Downloaded 811 times

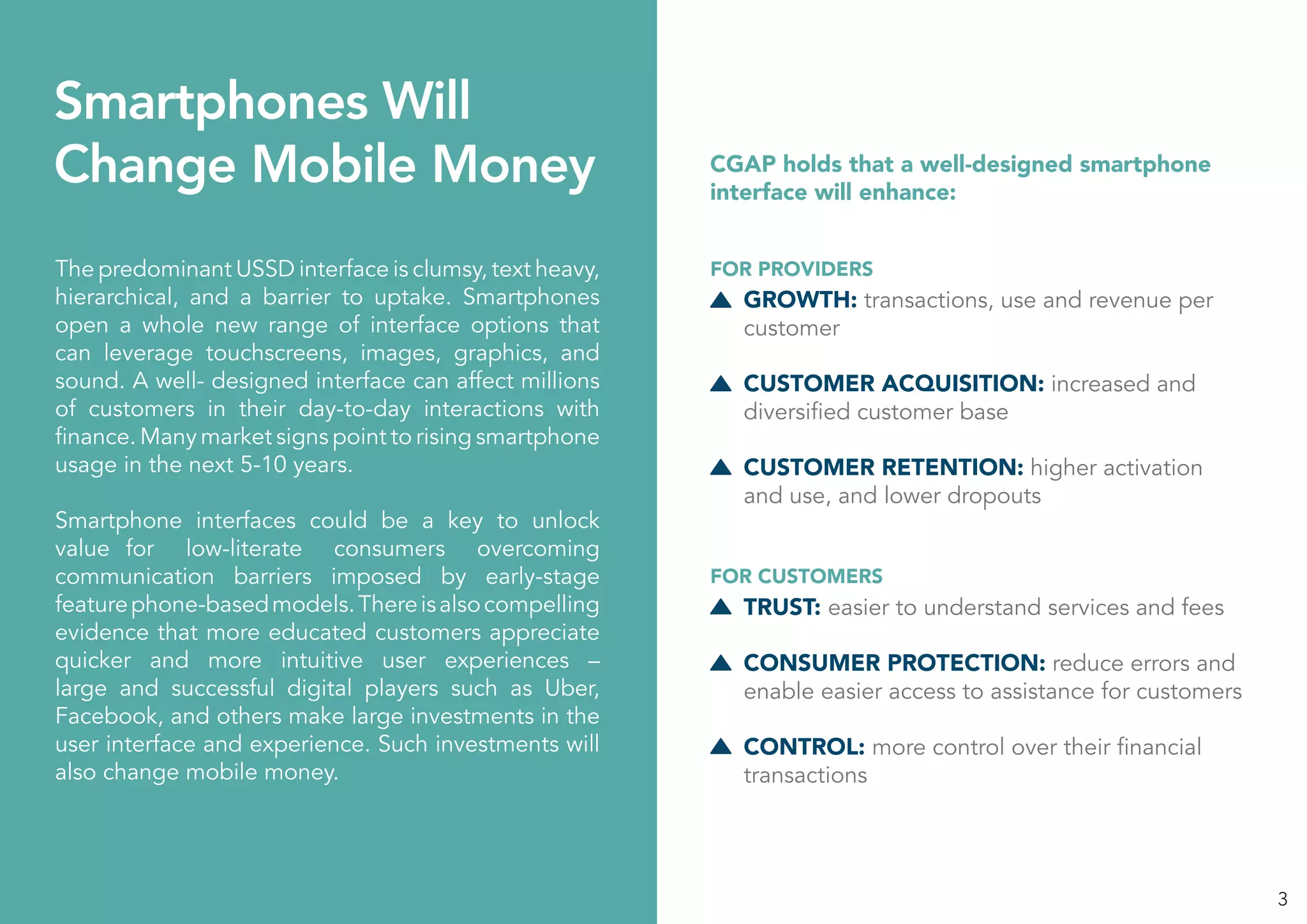

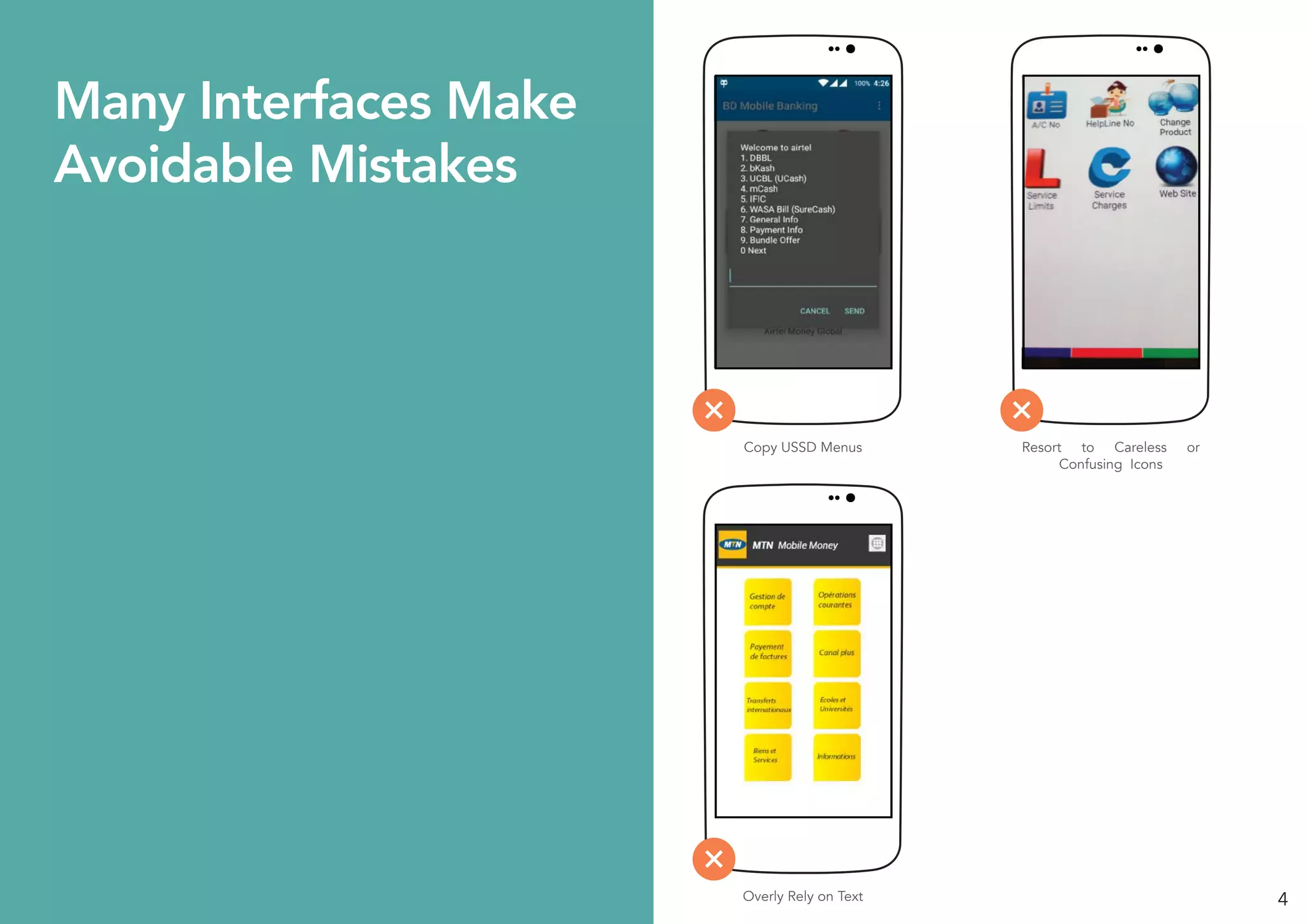

The document outlines key UI/UX design principles for mobile money services on smartphones, emphasizing the need for well-designed interfaces that can significantly enhance user experience, growth, and profitability. It stresses that smartphones can overcome barriers associated with traditional USSD interfaces and leverages user-friendly features such as simplified navigation and visual cues to improve customer interaction. The principles presented are intended for basic mobile money functions, particularly in low-income countries, and serve as a foundation for further enhancements in mobile money applications.