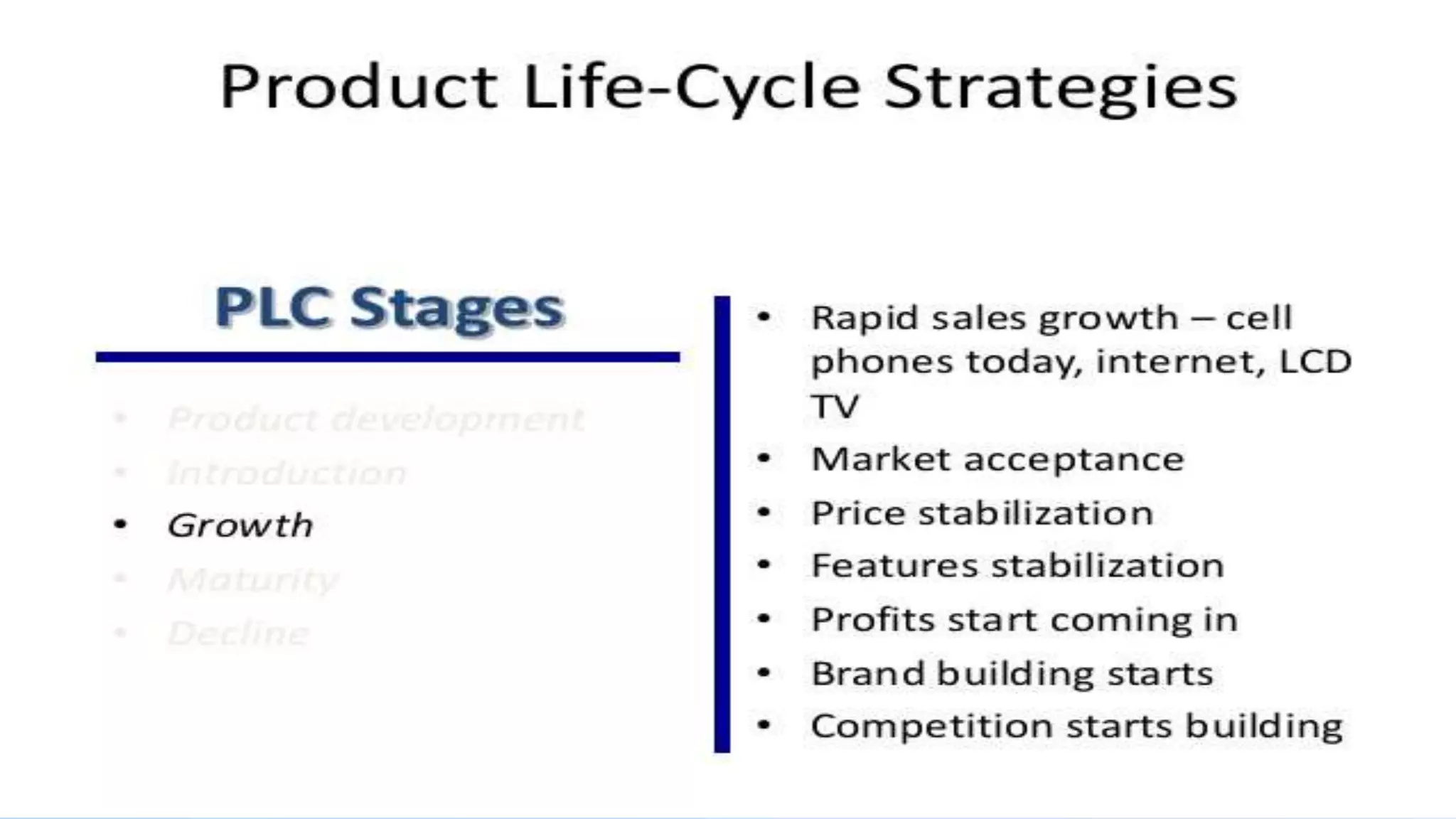

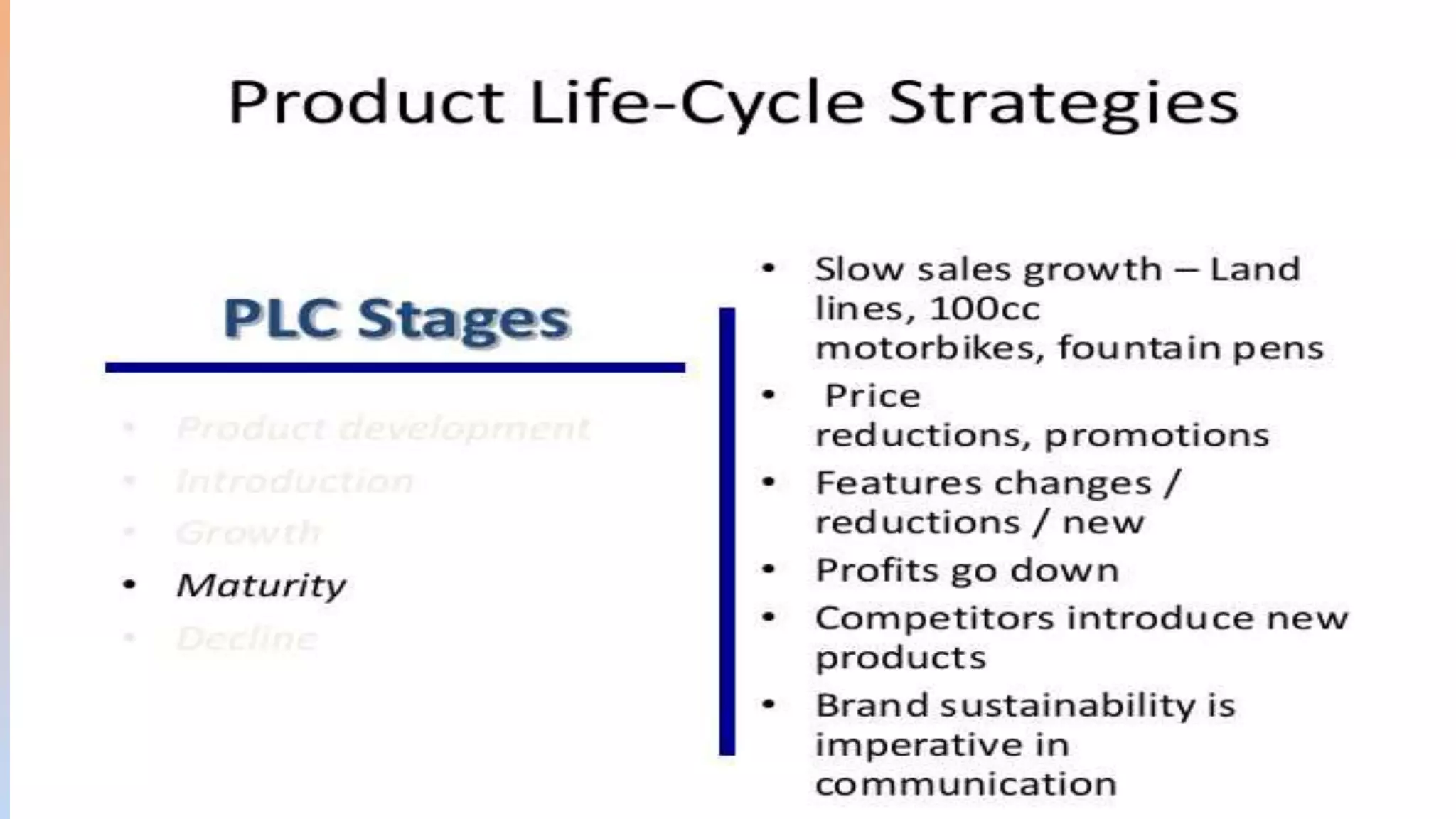

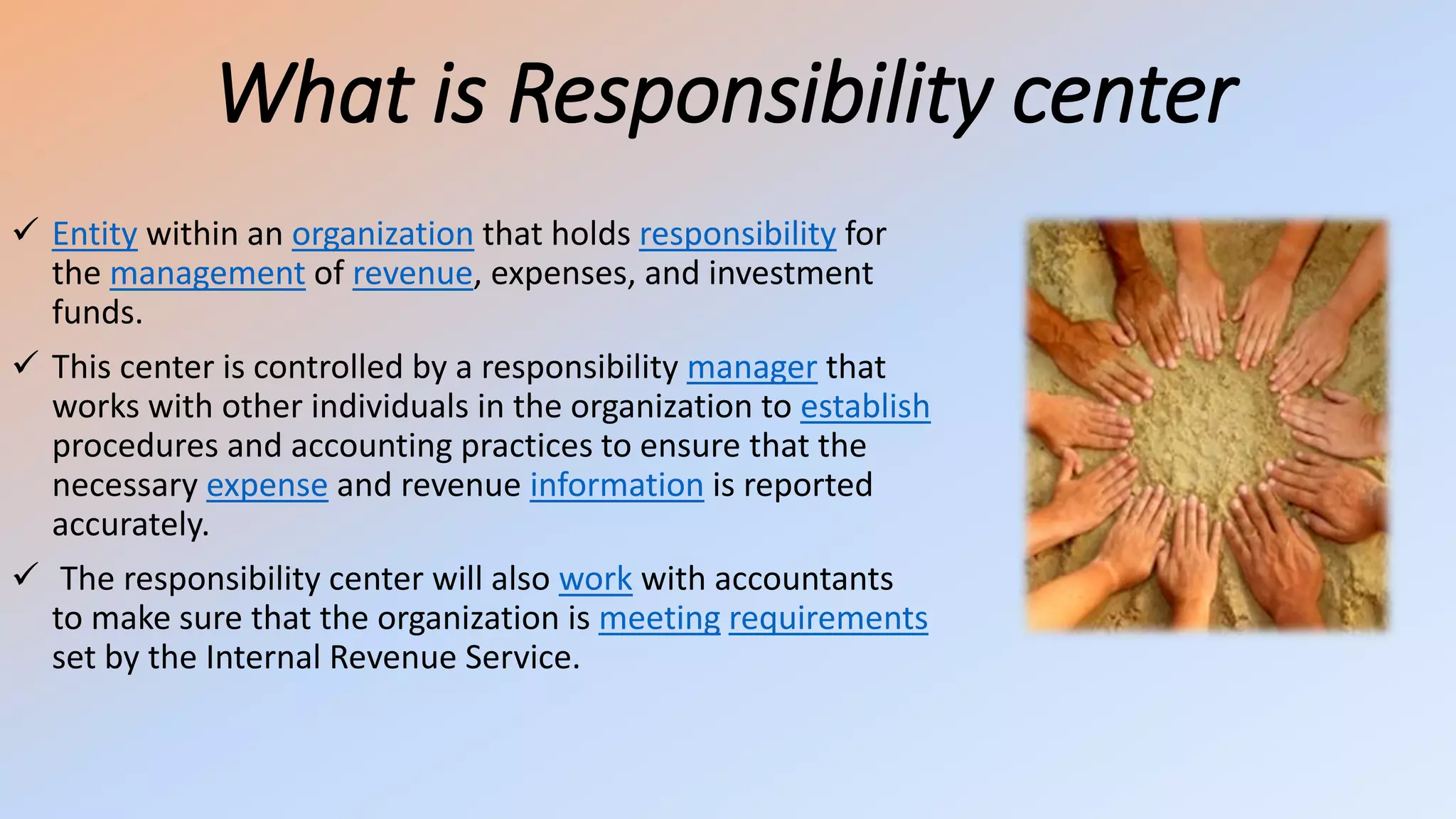

This document discusses responsibility centers and product life cycles. It defines responsibility centers as entities within an organization that are responsible for managing revenue, expenses, and investment funds. There are four main types of responsibility centers: cost centers, profit centers, investment centers, and revenue centers. The document also discusses target costing, which is setting a target cost for a product based on the desired selling price and profit. It outlines the objectives, applications, and limitations of using target costing. Additionally, the document covers value chain analysis and Porter's value chain model for analyzing a firm's activities to identify sources of competitive advantage. Finally, it defines transfer pricing as the price charged between different parts of the same company.

![Finlndia[1][2]1](https://cdn.slidesharecdn.com/ss_thumbnails/finlndia121-131228143103-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)