Download as PDF, PPTX

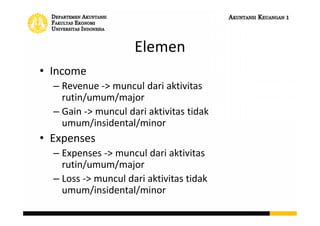

This document discusses the statement of comprehensive income. It begins by outlining the benefits and limitations of the income statement. It then describes the key elements of the income statement including revenue, expenses, gross profit, operating income, and net income. It also covers discontinued operations and how they are reported. The document concludes by explaining the statement of comprehensive income, retained earnings statement, and statement of changes in equity.