Downloaded 61 times

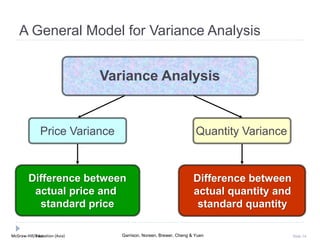

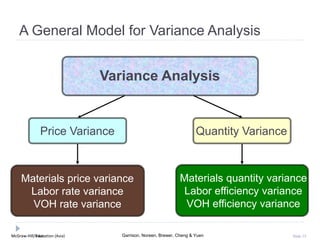

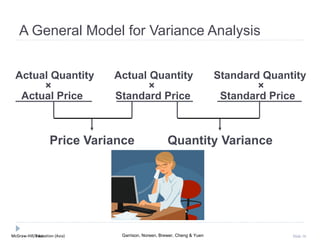

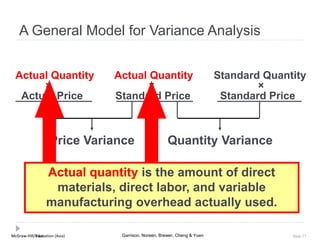

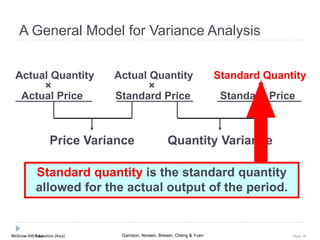

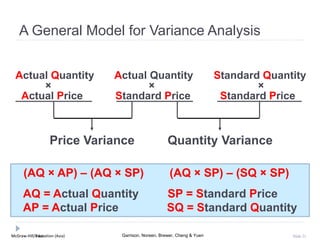

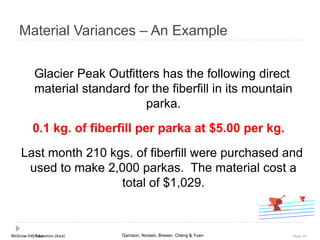

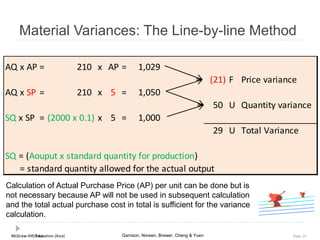

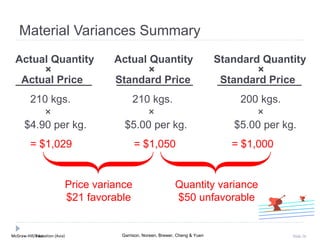

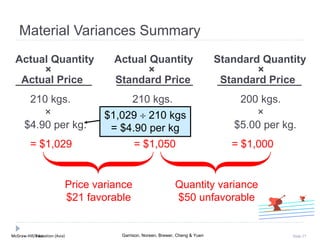

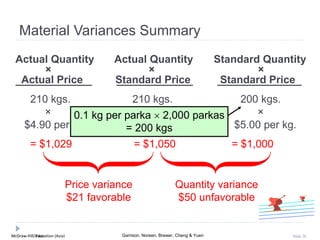

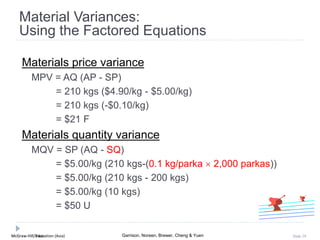

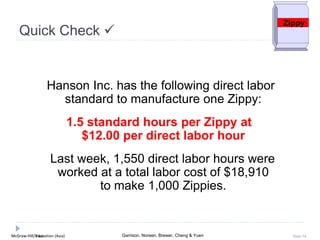

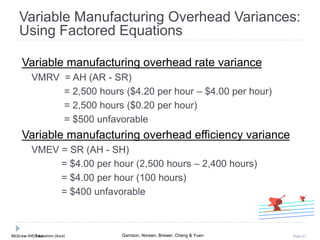

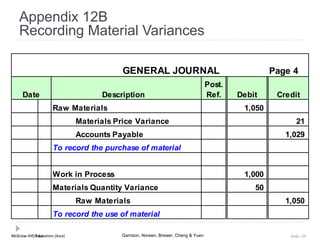

- Standards are benchmarks used to measure performance in managerial accounting. Quantity standards specify the input amounts, while price standards specify input costs. - Direct material price and quantity variances are calculated to analyze differences between actual and standard costs. The price variance is the difference due to actual price paid, while the quantity variance is due to using more or less material than standard. - An example calculates variances for a company that used 210kg of fiberfill costing $1,029 total to make 2,000 parkas. The $21 favorable price variance and $50 unfavorable quantity variance are determined.