reacquired as treasury shares The average market price of ordinary shares during 2013 was RM25 per share. Convertible Preference Shares On 1 January 2013, RM4,000,000, 8% cumulative, convertible preference shares at a par value of RM50 were issued and outstanding. Each of convertible preference shares is convertible into 20 ordinary shares. There were no preference dividends in arrears; however, Legasi Bhd has not declared preference shares dividends for the year 2013. Share Options Options were granted in 2011 to purchase 500,000 ordinary shares at RM20 per share. No options were exercised during fiscal year 2013. Convertible Bonds On I January 2013, Legasi Bhd has 10% convertible bonds at a carrying amount of RM3,000,000. This convertible bonds have been issued in 2010 and will be converted into 600 ordinary shares per RM1,000 bonds. On 1 September 2013, 70% of the convertible bonds have been converted into ordinary shares. REQUIRED: (Round the answer to three decimal points) (a) Determine the weighted average of shares outstanding and calculate the basic earnings per share for the year ended 31 December 2013. (b) Calculate the diluted earnings per share for the year ended 31 December 2013. 3