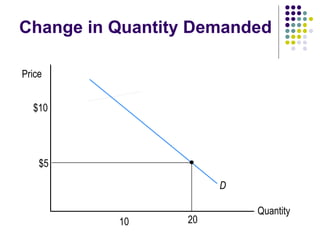

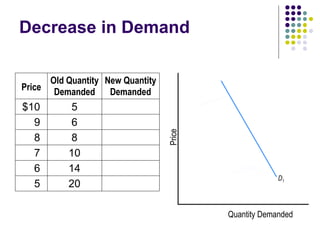

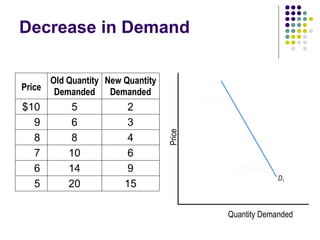

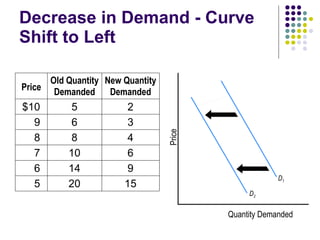

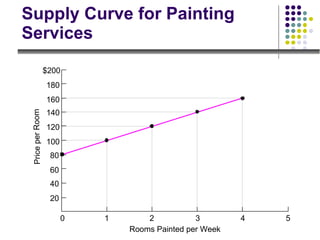

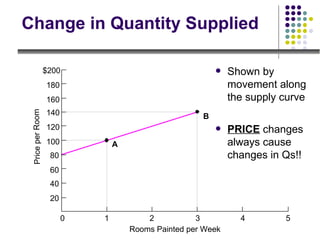

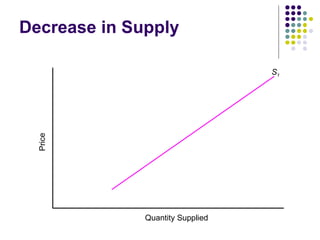

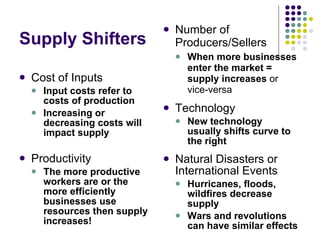

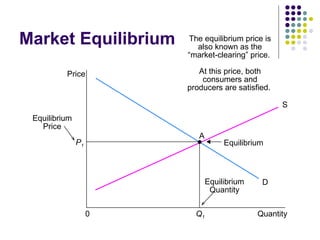

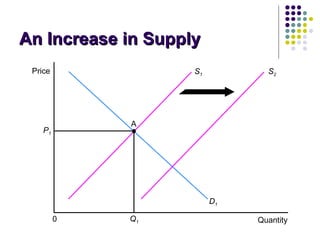

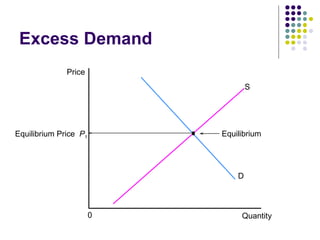

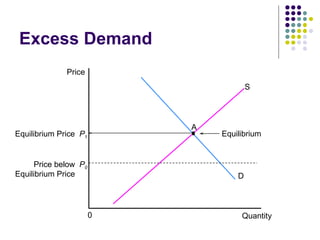

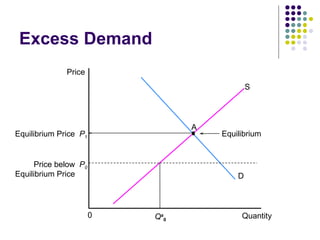

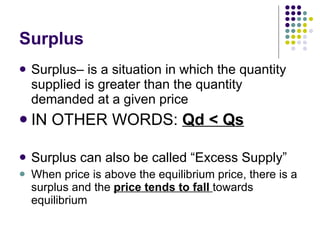

The document discusses supply and demand. It defines demand as the quantity consumers are willing and able to purchase at different prices. The law of demand states that quantity demanded increases when price decreases. Demand can shift due to factors like income, tastes, or prices of substitutes. Supply is defined as the quantity producers are willing to supply at different prices. The law of supply states that quantity supplied increases when price increases. Supply can shift due to costs of production, number of producers, or technology. Equilibrium occurs where quantity supplied equals quantity demanded. Disequilibrium results in shortages or surpluses which push prices toward the equilibrium level.