Downloaded 220 times

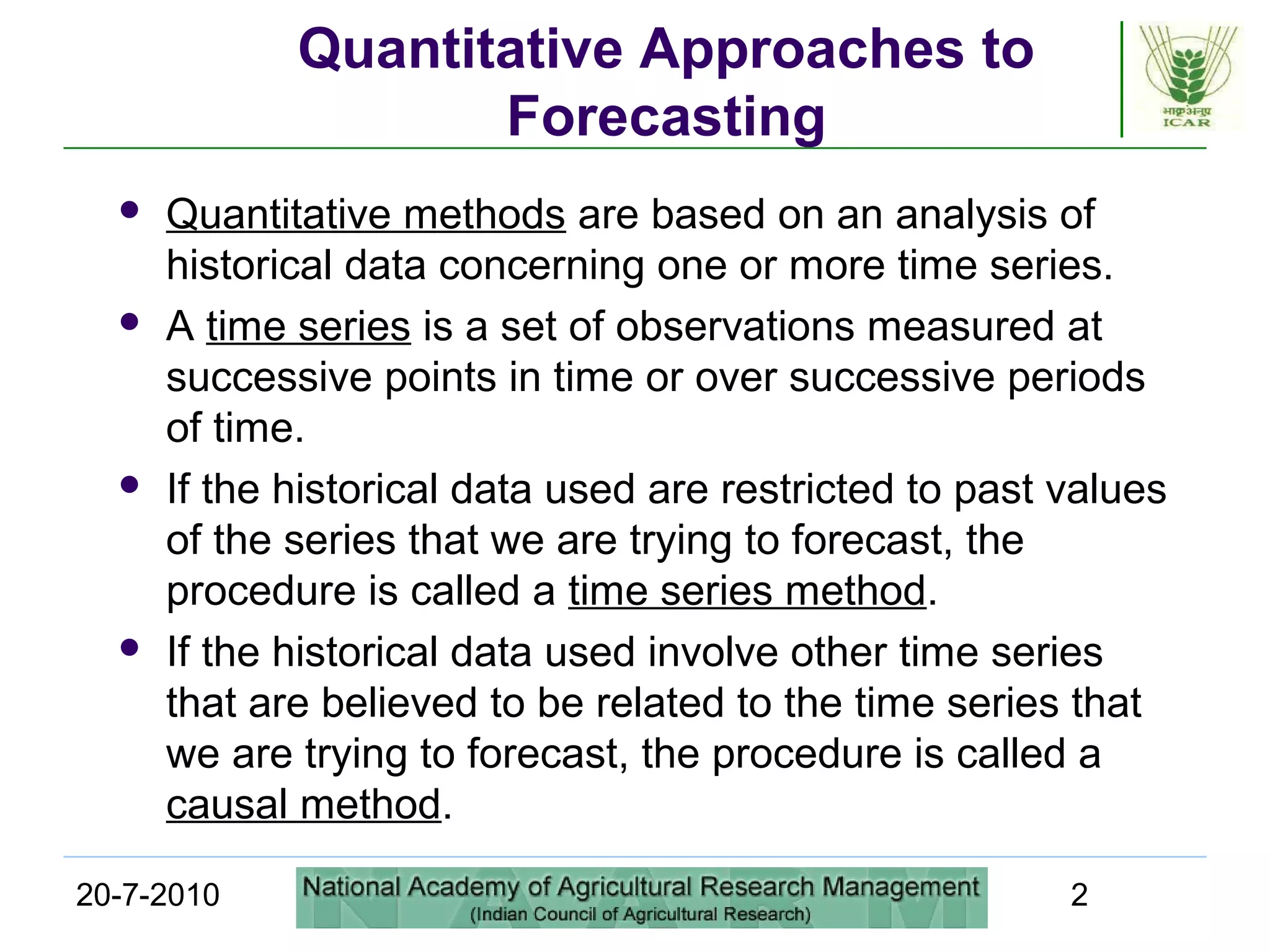

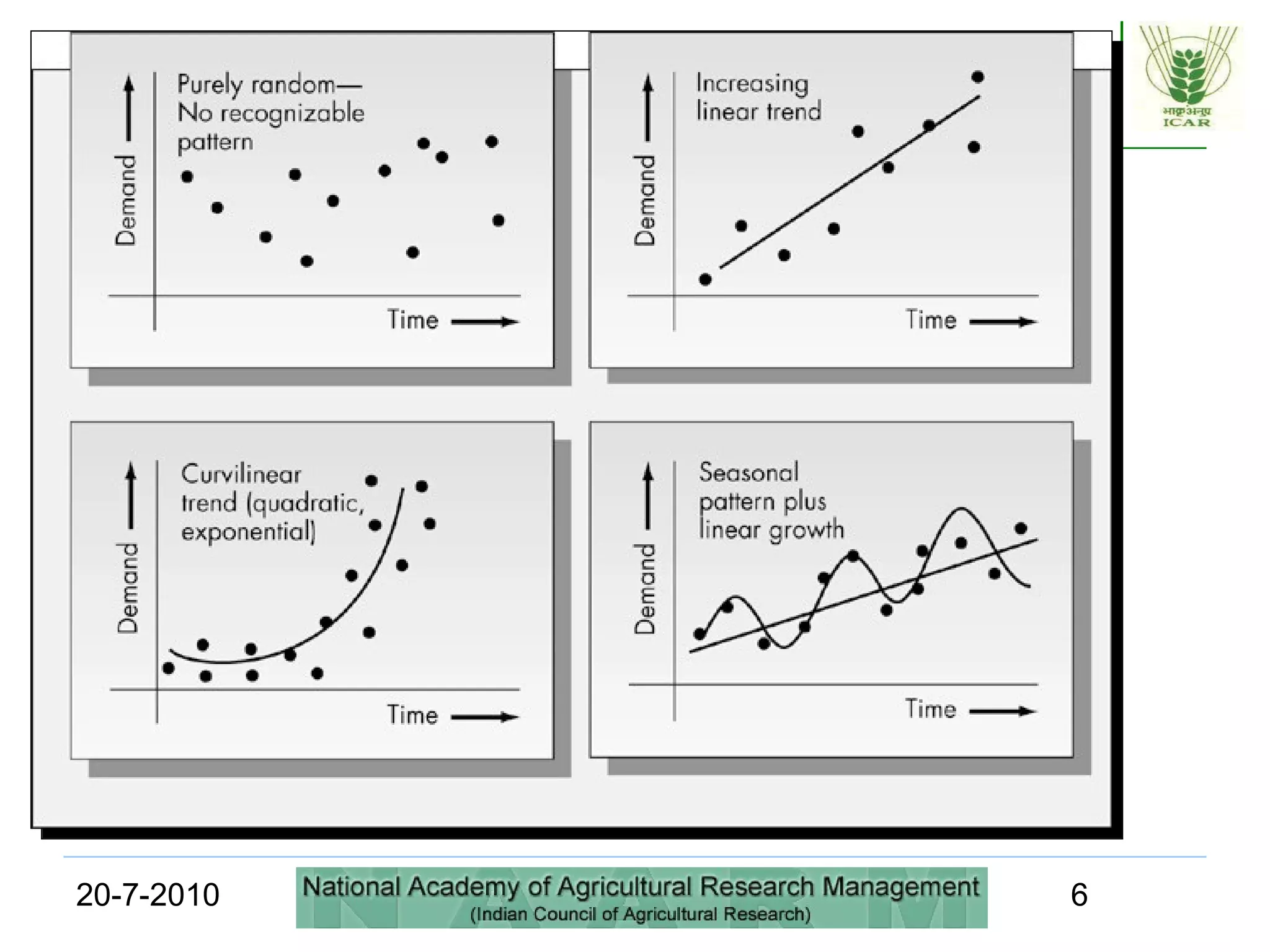

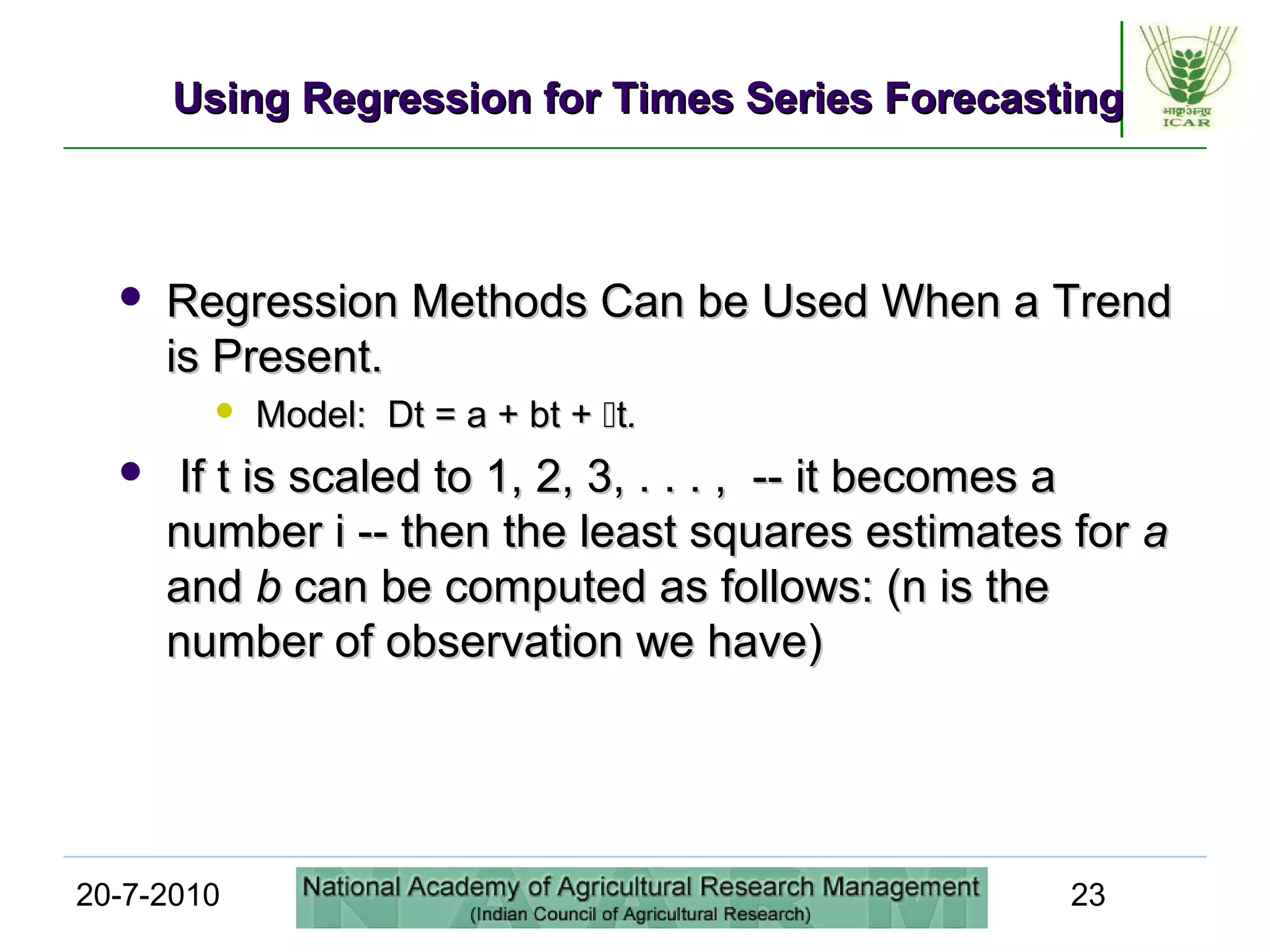

This document discusses quantitative forecasting methods, including time series and causal models. It covers key time series components like trend, seasonality, and cycles. Three main time series methods are described: smoothing, trend projection, and trend projection adjusted for seasonal influence. Moving averages and exponential smoothing are explained as common techniques for forecasting stationary time series. The document also covers decomposing a time series into trend, seasonal, and irregular components. Regression methods are mentioned as another approach when a trend is present in the data.