Download as PDF, PPTX

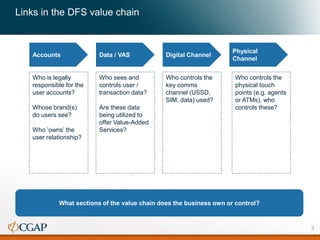

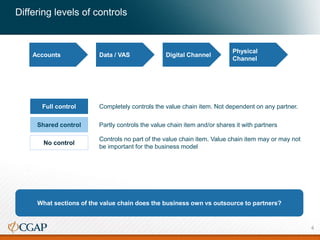

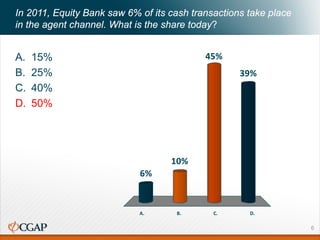

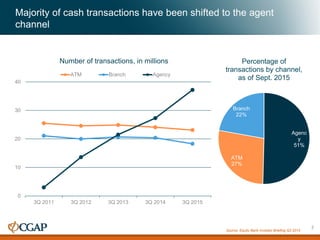

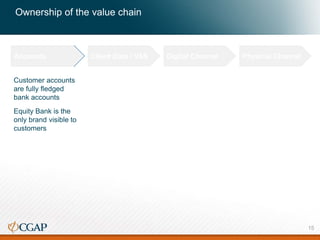

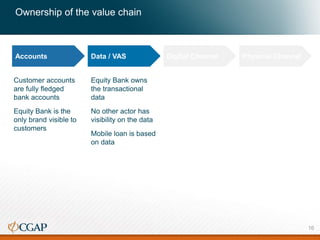

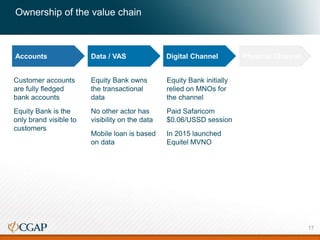

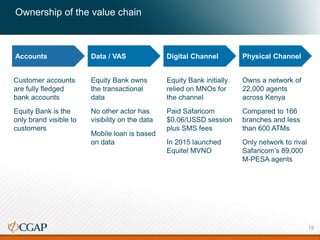

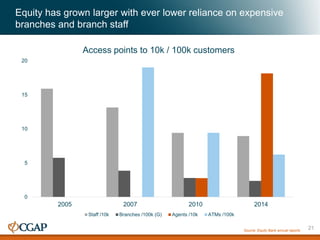

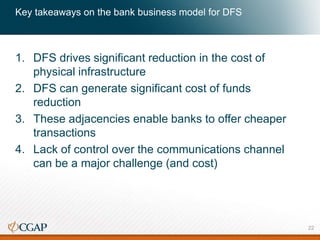

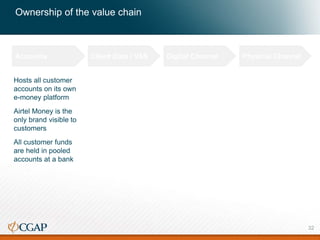

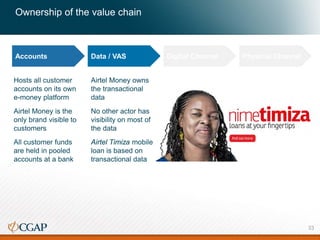

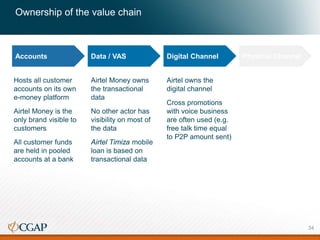

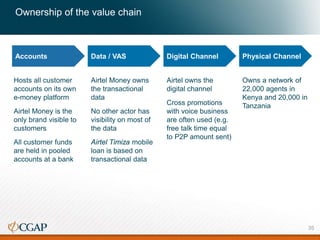

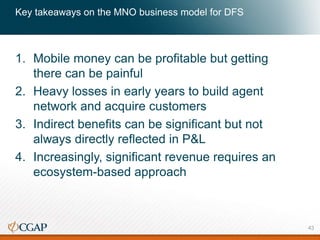

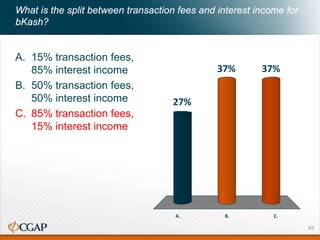

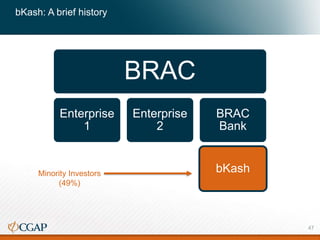

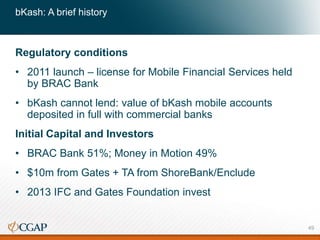

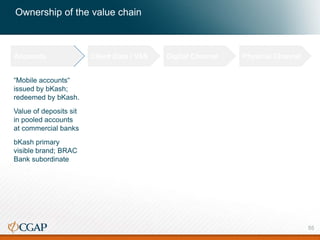

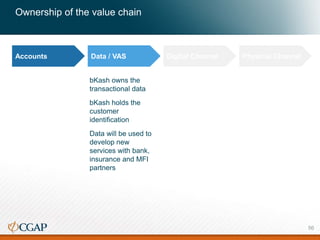

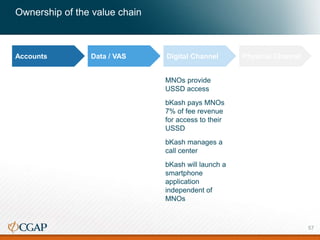

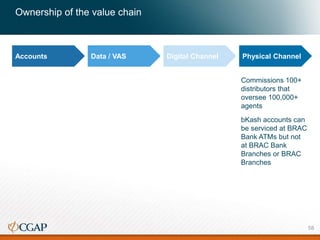

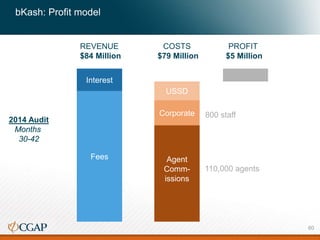

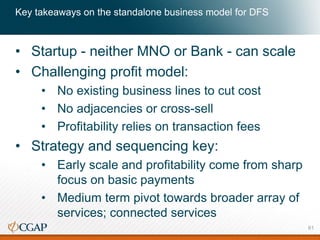

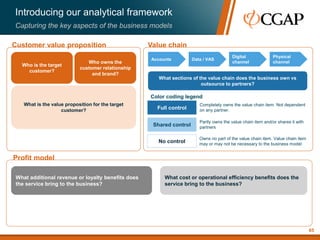

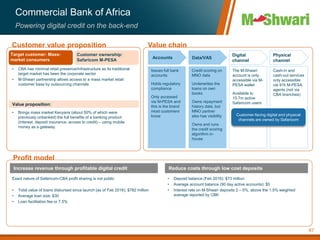

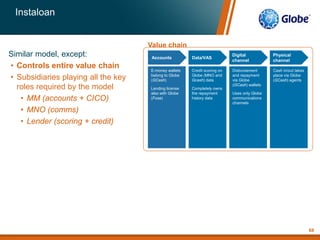

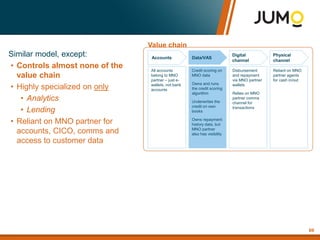

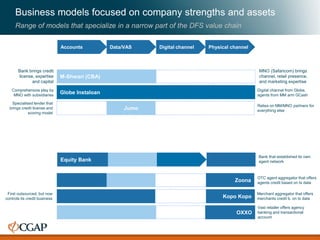

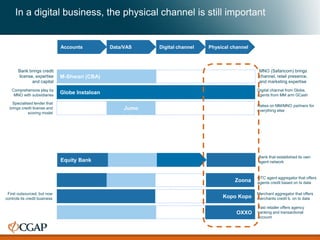

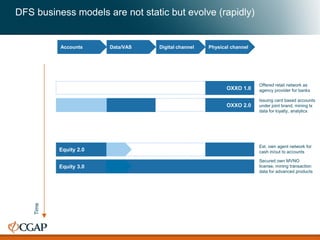

The document discusses different business models for digital financial services (DFS). It analyzes the bank model using Equity Bank as an example, the mobile network operator (MNO) model using Airtel Money, and the standalone model using bKash. For each model, it examines ownership and control over various parts of the DFS value chain including accounts, data, digital and physical channels. It finds that the bank model has the most control while the MNO model relies on partnerships. The standalone model falls between the two.

![Open banking [Evolution, Risks & Opportunities]](https://cdn.slidesharecdn.com/ss_thumbnails/openbanking-210606160258-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Slides] Digital Transformation, with Brian Solis](https://cdn.slidesharecdn.com/ss_thumbnails/slidesdigitaltransformationbriansolis-140429142804-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)