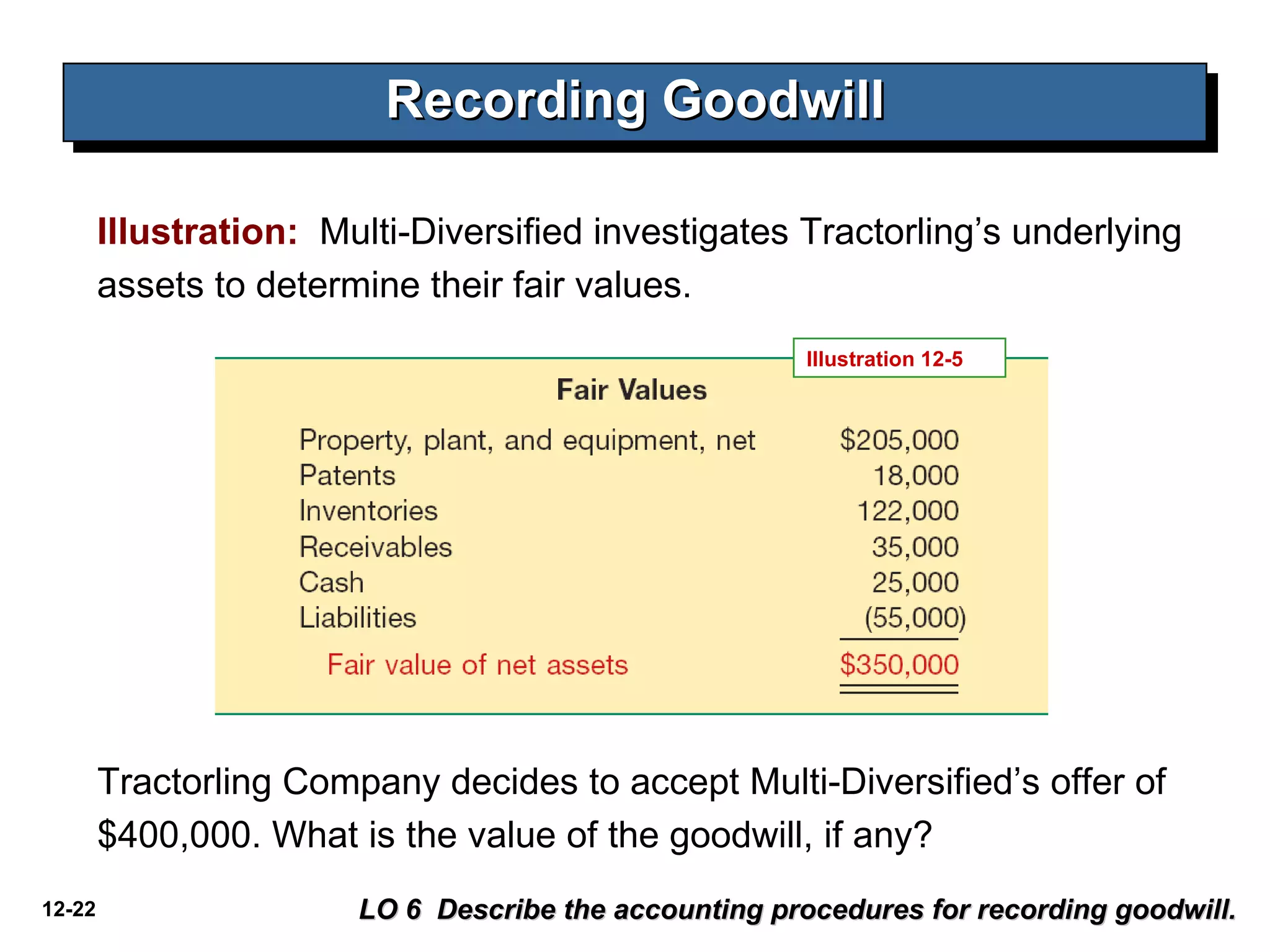

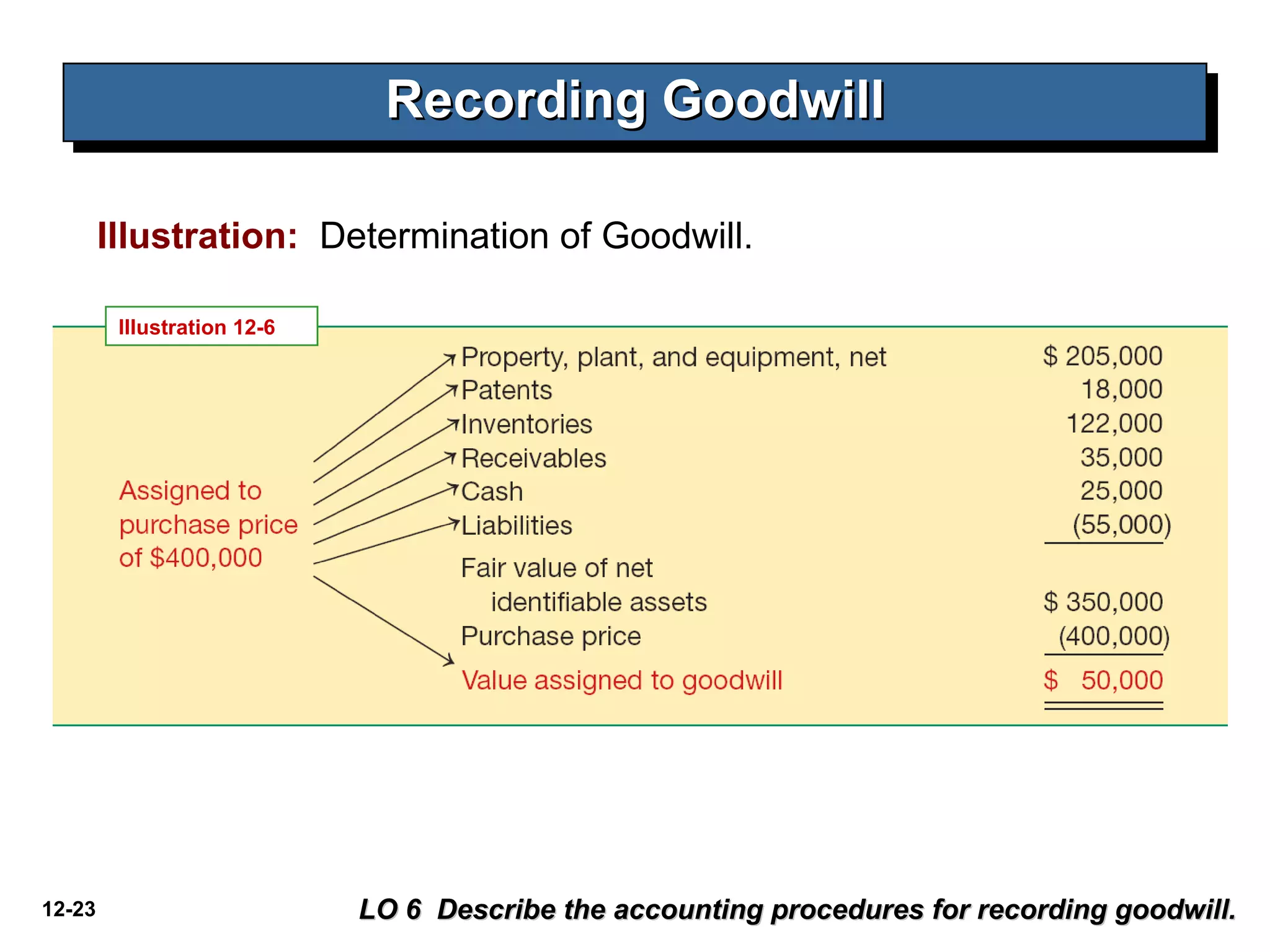

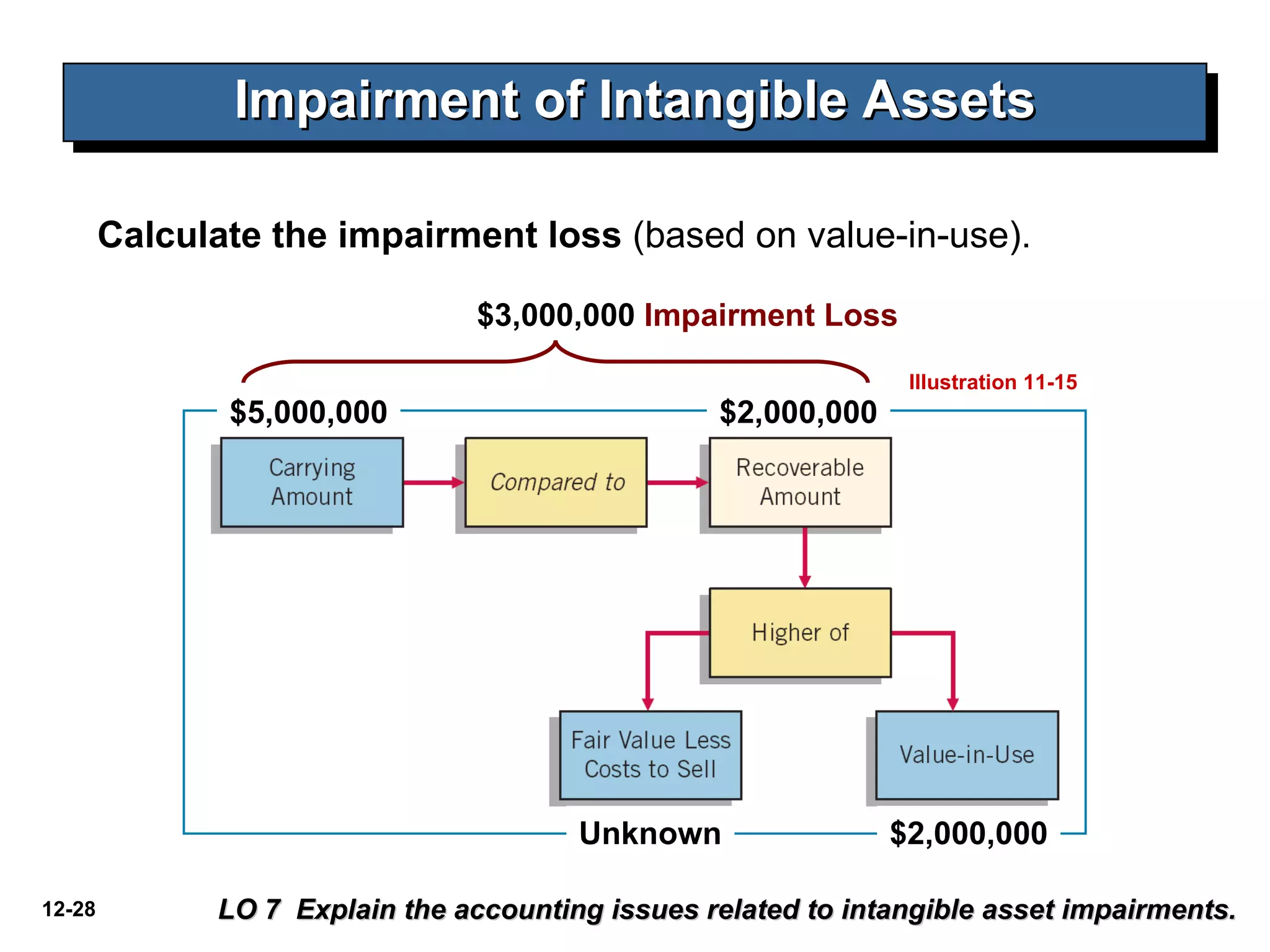

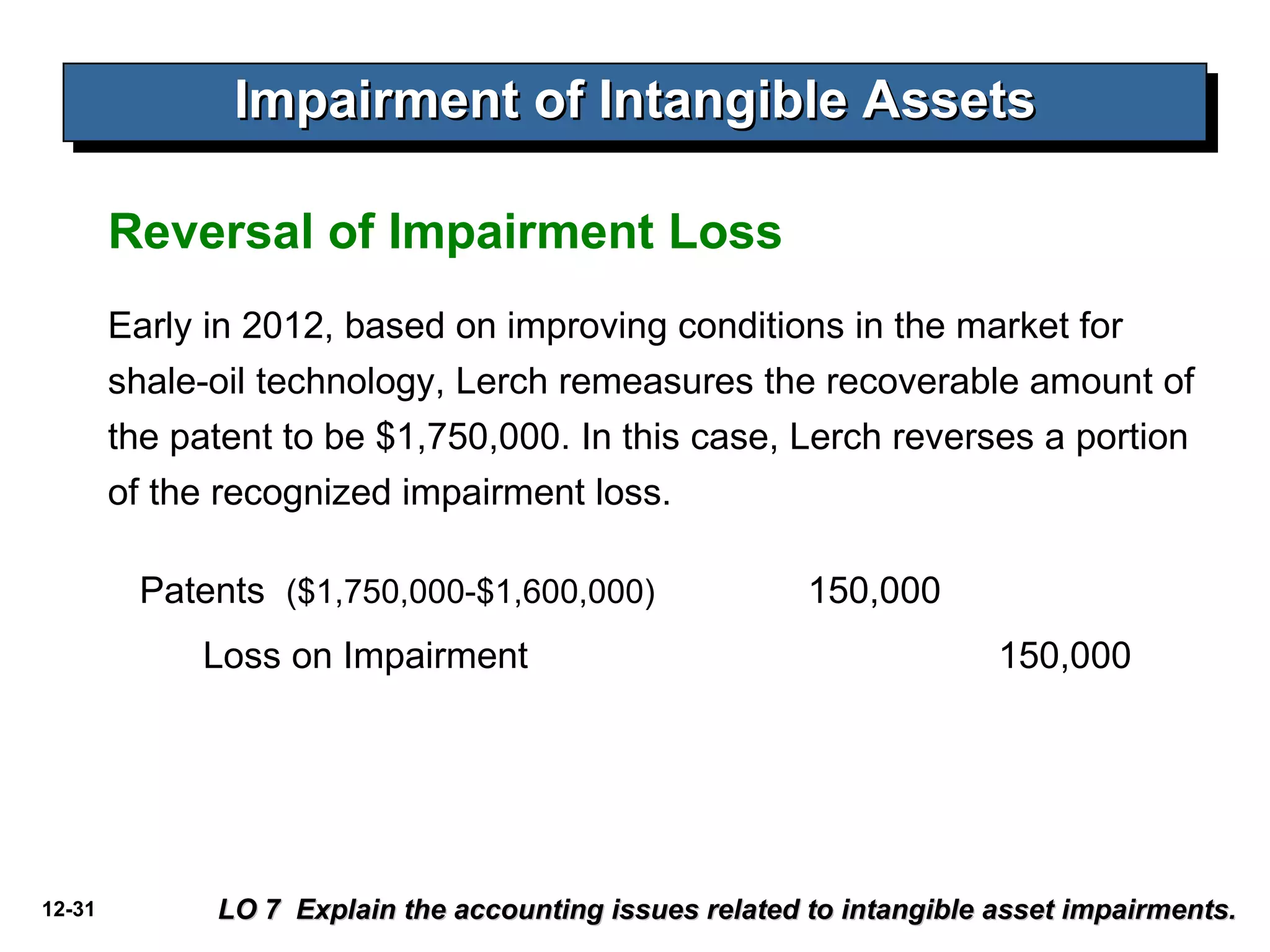

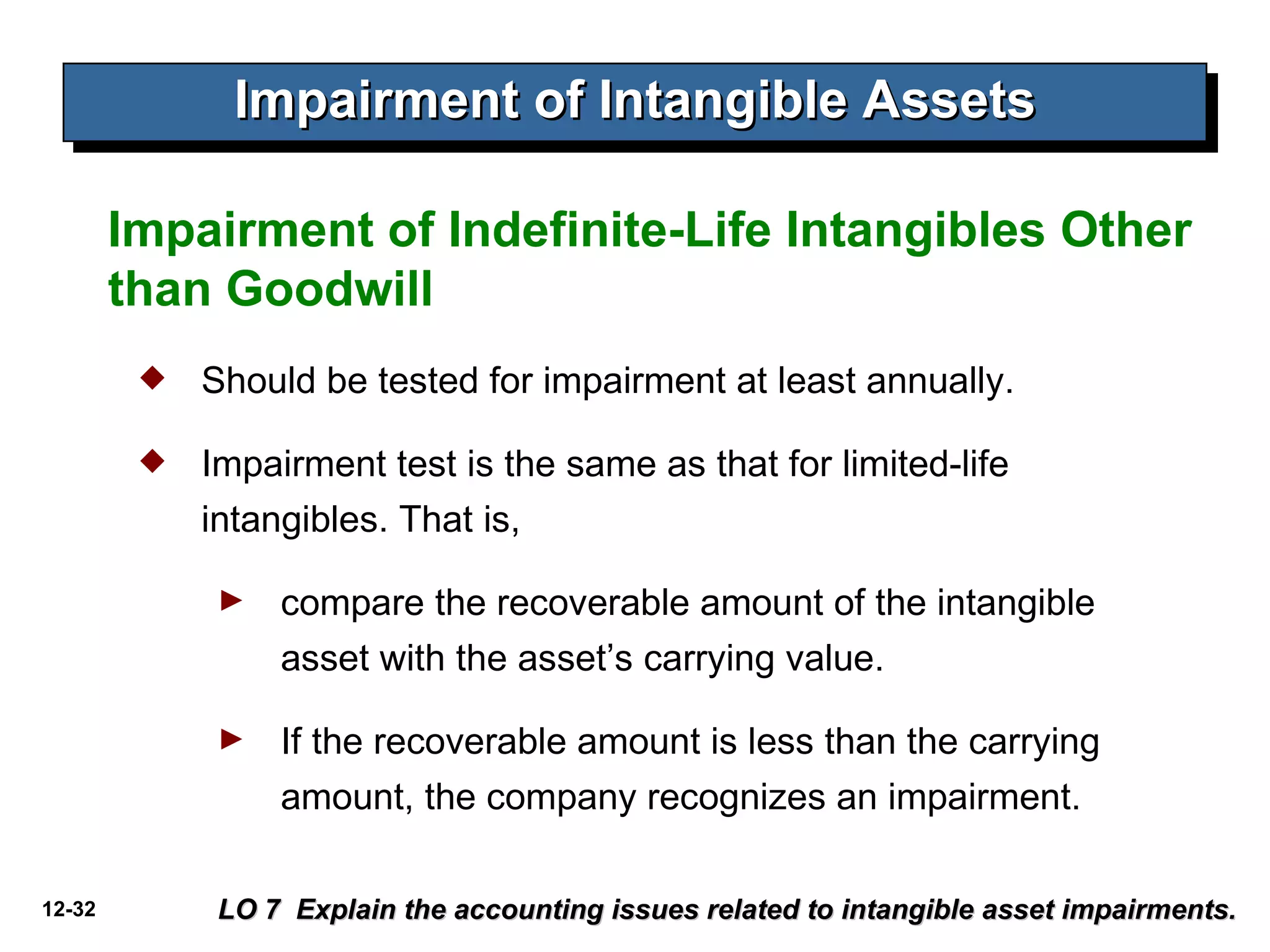

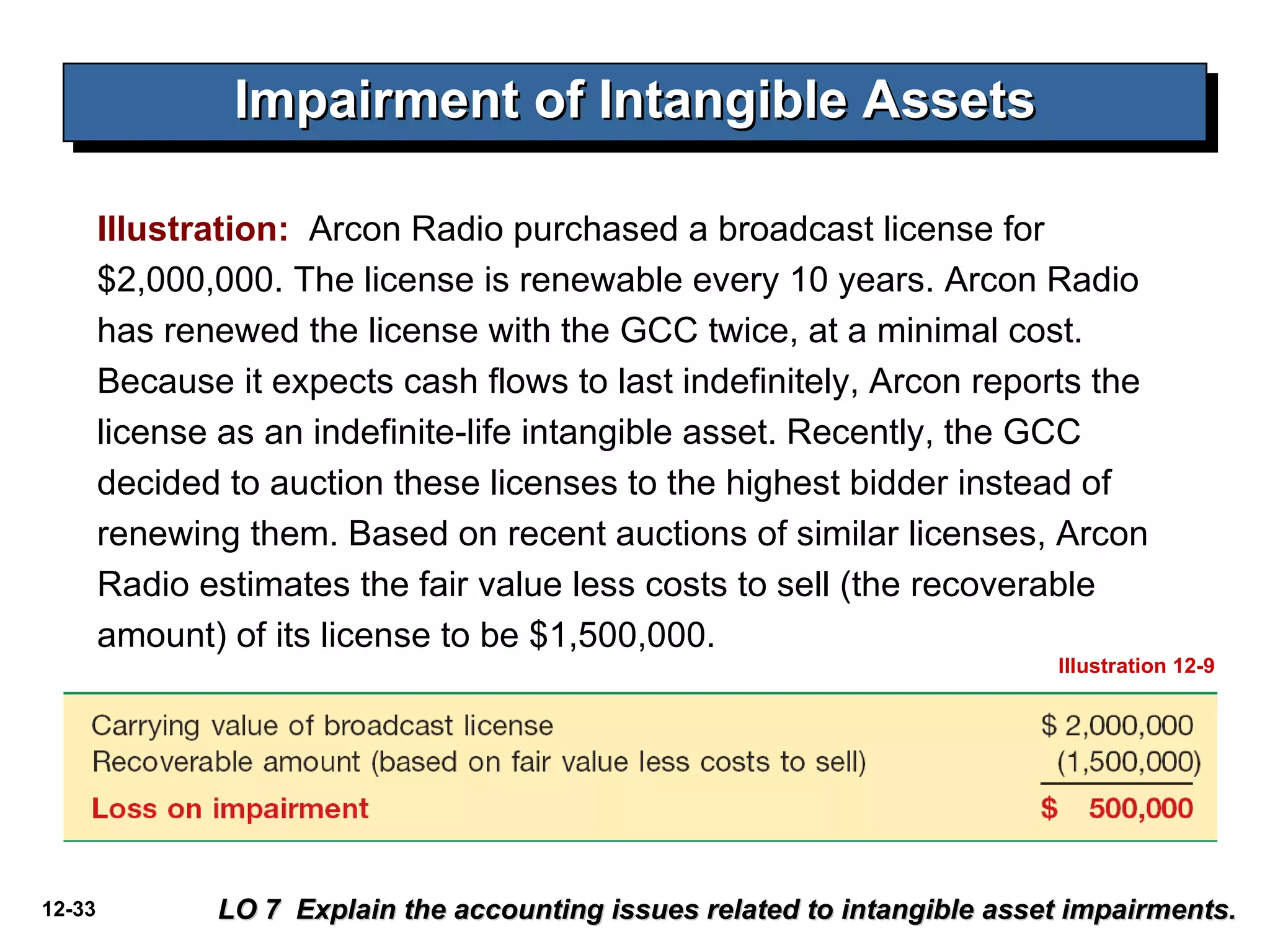

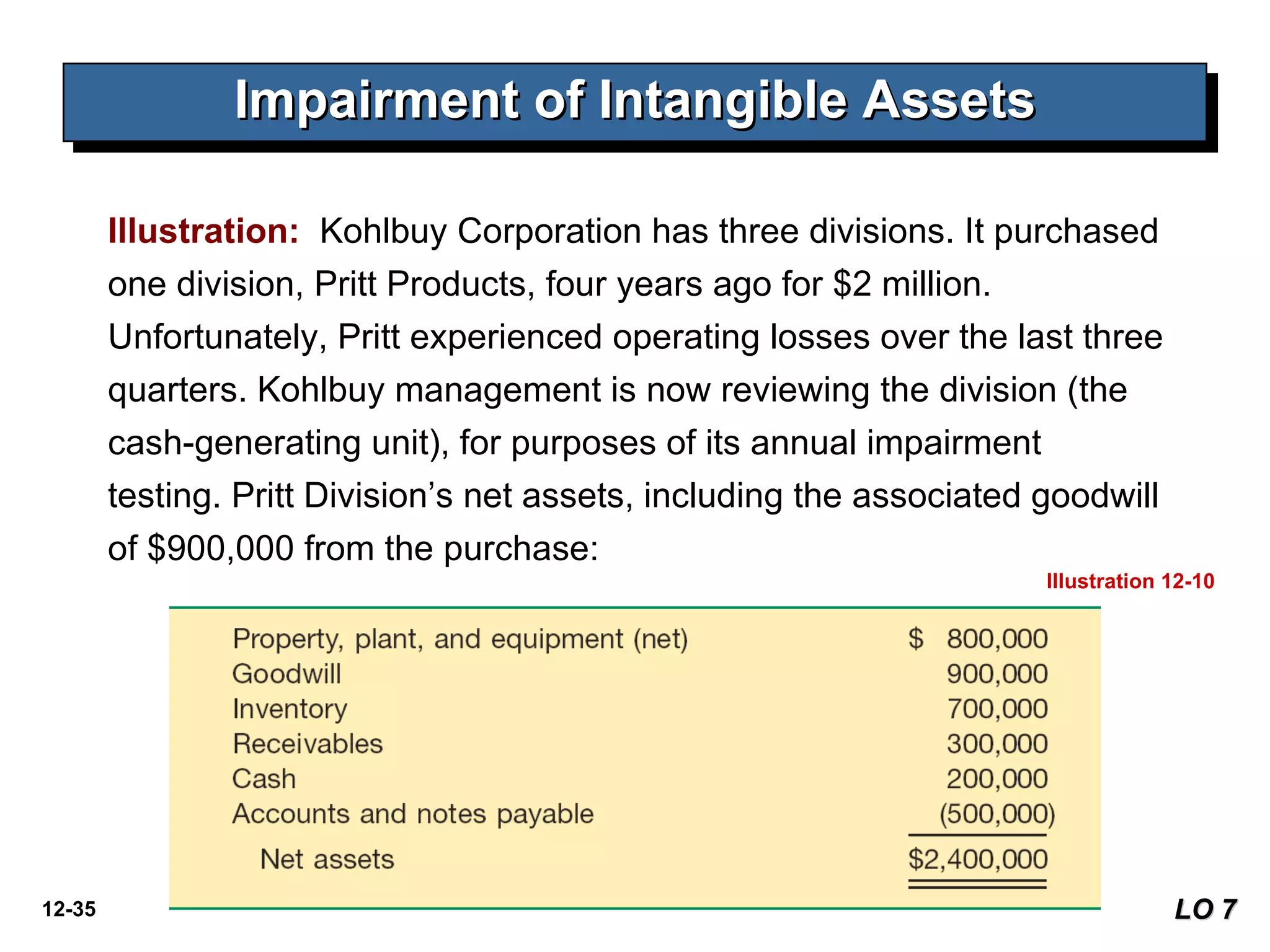

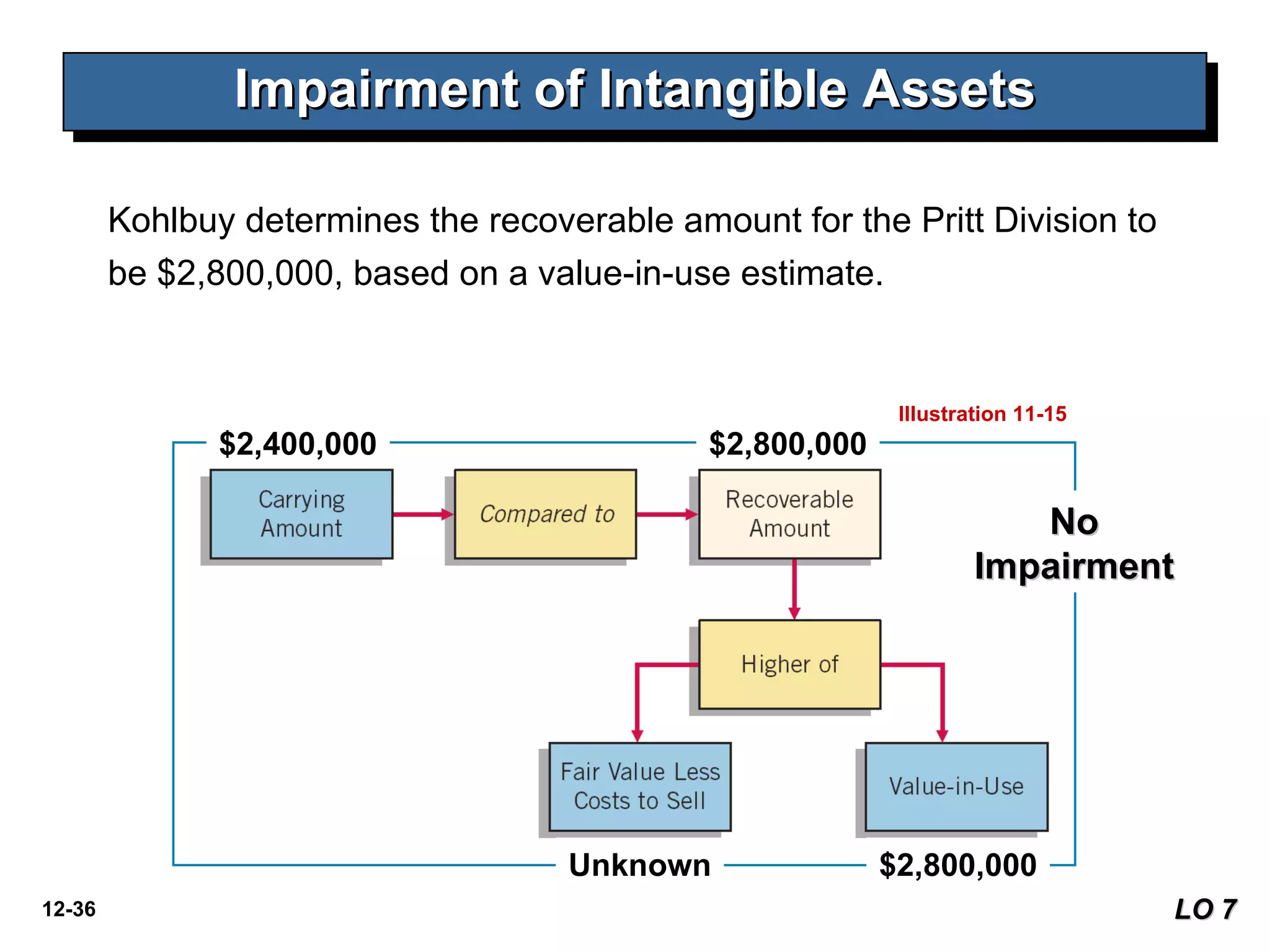

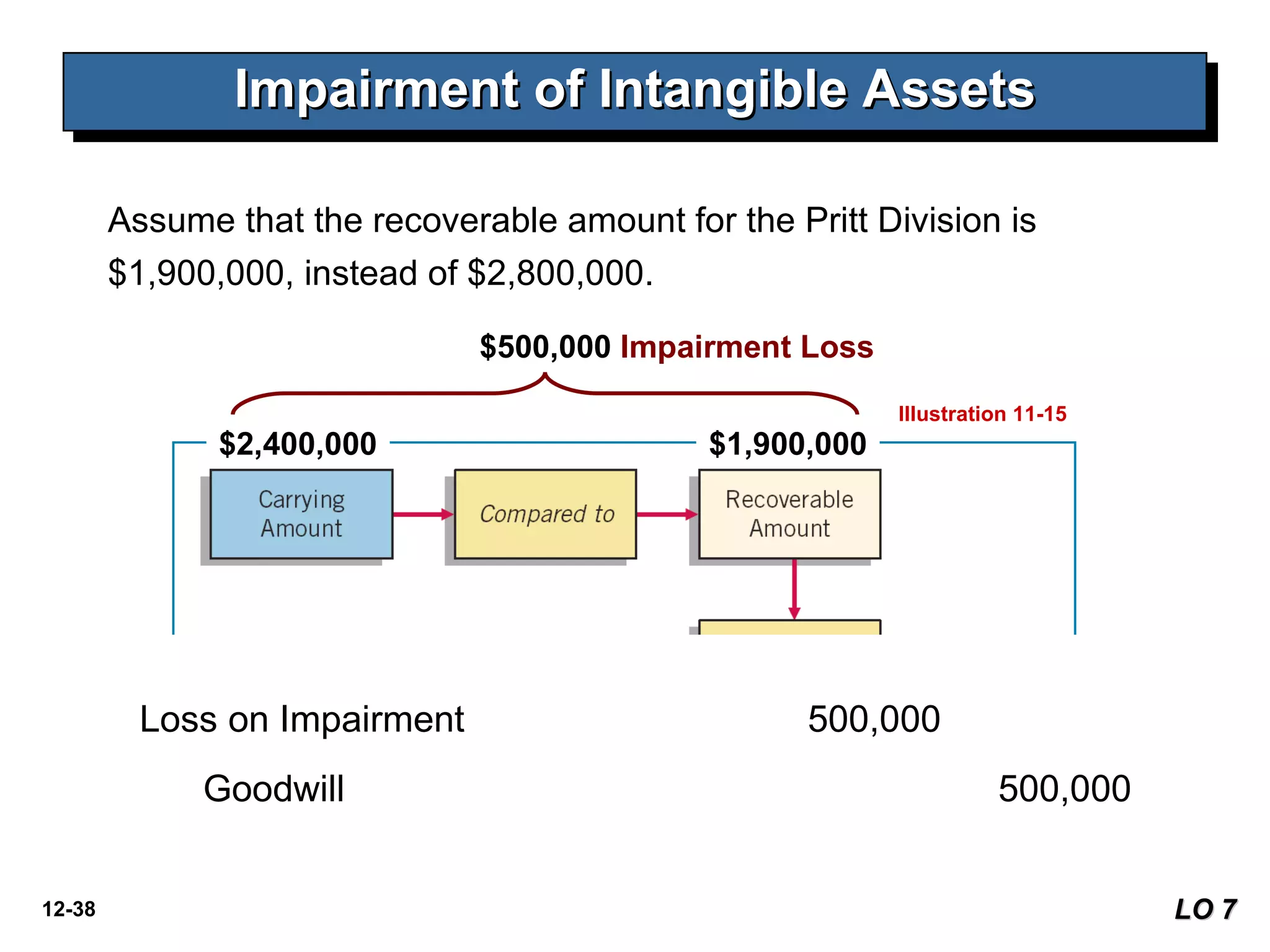

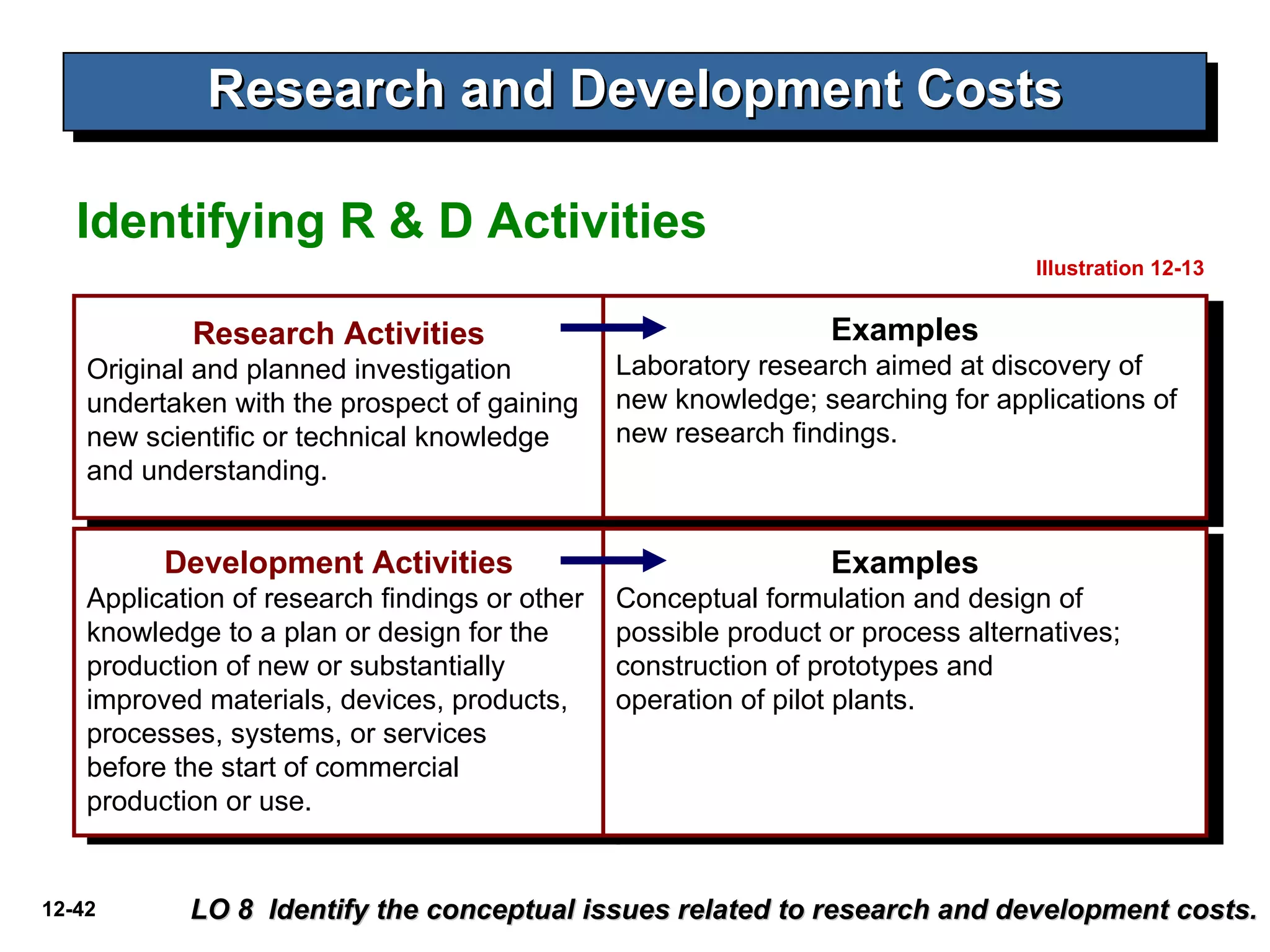

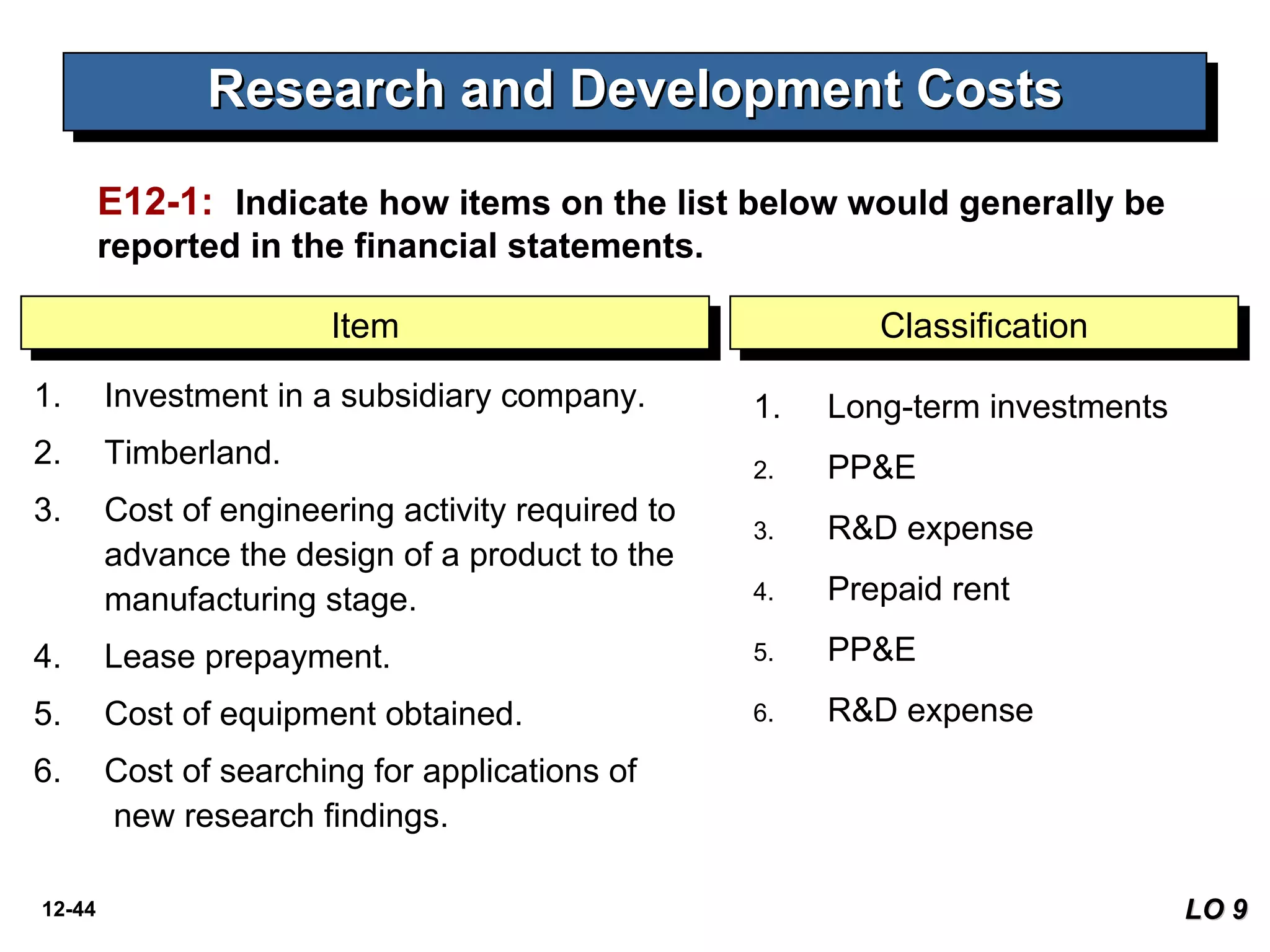

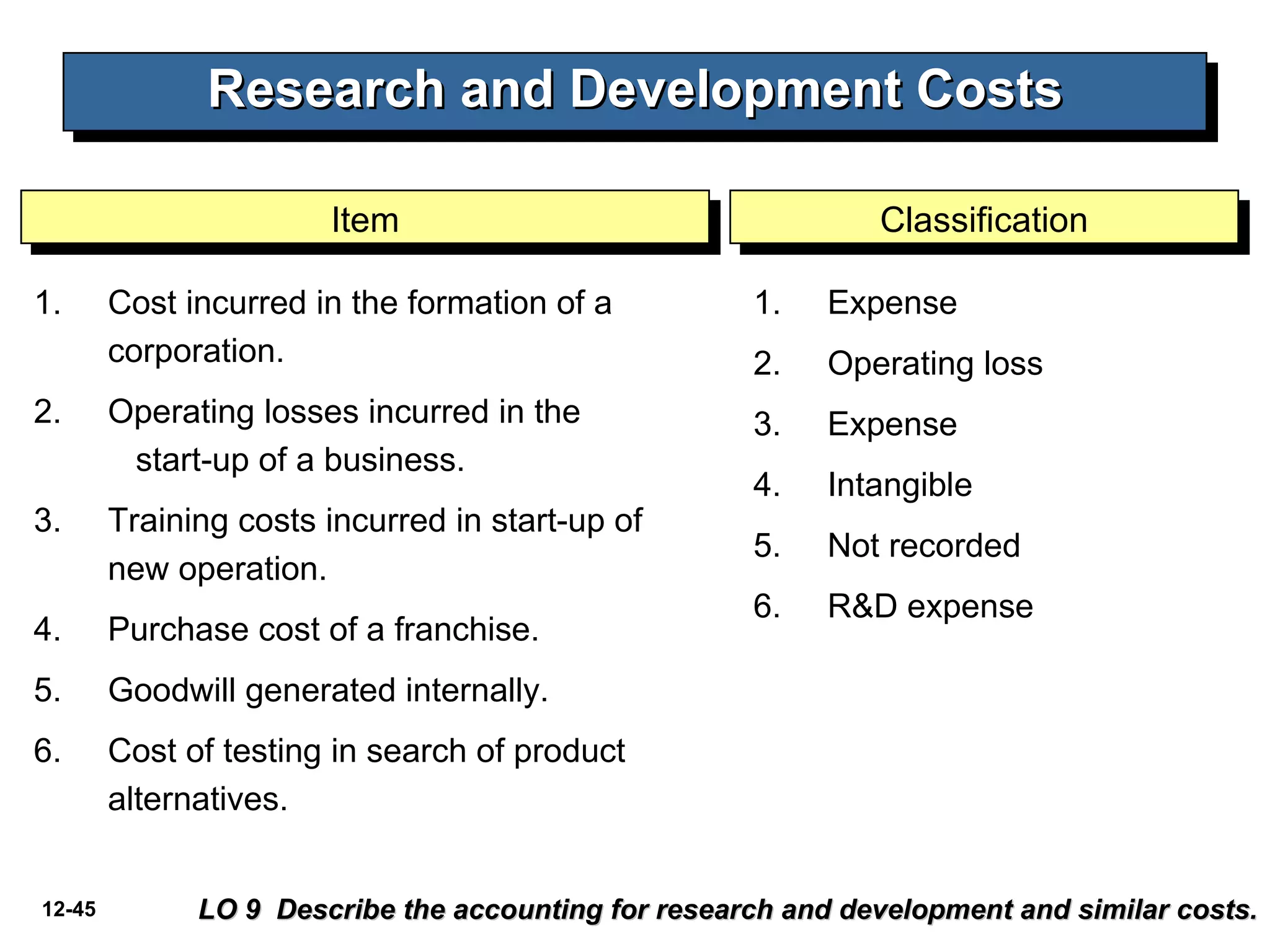

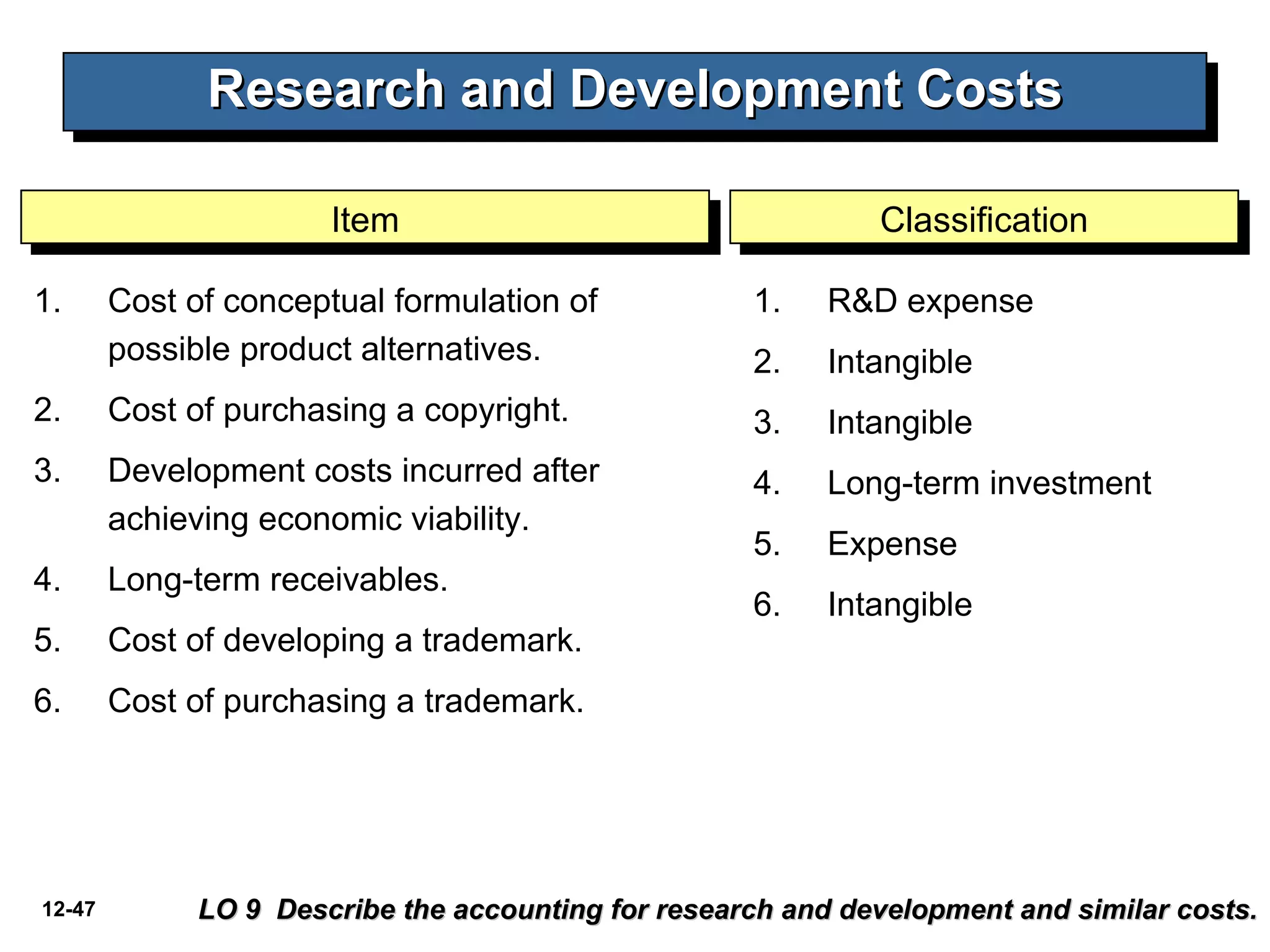

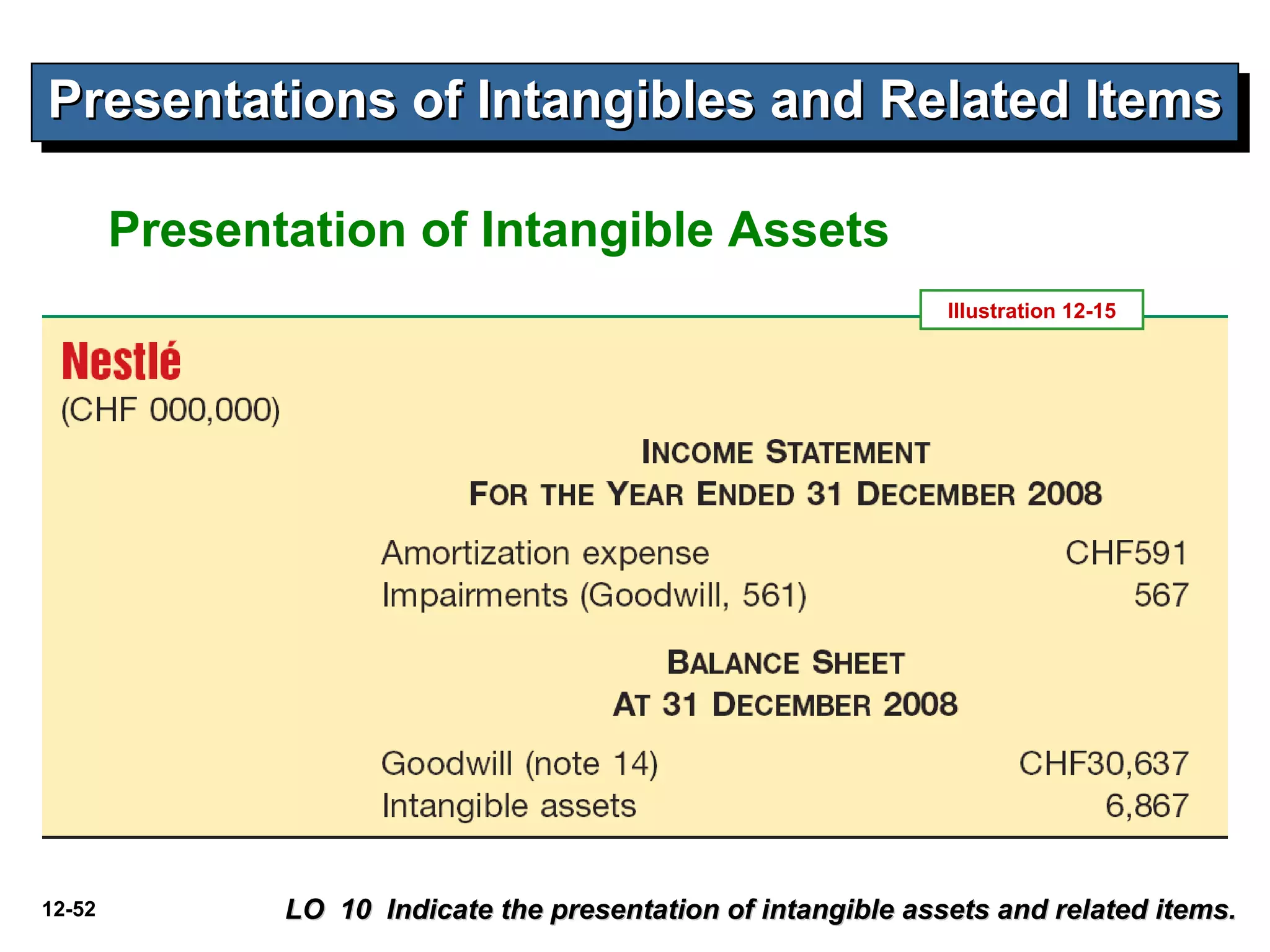

The document discusses accounting for intangible assets such as goodwill, patents, trademarks, and research and development costs. It describes characteristics of intangible assets, how to value and amortize them, types of intangibles including goodwill, procedures for recording goodwill, accounting for impairment of intangibles, conceptual issues and accounting treatment for research and development costs.