Downloaded 2,143 times

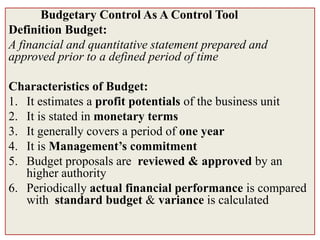

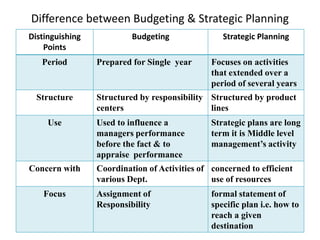

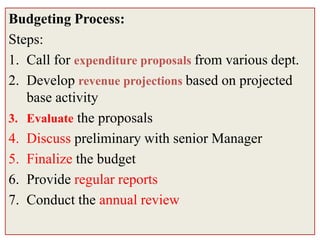

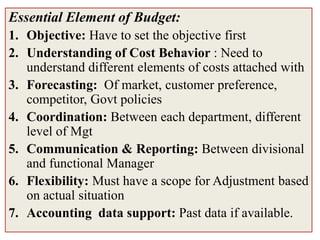

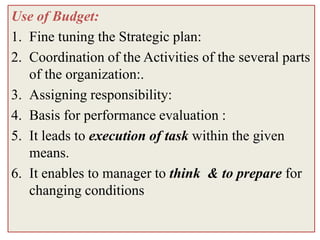

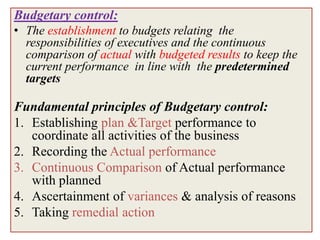

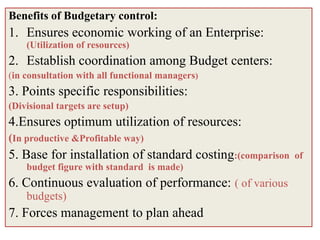

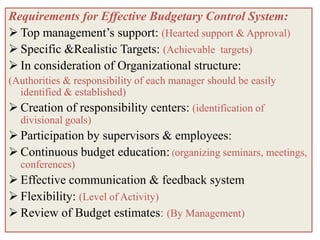

The document discusses budgeting and budgetary control. It defines a budget as a financial plan for a defined period. Budgets estimate profit potential, are stated in monetary terms, generally cover one year, and require management approval. The key aspects of budgets are setting objectives, understanding cost behavior, coordination, communication, flexibility, and accounting data support. Budgets are used for planning, coordination, responsibility assignment, performance evaluation, and adapting to changing conditions. Budgetary control involves establishing budgets, tracking actual performance, analyzing variances, and taking corrective actions.