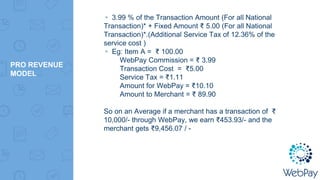

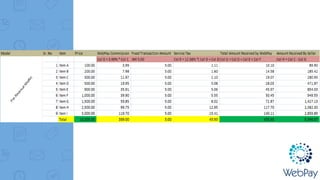

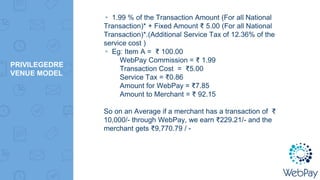

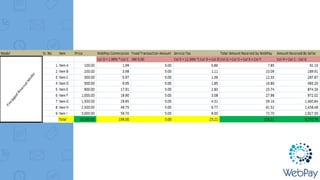

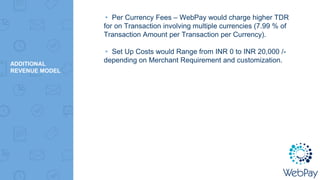

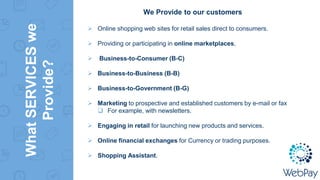

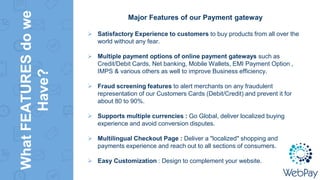

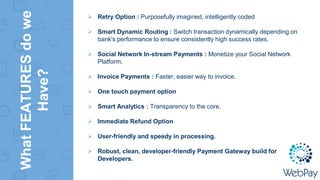

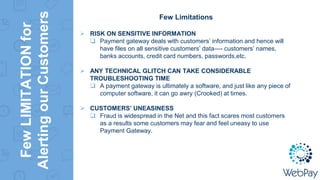

The document outlines the business plan for WebPay, a payment gateway service focused on providing secure, efficient electronic transaction solutions designed to empower small enterprises across India. It details the company's vision of being a trusted payments partner, showcasing its product features, market analysis, target customer segments, strategies for customer acquisition, and financial planning essentials. WebPay aims to navigate the evolving digital payment landscape while emphasizing security, customer experience, and market opportunities in a competitive environment.

![Market

Analysis

- Facts

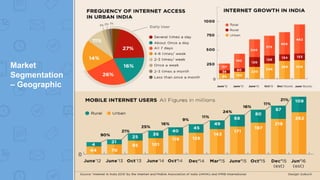

Digital Payments

Total Transaction Value [2016] – USD 28961.6 M

Expected Annual Growth Rate[2020] – 18.36% –USD 56837.5M

Why Now??](https://image.slidesharecdn.com/webpay-170410200339/85/Webpay-Payment-Gateway-Business-Plan-20-320.jpg)

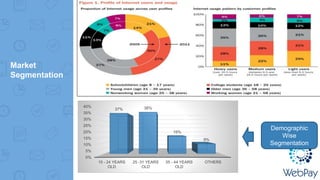

![Market

Analysis –

Segmentation

▸Segmenting Consumer Market [B2C]

▸Serving Customers directly in the form of Mobile App

▸Segmenting Business Market [B2B]

▸Partenring with

▸Bank

▸Online Shopping Sites

▸Local Merchants](https://image.slidesharecdn.com/webpay-170410200339/85/Webpay-Payment-Gateway-Business-Plan-23-320.jpg)