Downloaded 1,657 times

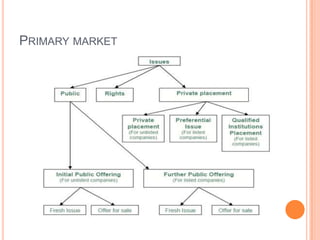

This document discusses capital structure and financial markets, specifically the primary market. It defines the primary market as the market for new issuers, where companies can directly issue shares, bonds, or other securities to raise capital. The document outlines the key participants and processes in the primary market in Nepal, including requirements for disclosure, underwriting, and issue procedures that must follow the Company Act and SEBON guidelines. Overall, the primary market provides an important channel for companies and governments to raise funds for investment and growth.