Digital Financial Services: Key Concepts

•

4 likes•5,277 views

Attendees to a workshop hosted by CGAP voiced their opinions on different topics related to digital finance.

More Related Content

What's hot

What's hot (20)

Similar to Digital Financial Services: Key Concepts

Similar to Digital Financial Services: Key Concepts (20)

More from CGAP

More from CGAP (20)

Recently uploaded

Recently uploaded (20)

Digital Financial Services: Key Concepts

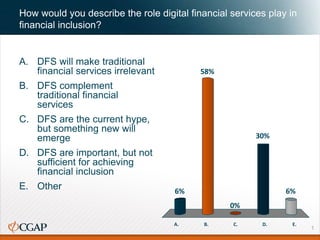

- 1. How would you describe the role digital financial services play in financial inclusion? A. DFS will make traditional financial services irrelevant B. DFS complement traditional financial services C. DFS are the current hype, but something new will emerge D. DFS are important, but not sufficient for achieving financial inclusion E. Other 1 A. B. C. D. E. 6% 58% 6% 30% 0%

- 2. What is your main motivation for attending this event? A. I would like to know what others are doing in DFS B. I would like to learn about the latest trends in DFS C. I would like to know more about what funders can do to support DFS D. I want to learn the basics – this is completely new to me E. I wanted to come to Paris F. Other 2 A. B. C. D. E. F. 7% 20% 7% 10% 3% 53%

- 5. Digital Financial Services “Branchless Banking” “Mobile money” “Internet Banking” “Mobile financial services” Financial services delivered over a digital channel (mobile, internet) using any electronic instrument (card, phone, computer) Accounts, products and services can be accessed remotely (outside a physical branch or outlet) Mobile Financial Services Digital Financial Services 3

- 6. FSP Agent Client The basic DFS model

- 7. FSP Client The basic DFS model: Cash-in Client opens DFS account (accessible by POS or phone) Agent opens DFS account (accessible by POS or phone) 2 Cash-in 3 Agent account debited Client account credited 1 1 - + Agent

- 8. FSP Client The basic DFS model: Cash-out 2 Cash-out Agent 1 Agent account credited Client account debited- +

- 9. Key terms: E-money Standarddefinition Closed-loop store cards are not e- money • Monetary value represented by a claim on an issuer • Electronically stored (on a server or–rarely–a card) and exchanged • Widely accepted means of payment by others than the issuer • Can be redeemed as cash Stored value accounts also fit the definition E-money accounts can be issued by non-banks. They are regulated more lightly than bank products.

- 10. Key terms: Agents • Offer services on behalf of the provider • Are separate entities—not provider staff • Provider typically fully liable for agent • This liability cannot be contracted away • Usually have different core businesses • Often small retailers or airtime vendors • In advanced markets, dedicated agents exist • Transact against own funds in real time • Don’t at any point hold customers’ cash

- 11. Verify client identity • Comply with KYC standards • Guard against fraud Help clients transact • Cash-in and cash-out • OTC payment transactions Act as face of the service • Sign up clients • Educate clients about the service • Troubleshoot clients’ problems Agents fulfill 3 important functions in a DFS service

- 12. CGAP research on the activity rate of customers registered by best vs. worst agents Agents are central to the success of the business Providers often focus on agent quantity, but agent quality is more important: • If agents are weak, customers will not use the service • Registering inactive customers is only a drain on the business Top 20% of agents by # of registrations Top 10% by activity rate Bottom 10% by activity rate Top10%Bottom10% Activity Rate Customers registered by these agents make up 5.7% of total customers Activity Rate 39.9% 0.9% Profile of customers registered by these agentsAll Agents Top 20% of agents by # of registrations Customers registered by these agents make up 5.1% of total customers

- 13. Why are DFS transformative?

- 14. Traditional financial services are inaccessible to the poor 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% World Developing countries Of adults earning <$2 /day Global financial inclusion Excluded Included Source: World Bank Findex 2012

- 15. Why are traditional financial services inaccessible to the poor? 1. High cost of bank branches Branch infrastructure is small & heavily urban 2. High documentation requirements Large share of population cannot qualify Illiterate clients often excluded 3. Low income clients find banks intimidating Products, experience not designed for them Often prefer more familiar informal services 4. Most banks don’t want low-income clients Opening and monthly fees, minimum balances, etc. DFS models help overcome them all

- 16. Technology dramatically lowers cost of outreach *Includes costs for physical set up (e.g. brick and mortar branches, hardware) only. 1 Lower cost translates directly to larger scale

- 17. Case in point: Financial infrastructure in Kenya Bank branches have been built over the past 100+ years. Today, there are 1,200+ bank branches in Kenya.

- 18. Case in point: Financial infrastructure in Kenya The ATM network has been built over the past 24 years. Today, there are 2,300+ ATMs in Kenya.

- 19. Case in point: Financial infrastructure in Kenya Today, there are 120,000+ DFS agents in Kenya. DFS agent networks has been built over the past 7 years. Low cost of infrastructure translates to high access.

- 20. The same goes at the global level Points of presence for traditional financial services…

- 21. The same goes at the global level …are dwarfed by mobile phone connections. 6,800,000,000 Mobile Phone Connections Source: GSMA Wireless Intelligence

- 22. Risk-based KYC has lowered documentation requirements It now aligns with what most people actually have …in return for restricting those accounts: • Limited maximum balances • Limited transaction amounts • Limited types of transactions Bank High DFS Low DFS Basic details Y Y Y National ID Y Y - Proof of address Y - - Regulators are allowing lower Know-Your-Customer (KYC) requirements for DFS accounts: 2 Ghana Low DFS: • $300 • $100/day • $1,000/month Endorsed by global standard setting bodies and watchdogs for Anti-Money Laundering and Combating Funding for Terrorism (AML/CFT) Changes as ID systems improve Y

- 23. Mohammad Moniruzzaman, 2009 CGAP Photo Contest Local agents are far more inviting to poor people • Less formal • No paperwork • No queues • Familiar setting • Often known in the community • Agent is a peer 3

- 24. Distribution of agent transactions by day of the week and hour % of total transactions within a sample of agents Mon Tue Wed Thu Fri Sat Sun 10 2 3 4 5 6 108 12 14 16 18 20 2221 2397 11 13 15 17 19 22.6% 36.0%1.2% 40.2% Business hours at Agent Partner Business hours at bank branch network Agents are also more accessible and convenient Source: Akya/CGAP analysis; Note: Based on sample of 3,961 transactions

- 25. This isn’t about charity or CSR but real business (and that’s great) Source: GSMA MMU State of the Industry 2015

- 26. …and this is with a single use case! DFS has been primarily centered on domestic remittances (and airtime) DFS are evolving to become considerably more than that

- 27. Advancing financial inclusion to improve the lives of the poor www.cgap.org