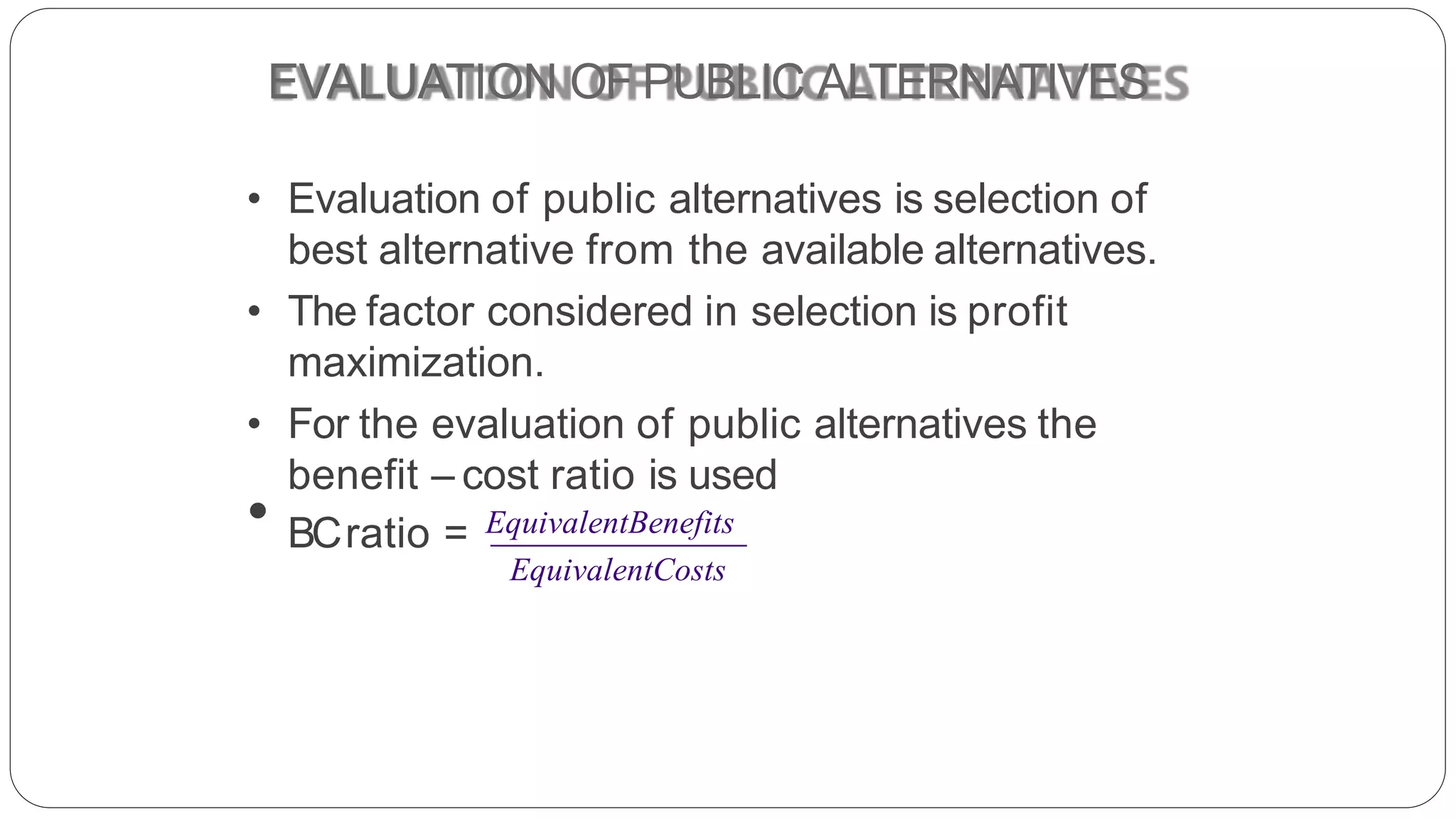

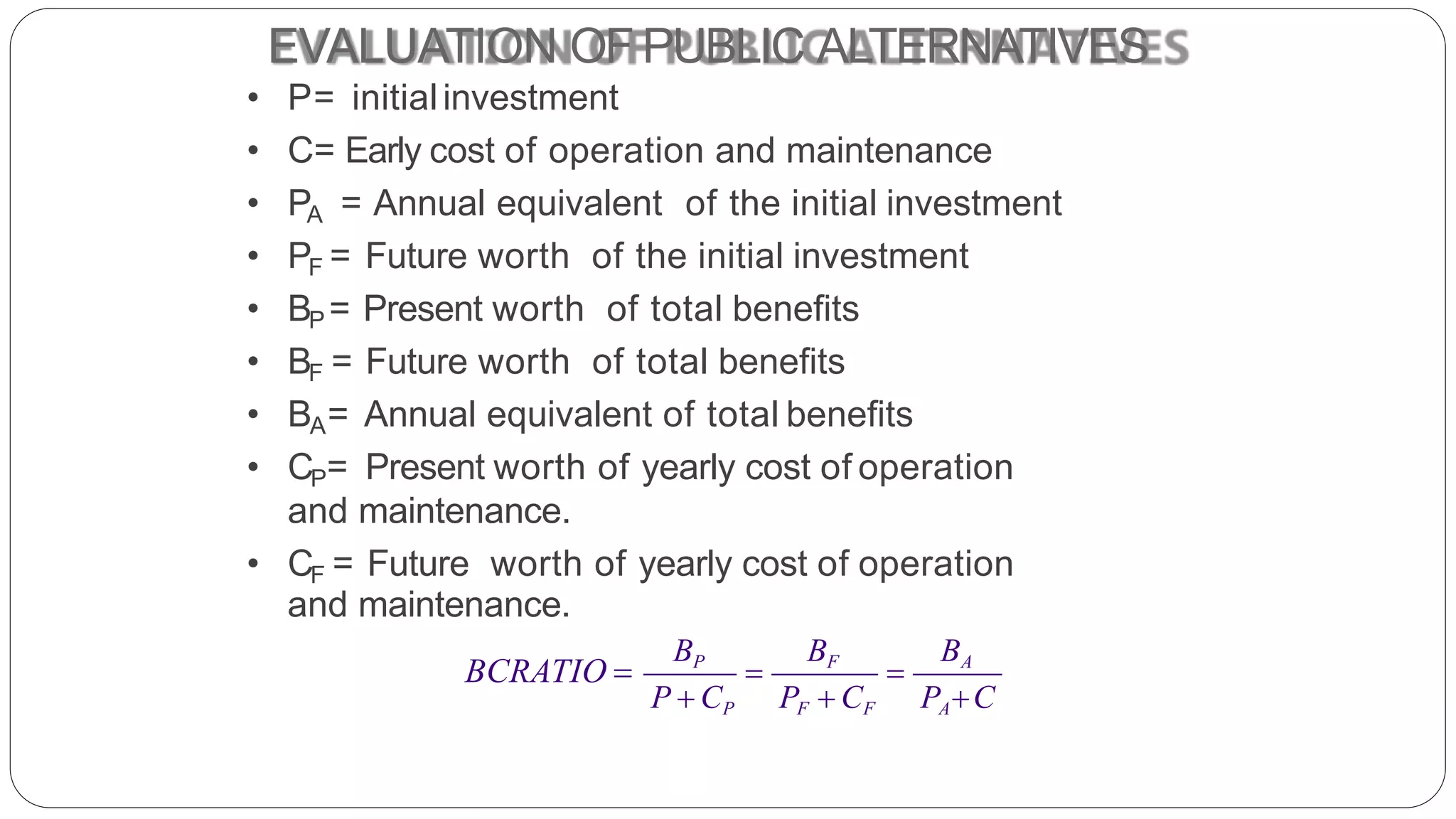

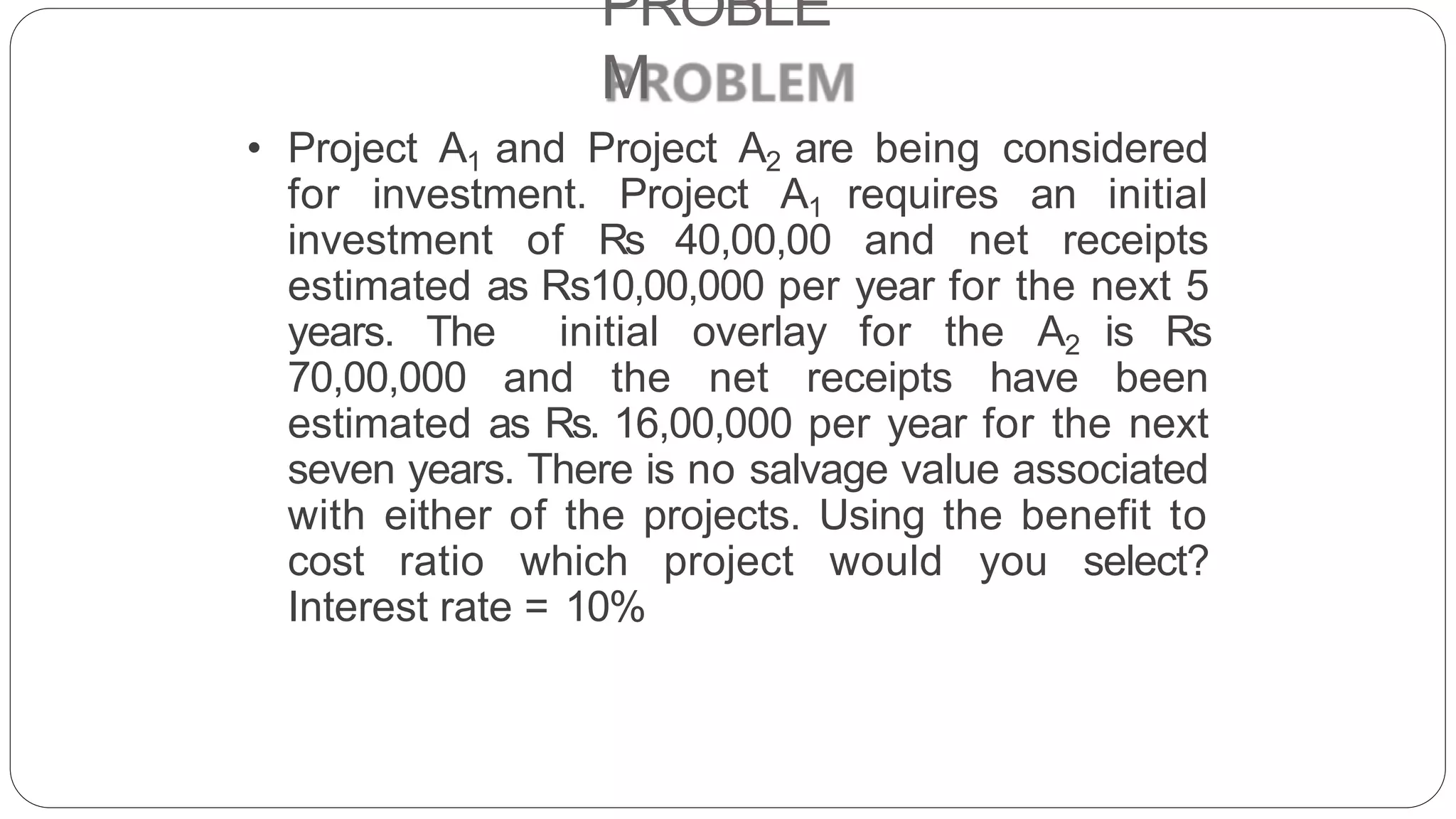

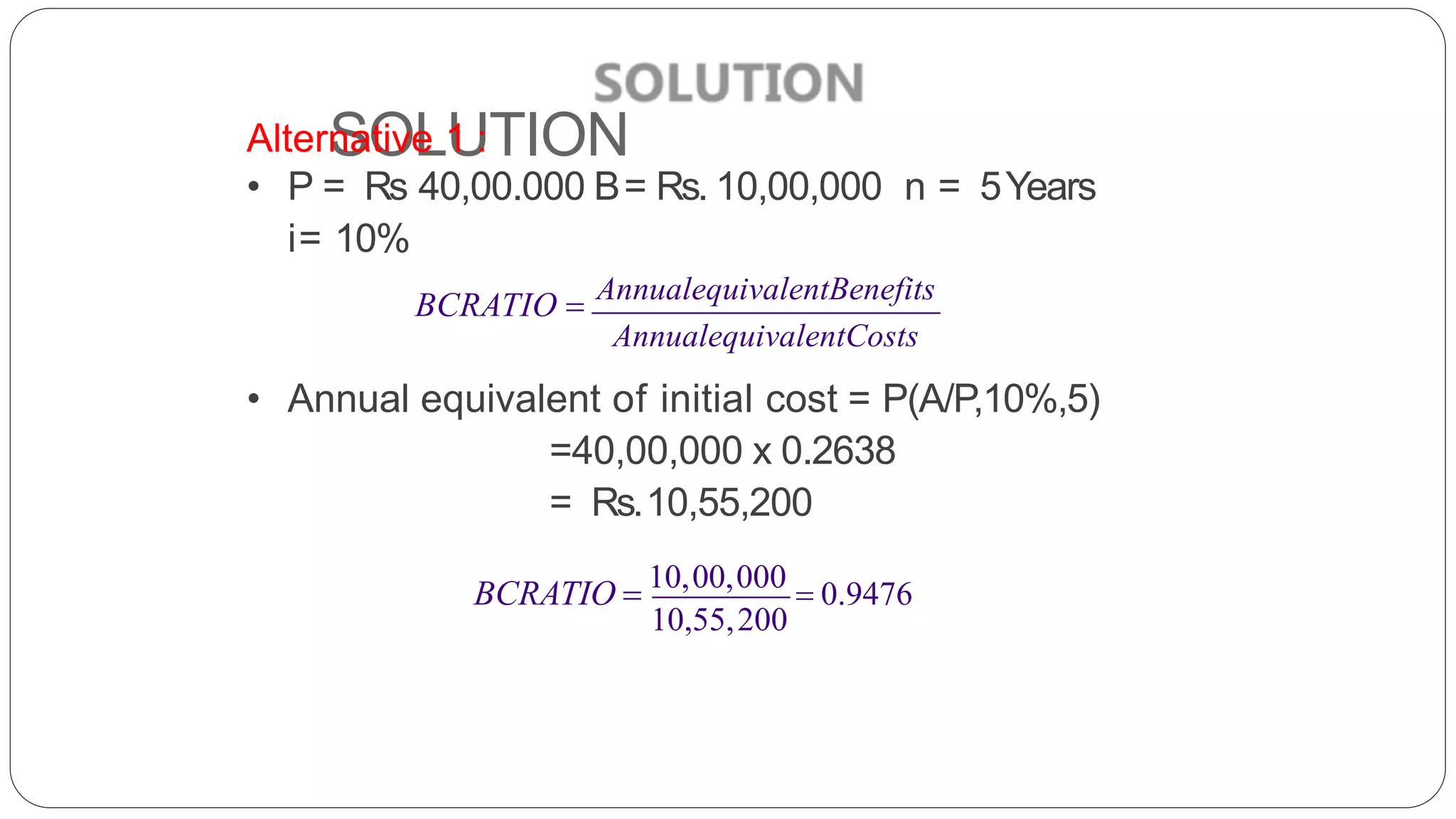

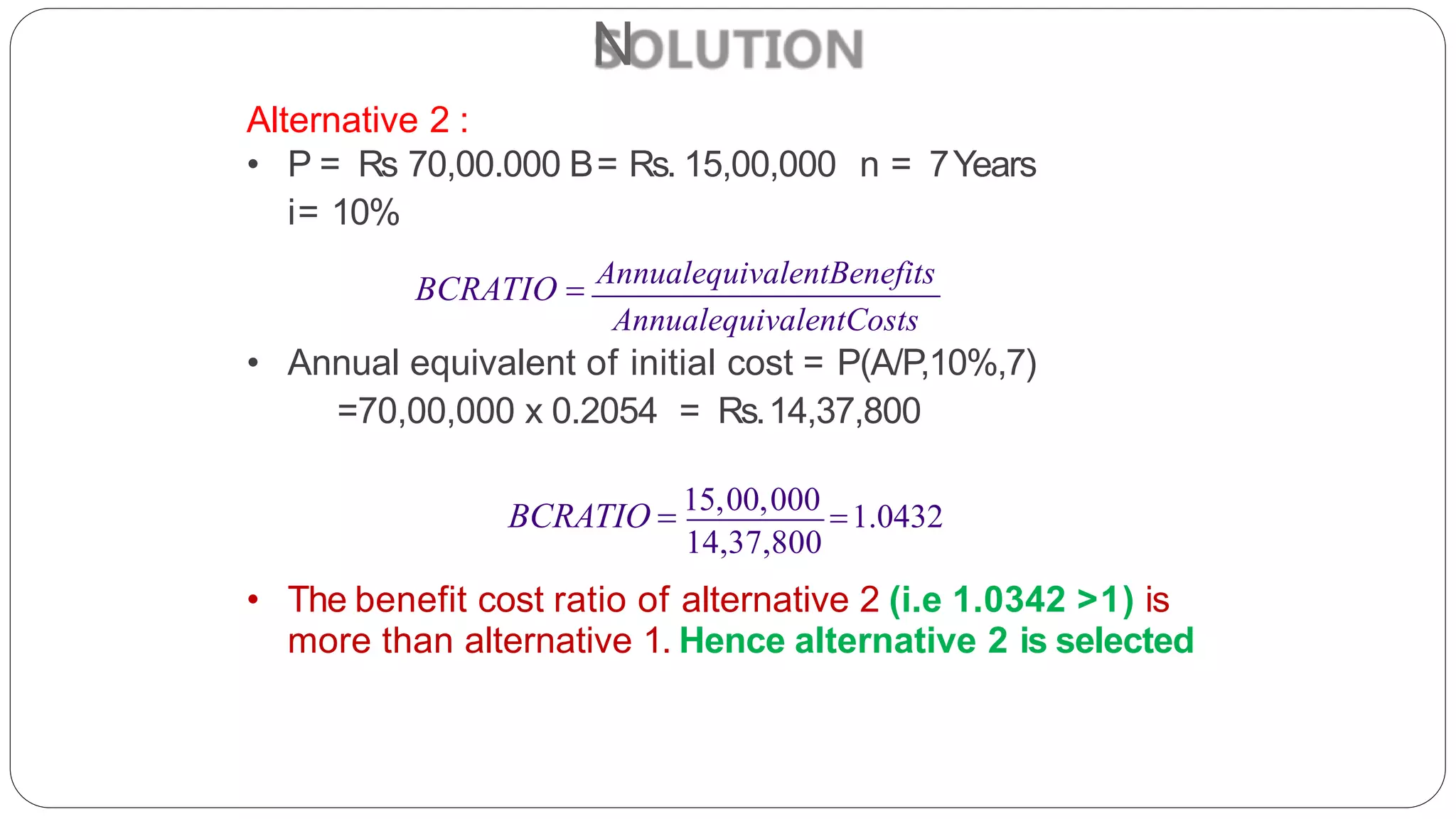

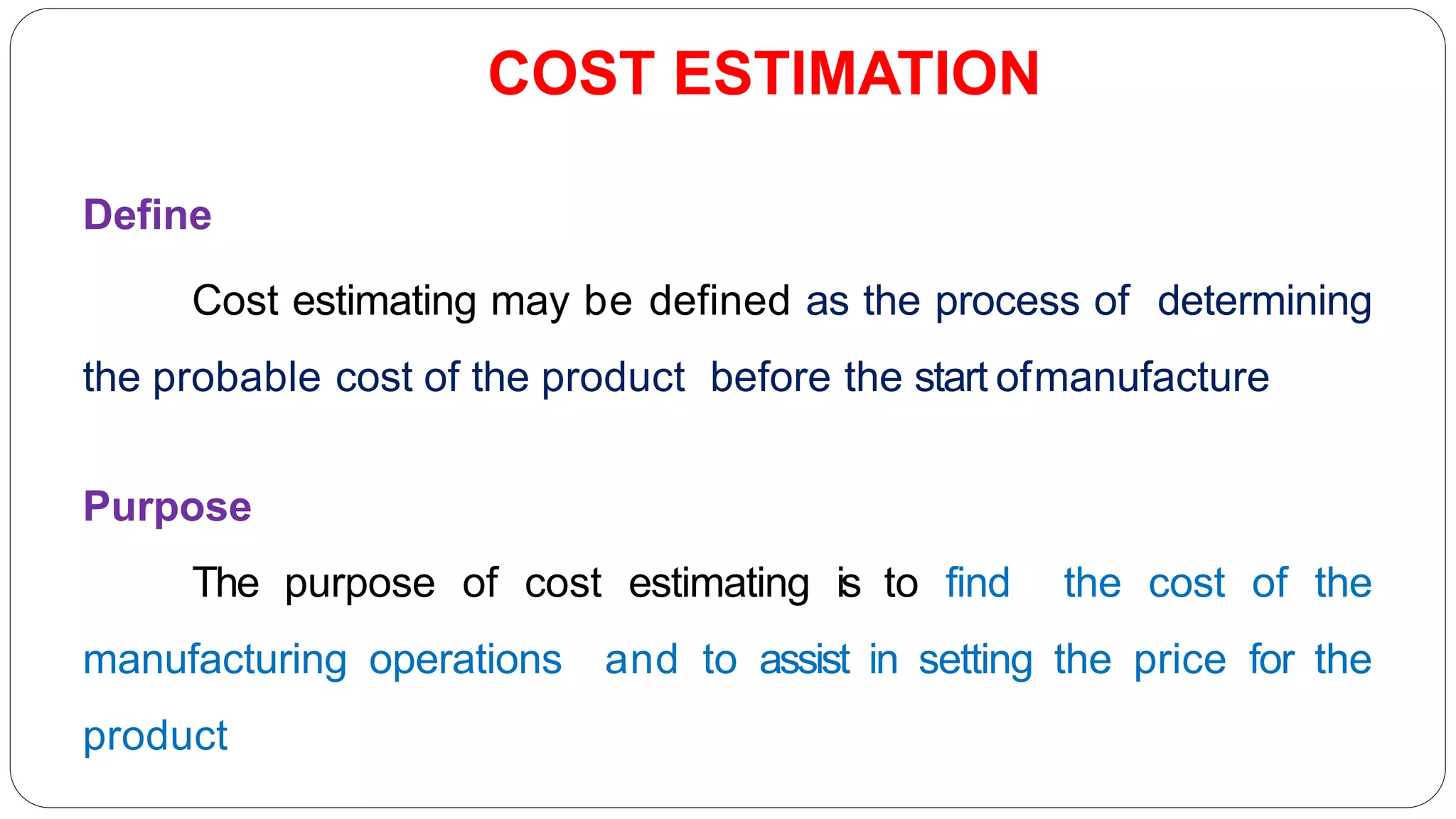

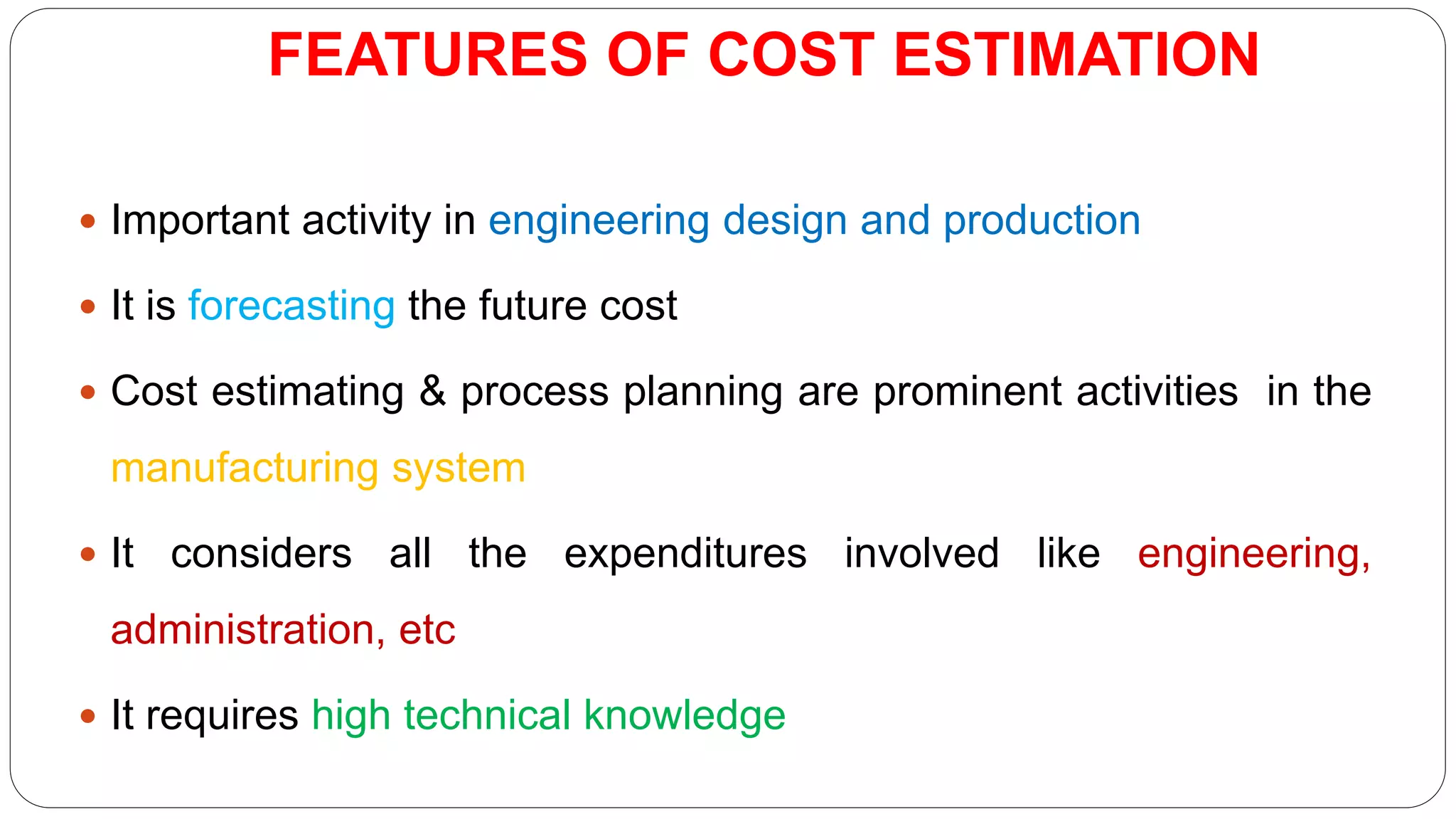

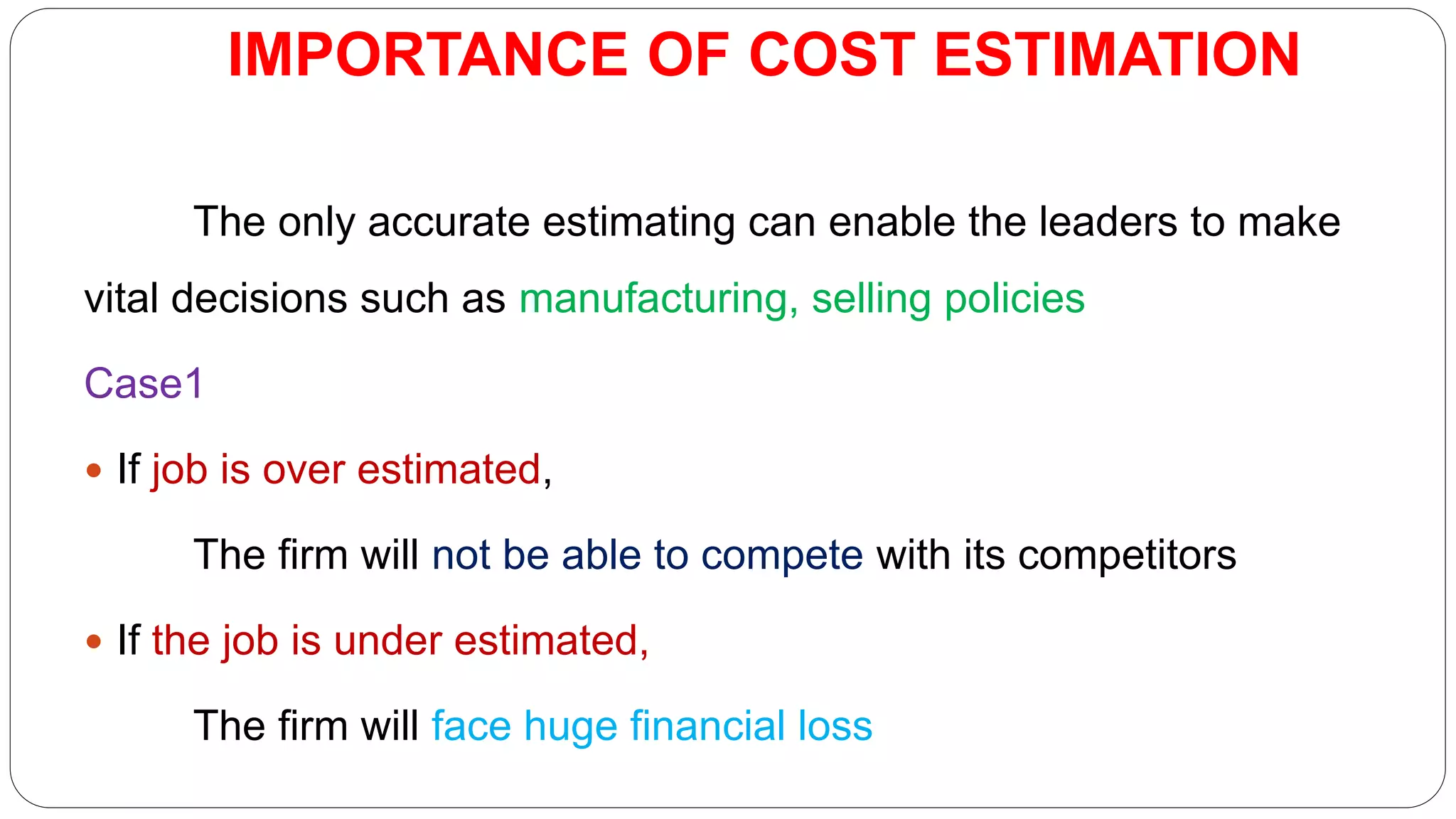

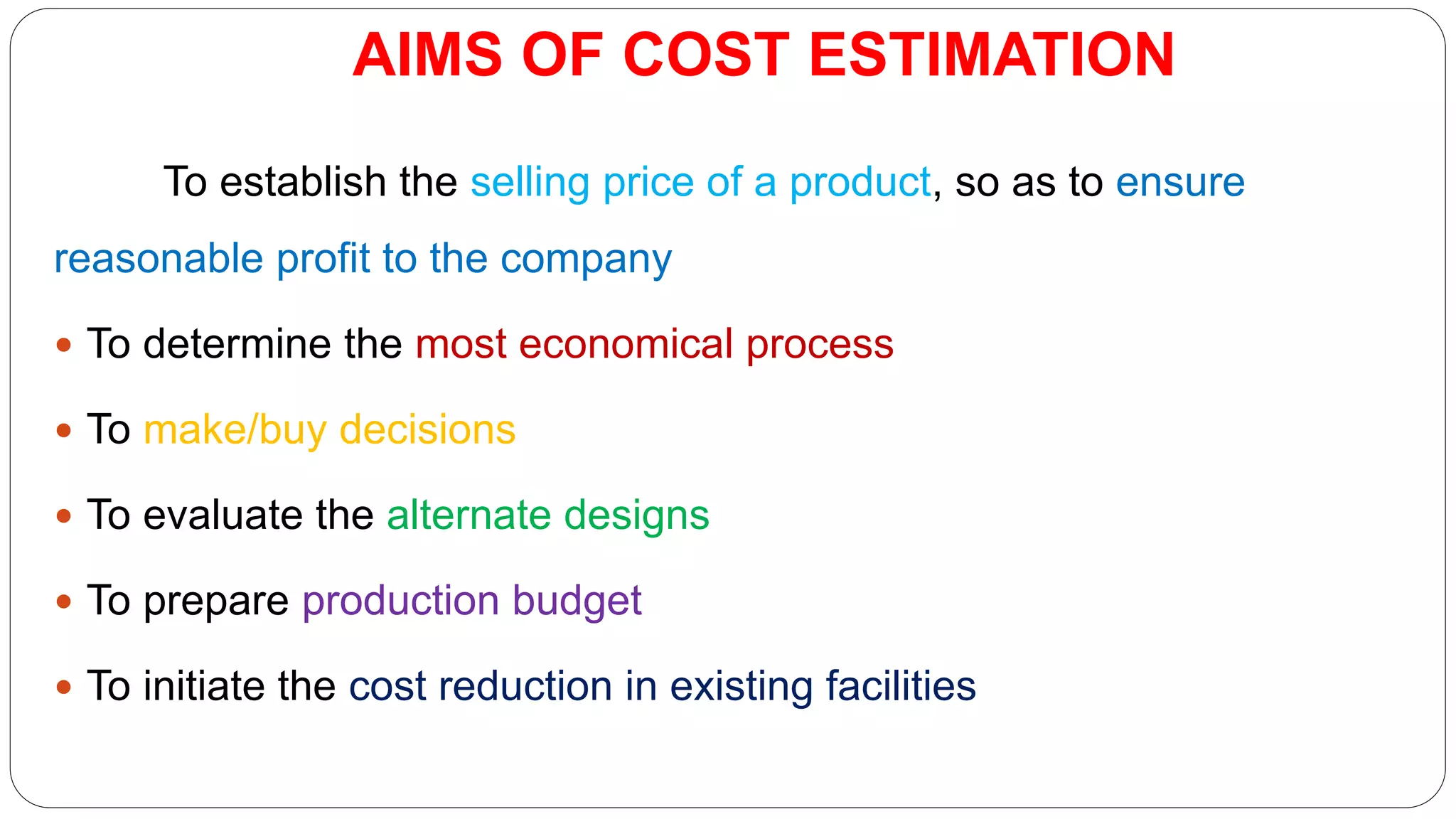

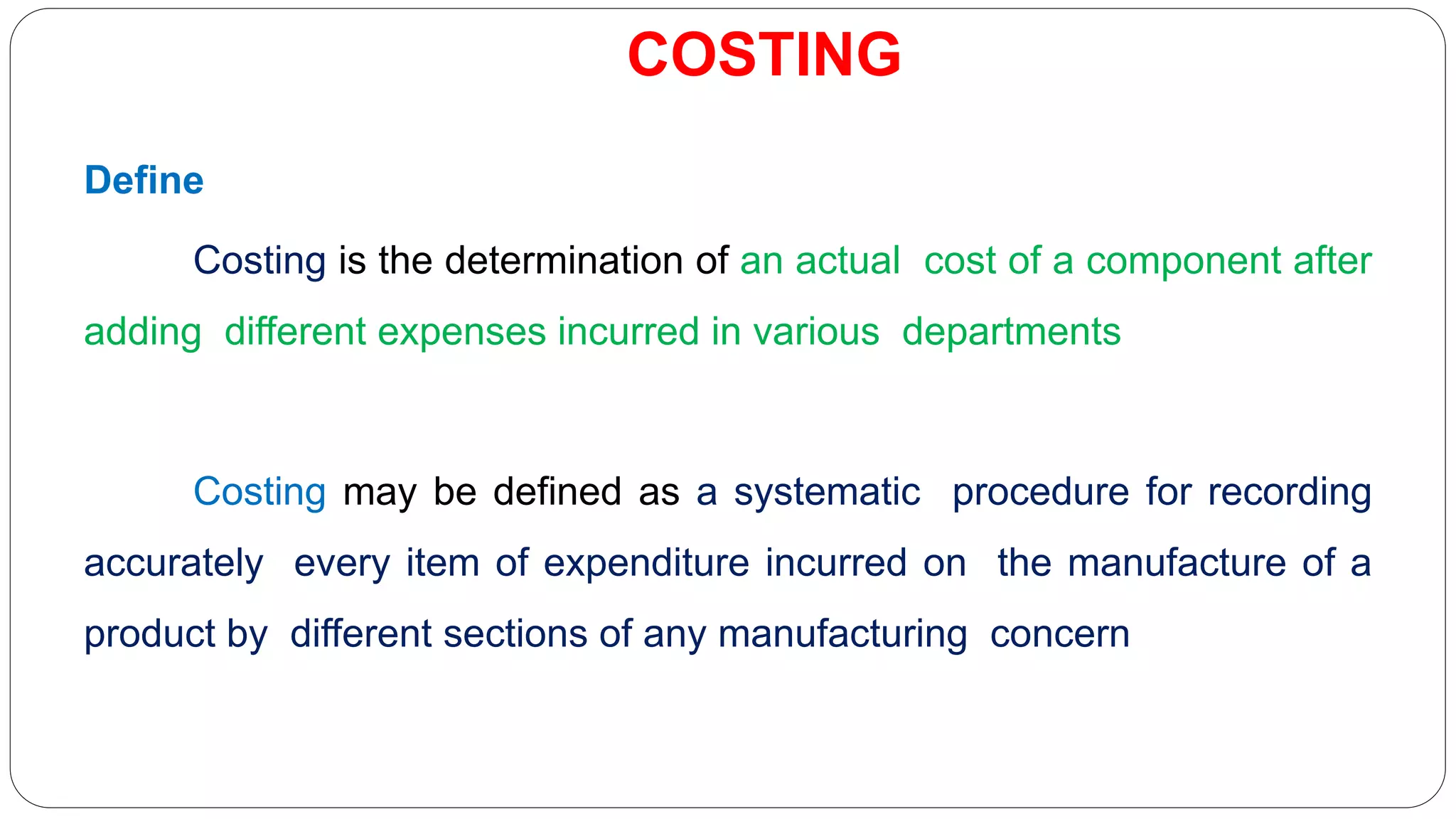

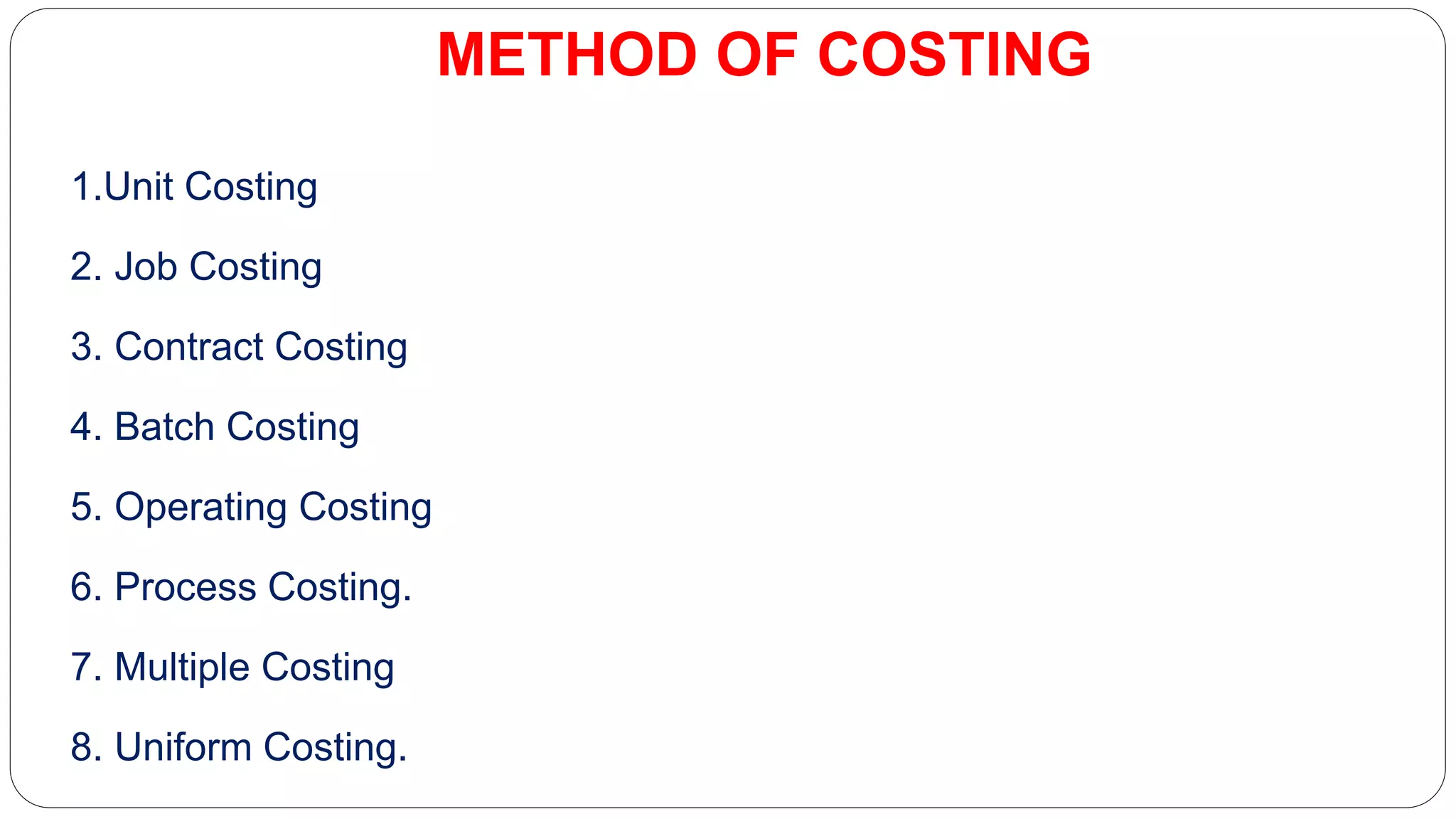

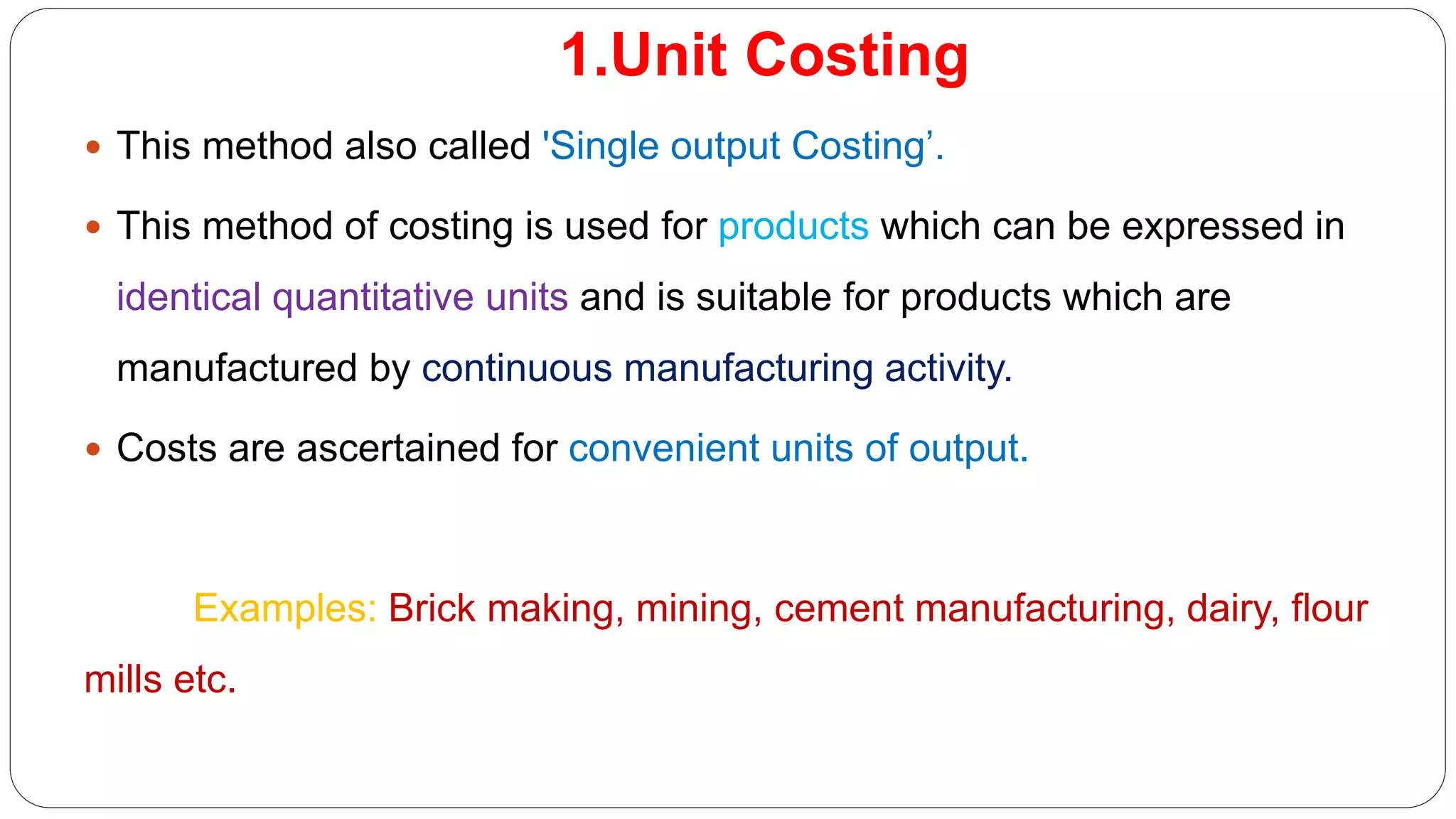

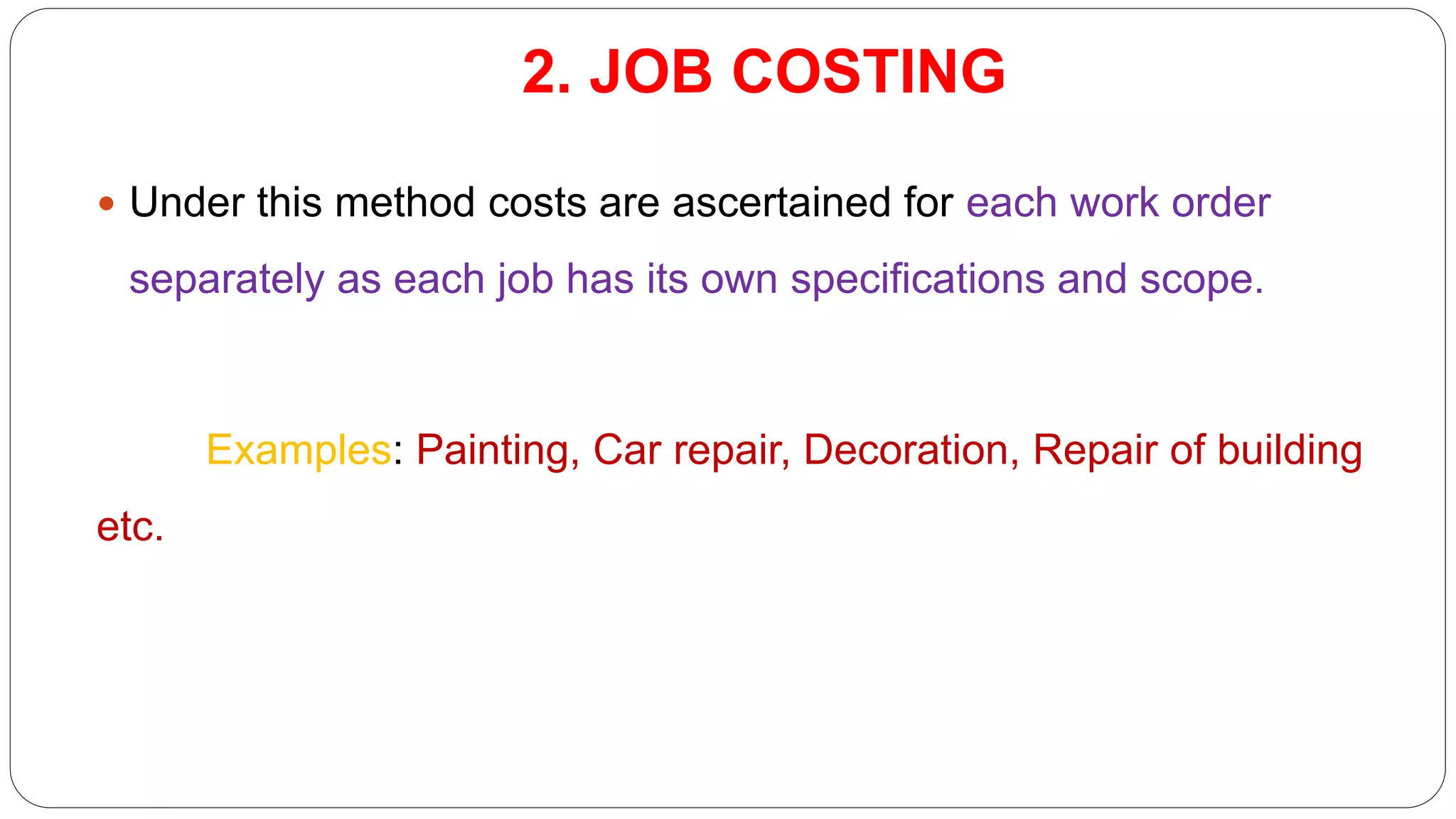

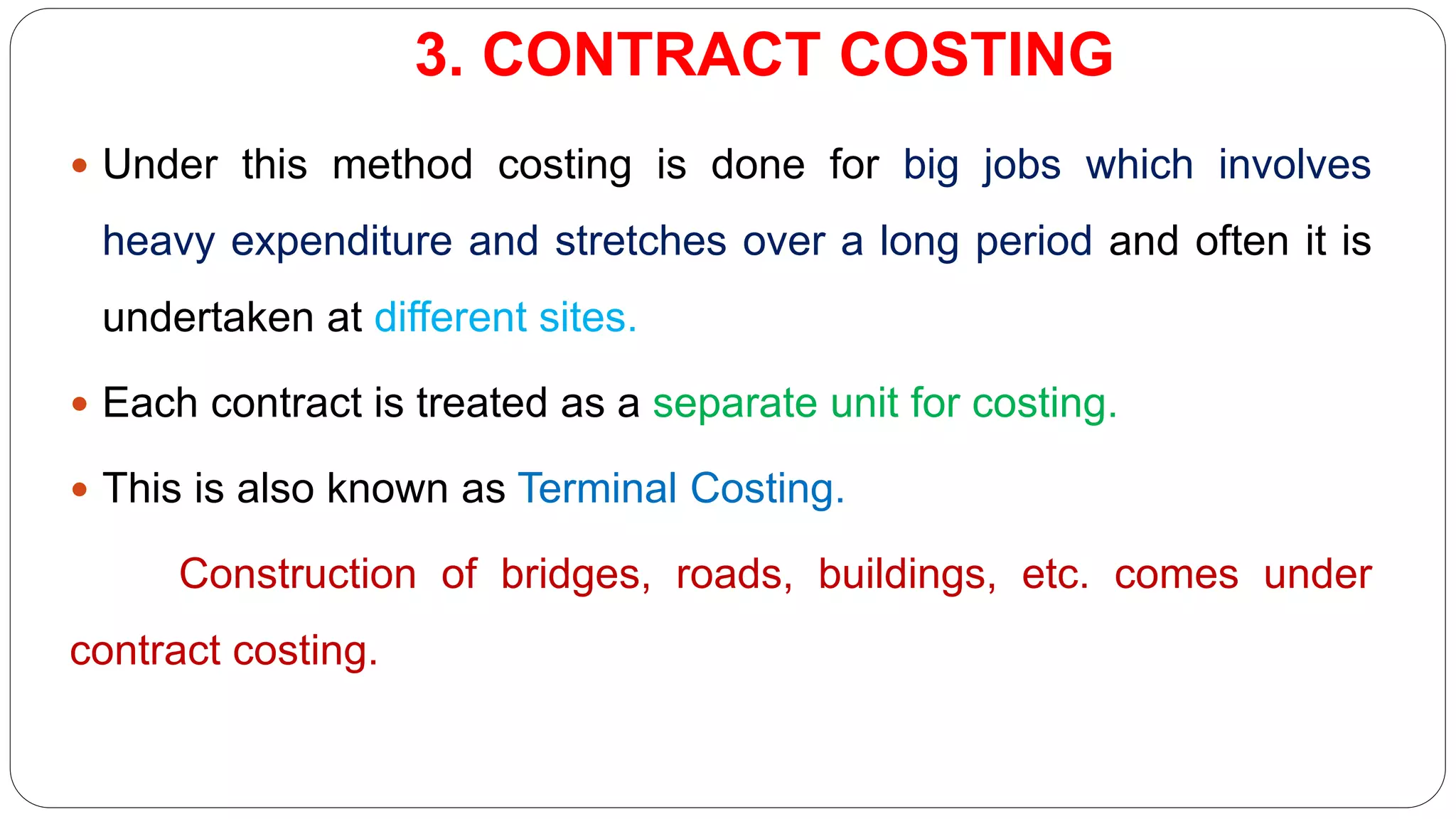

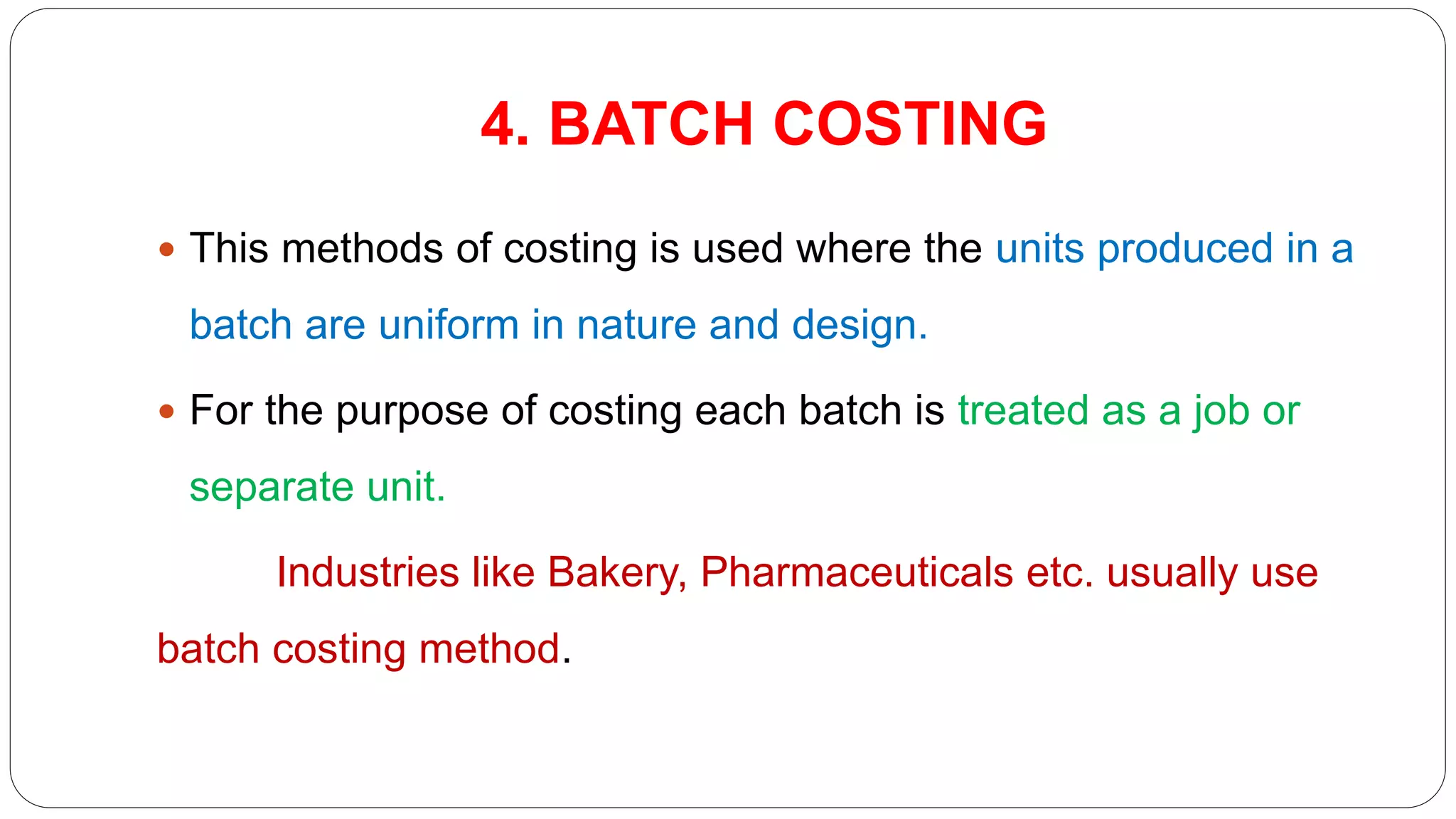

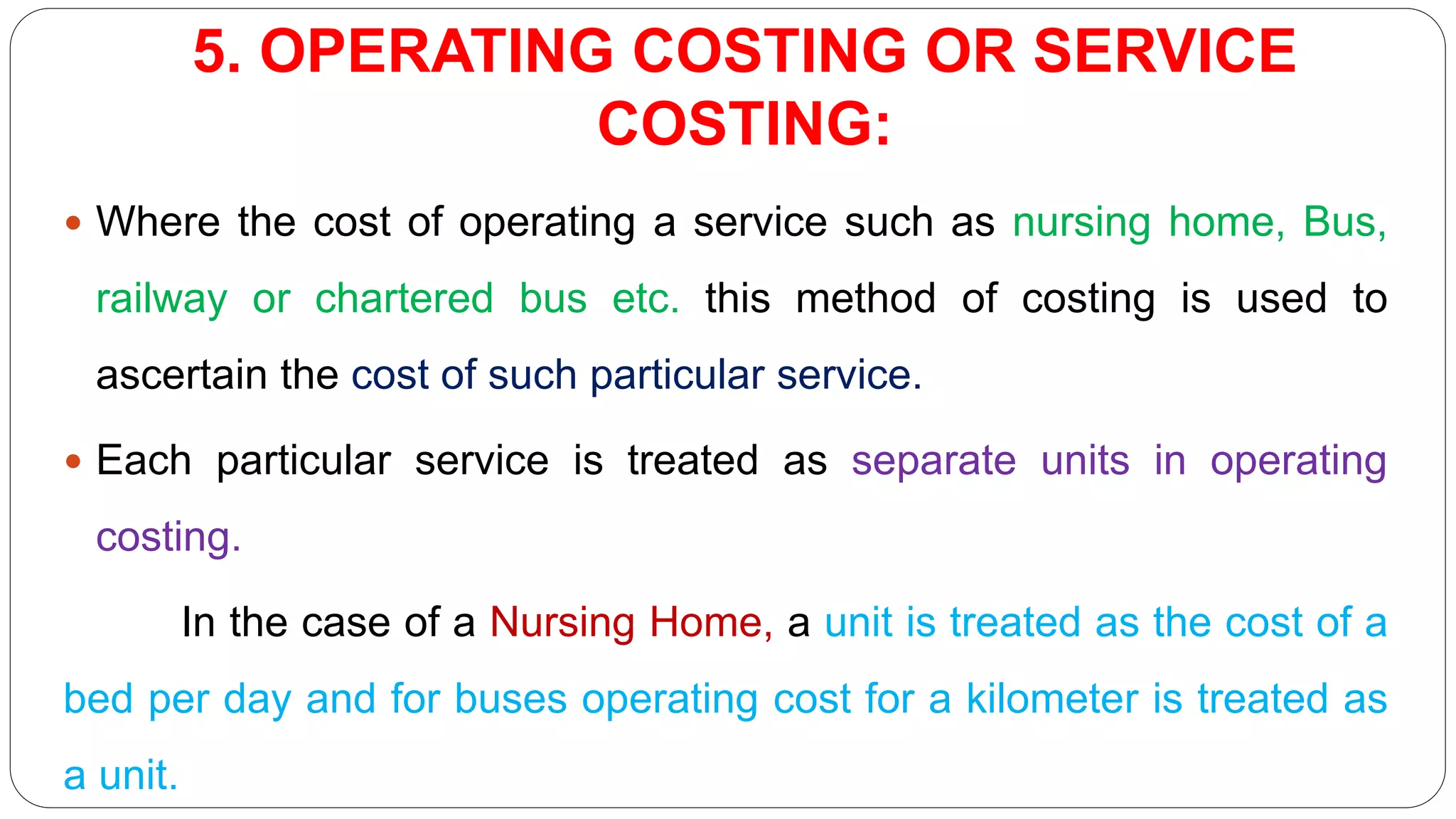

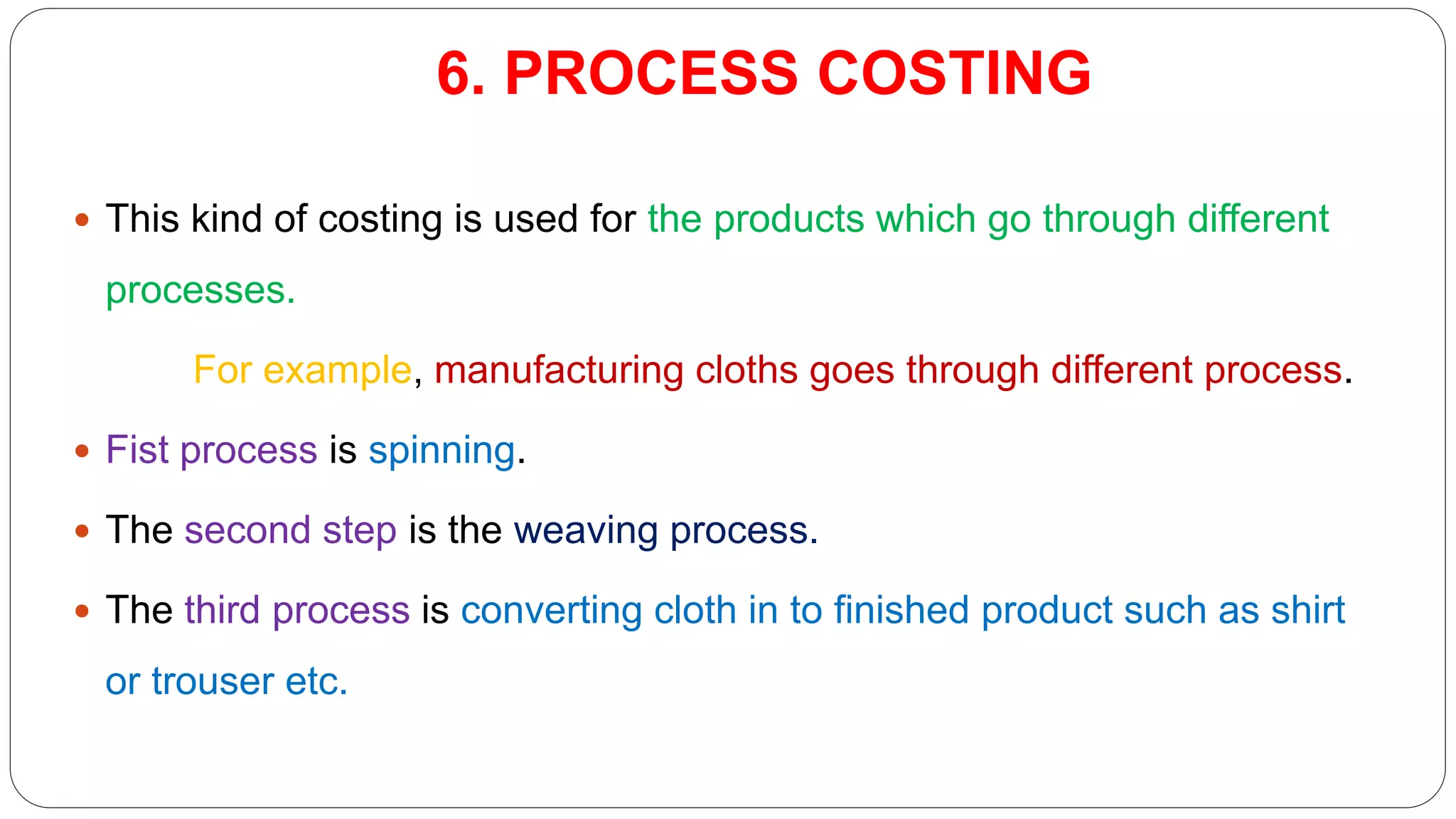

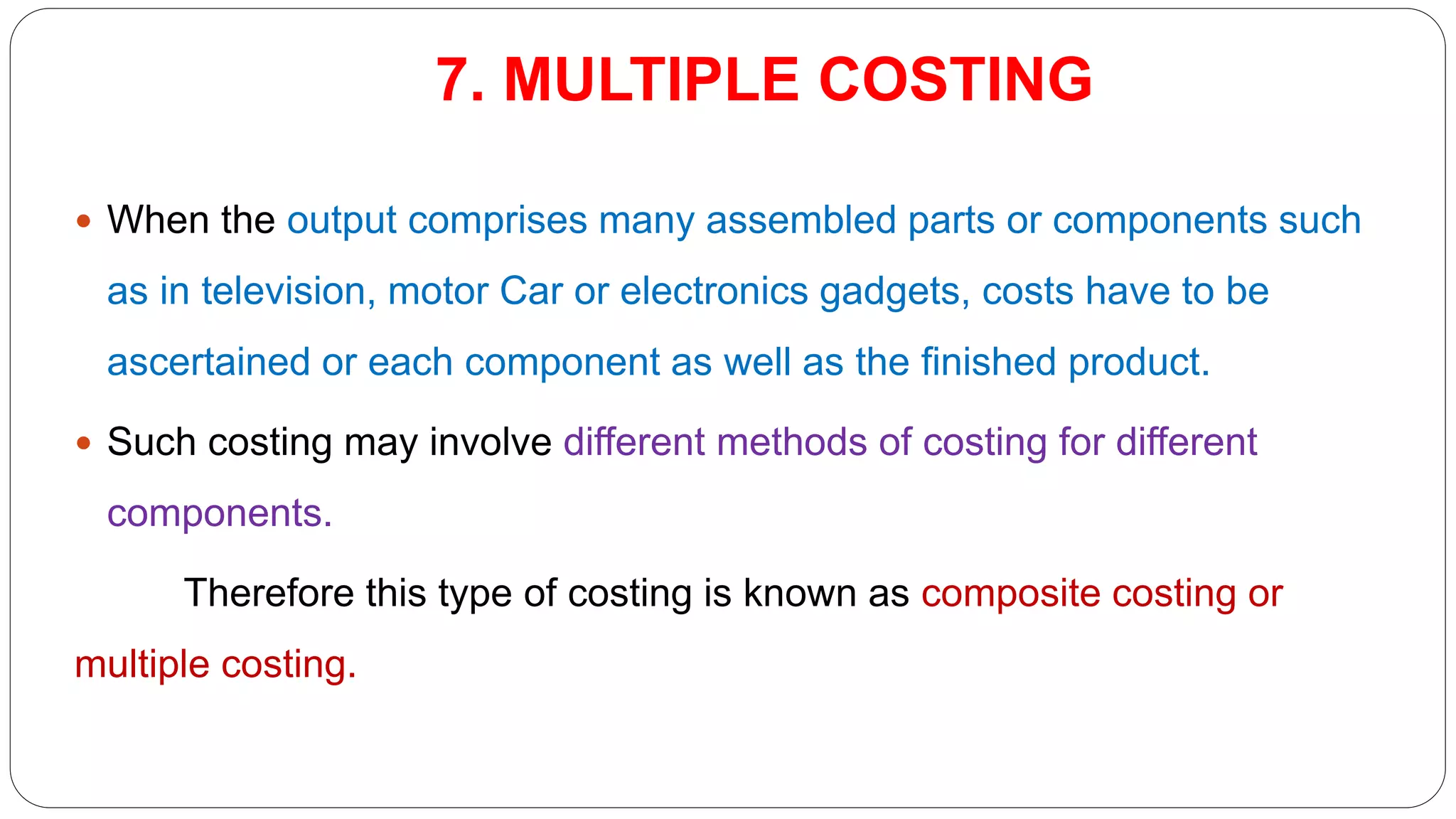

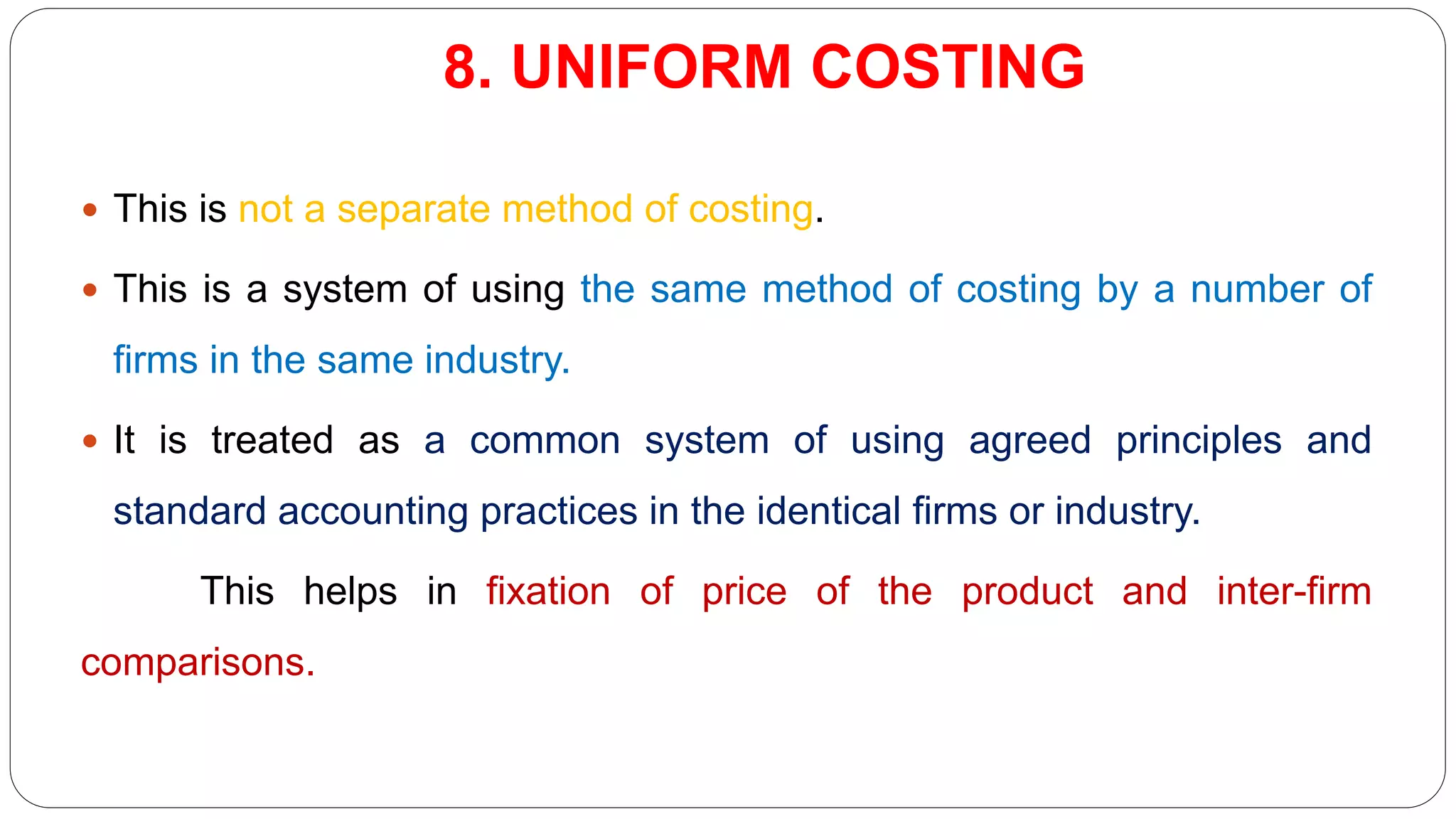

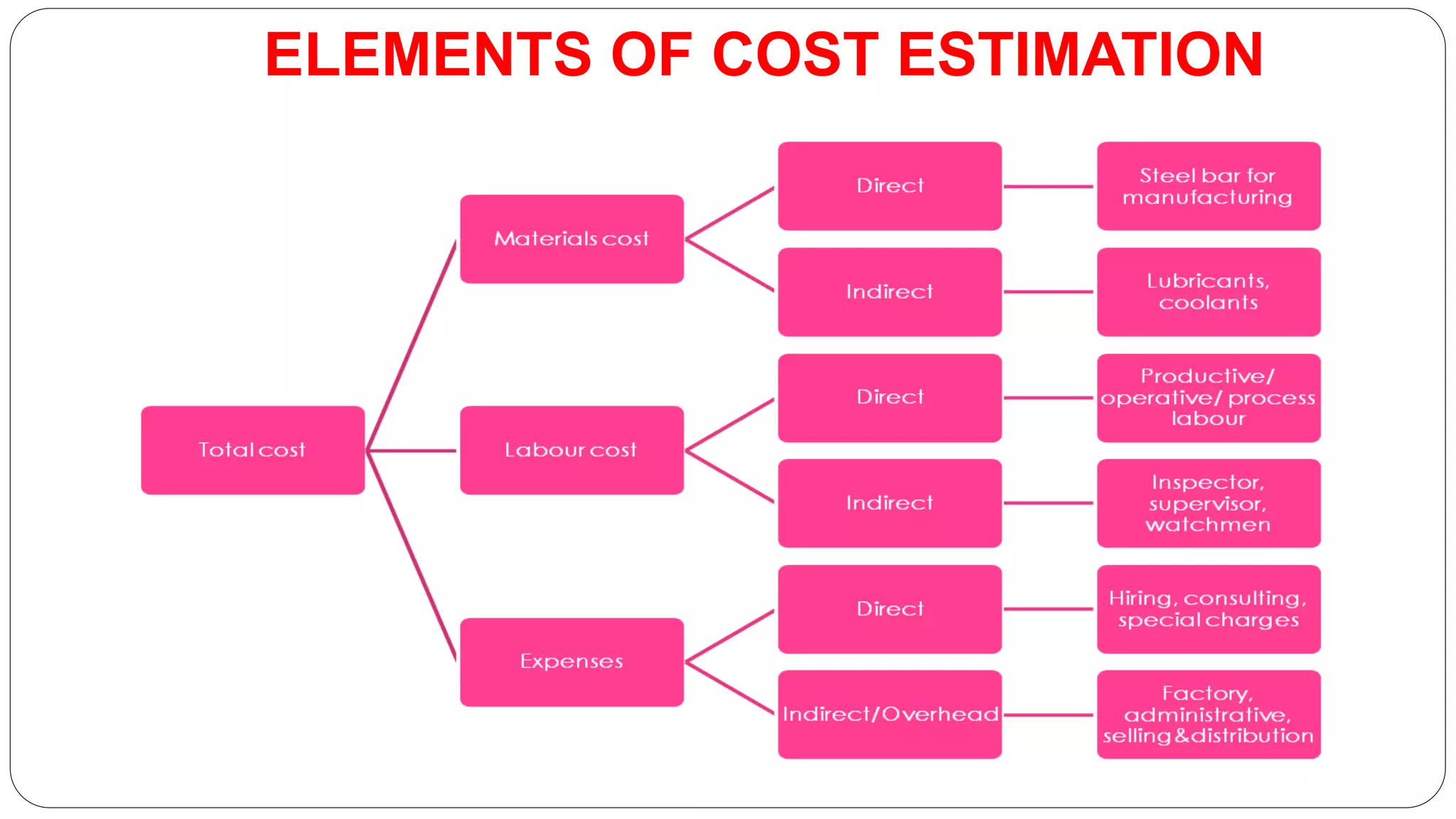

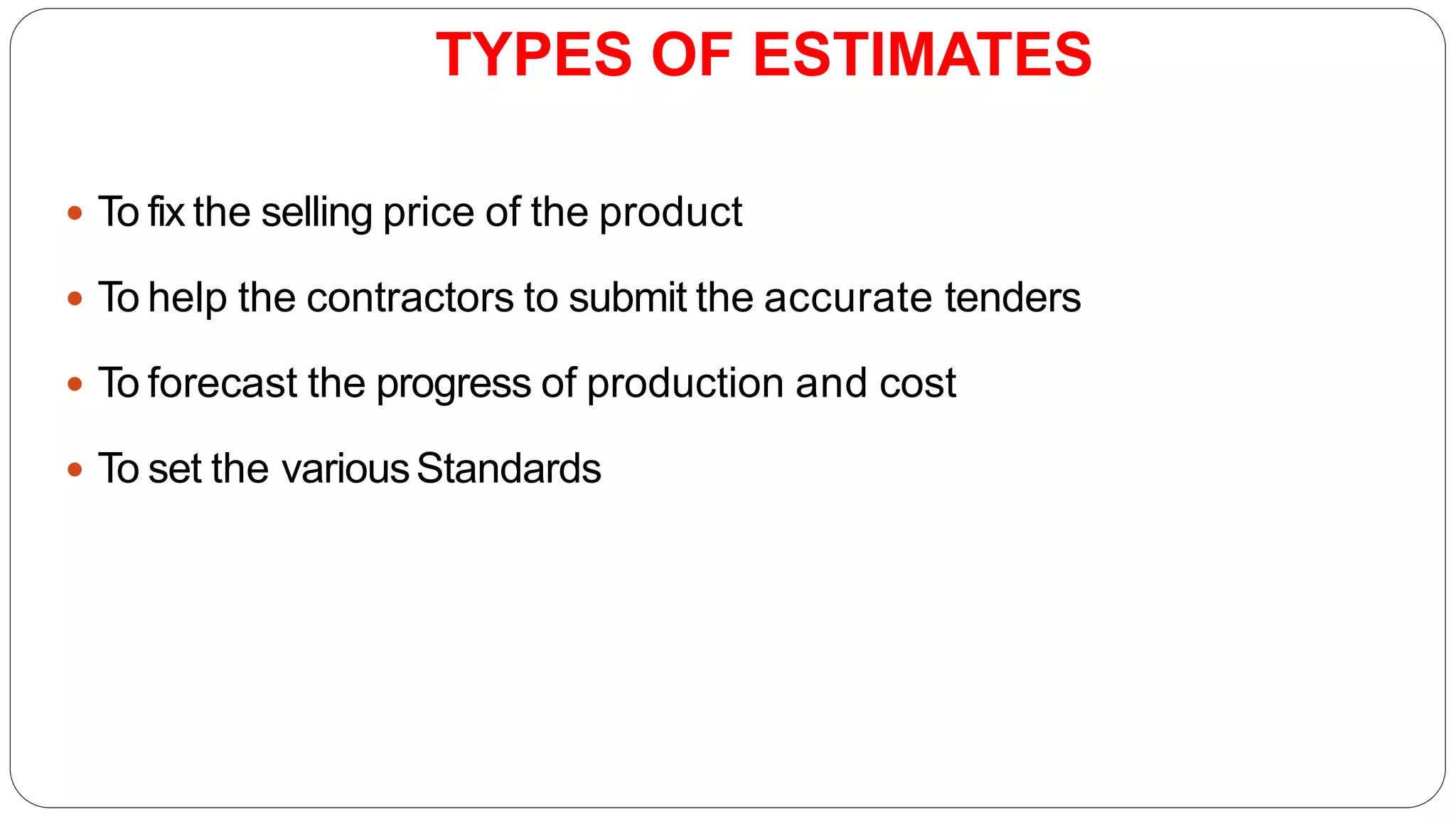

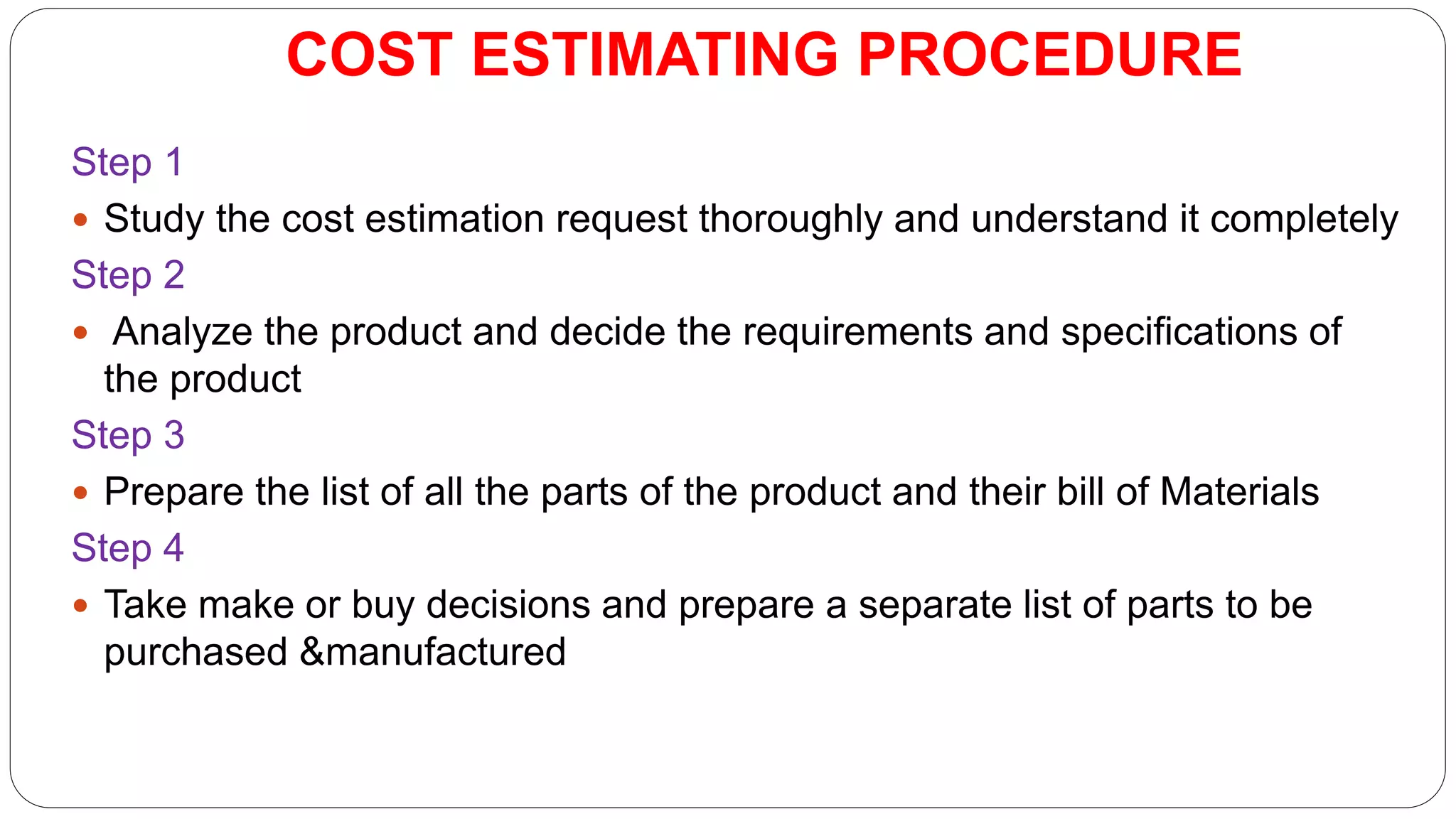

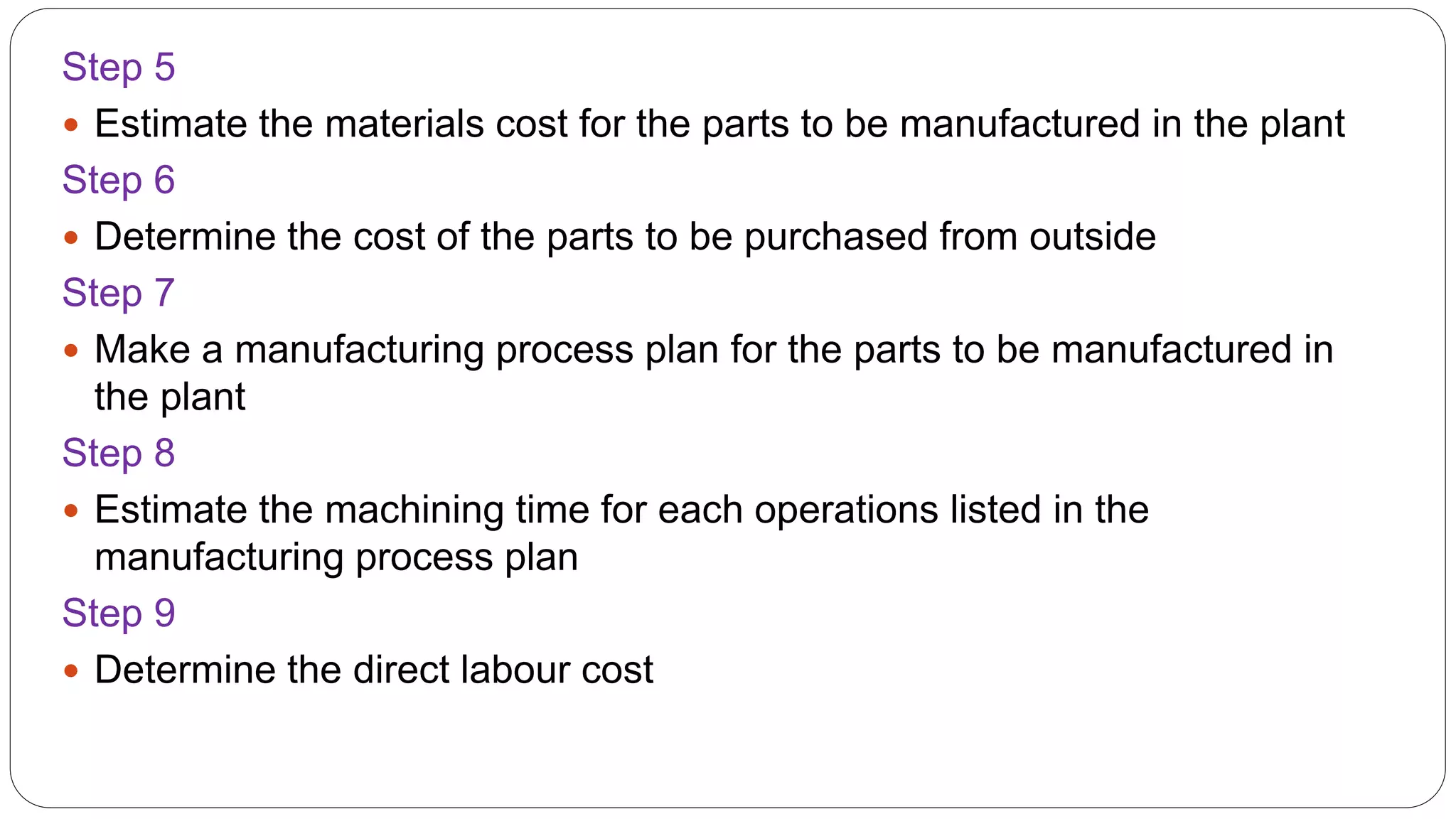

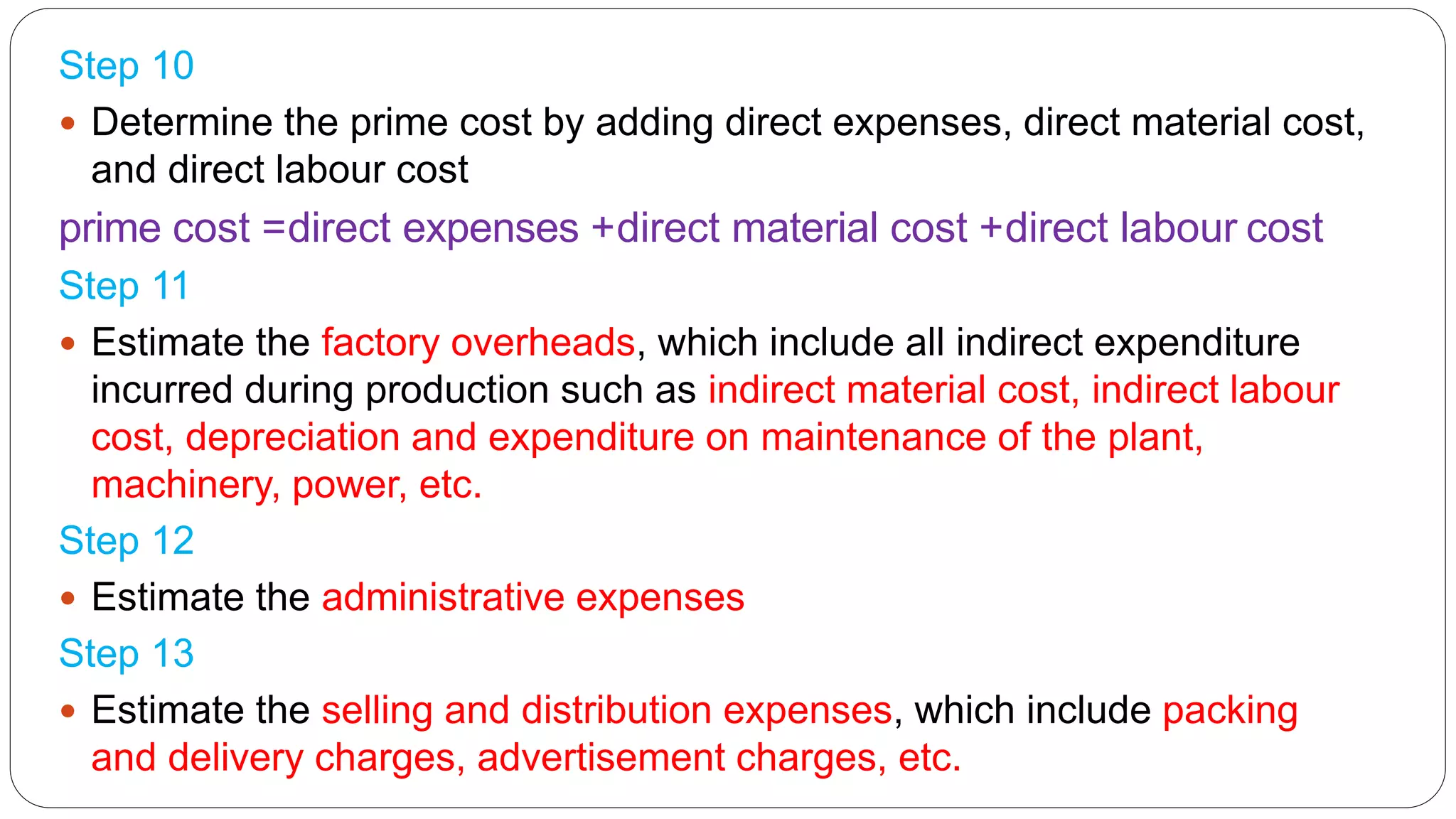

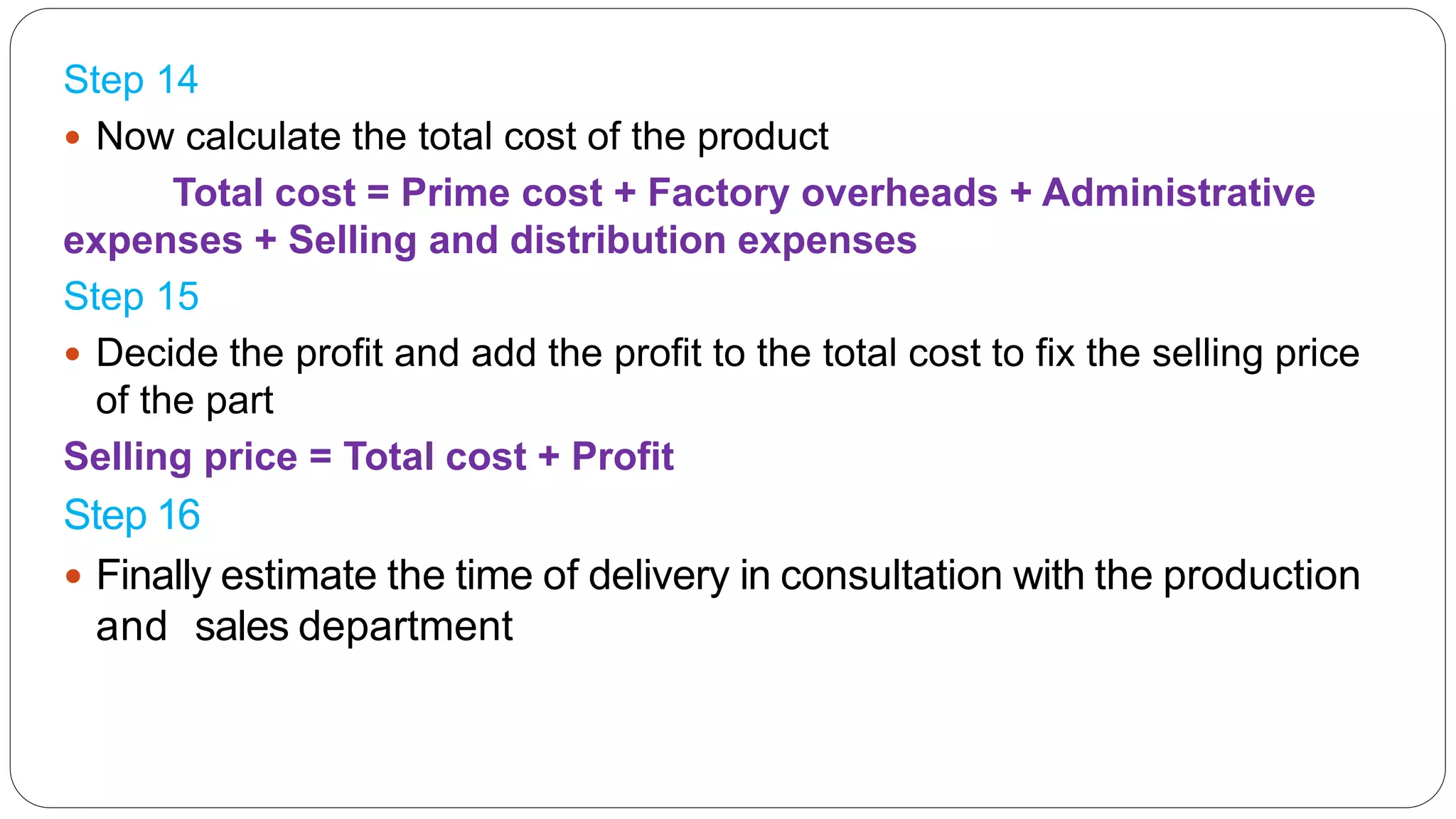

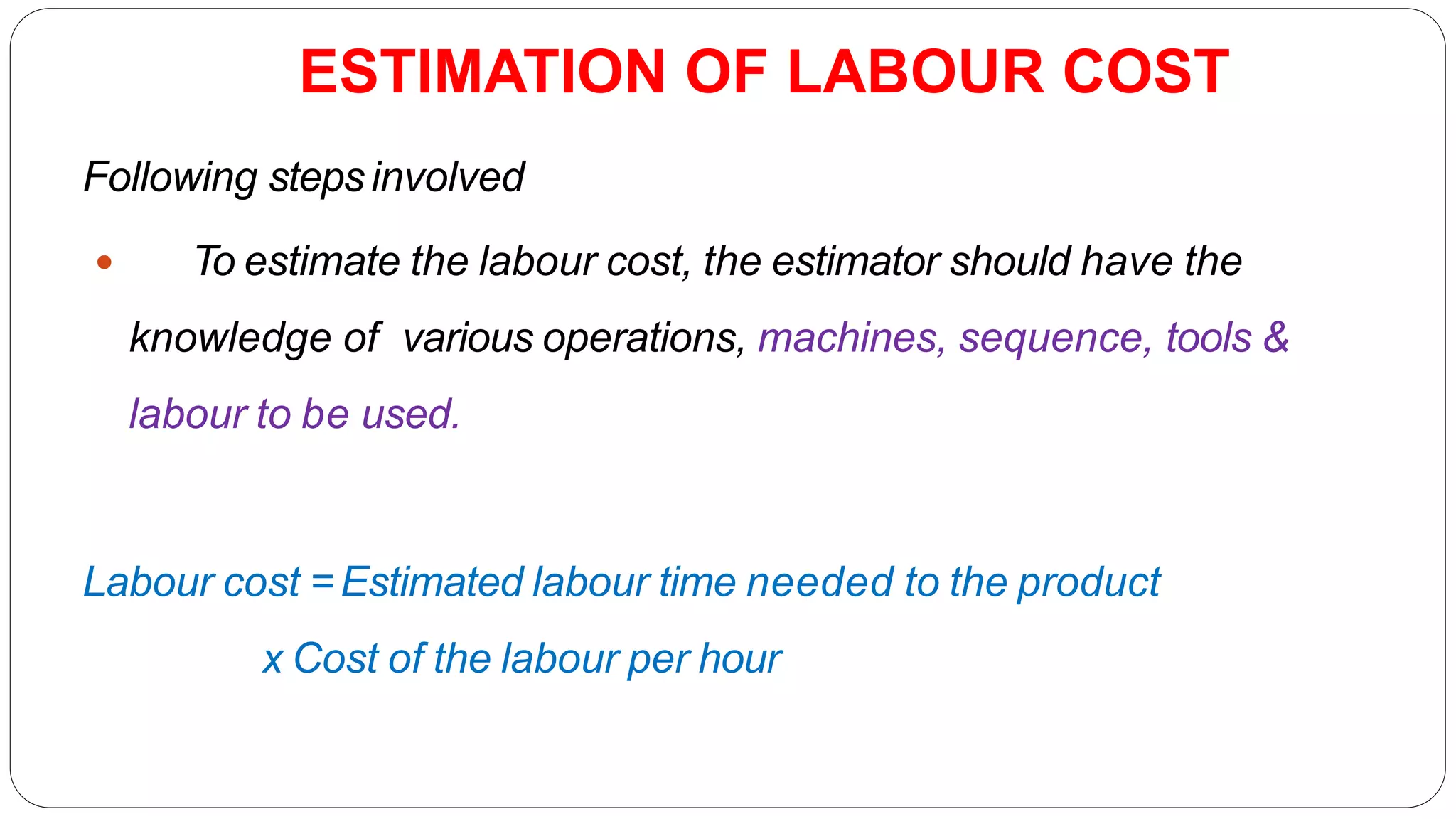

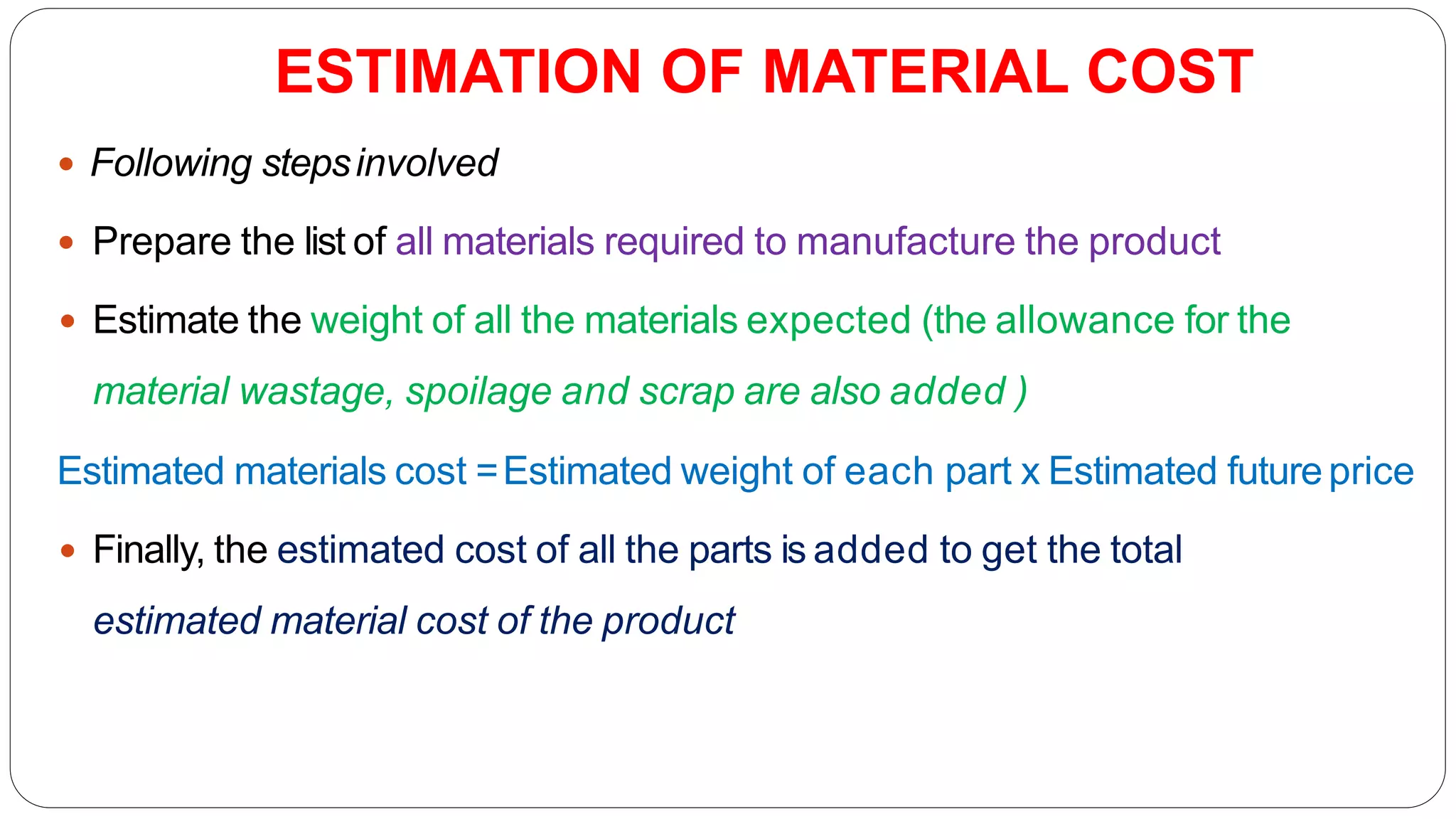

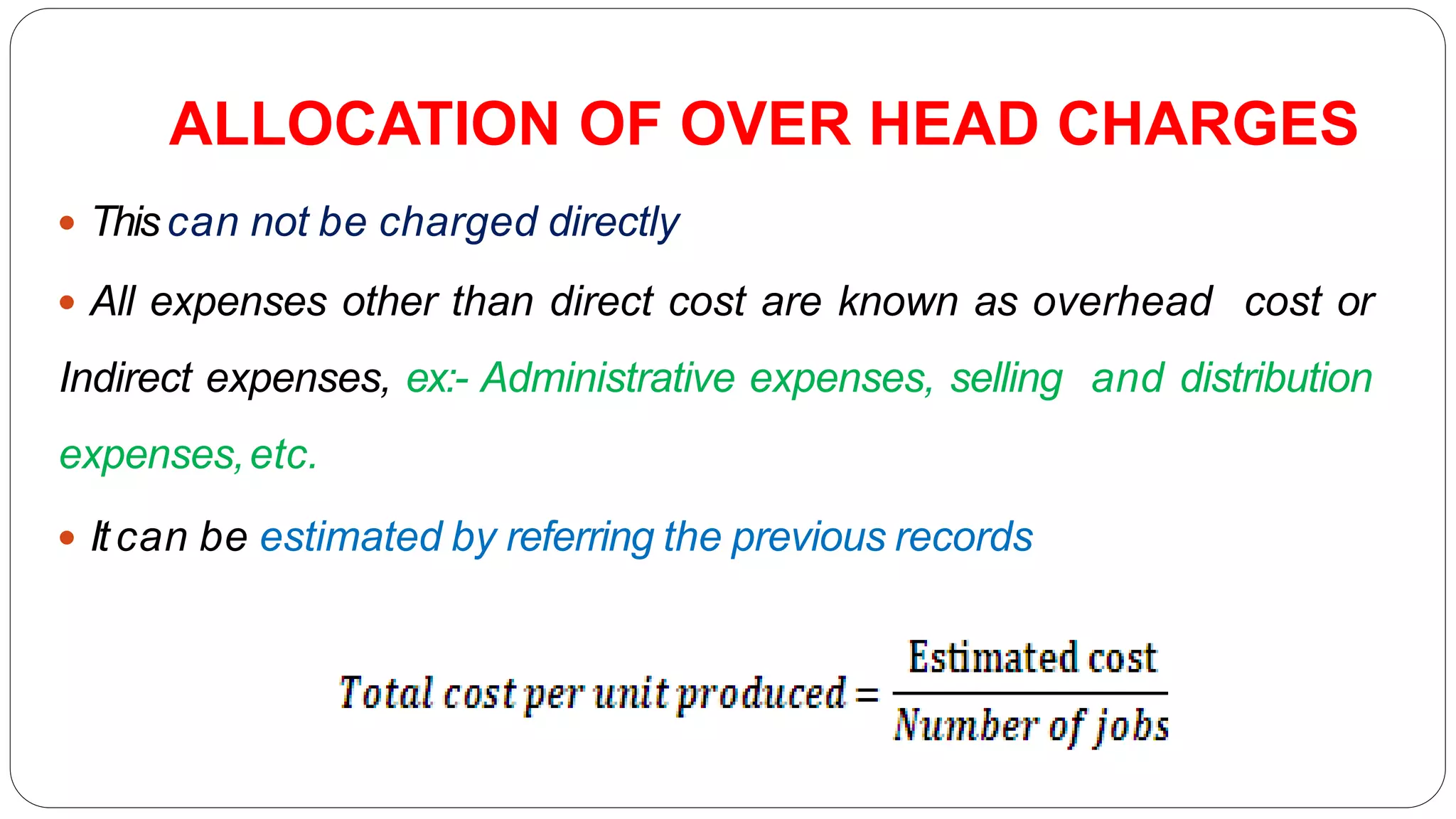

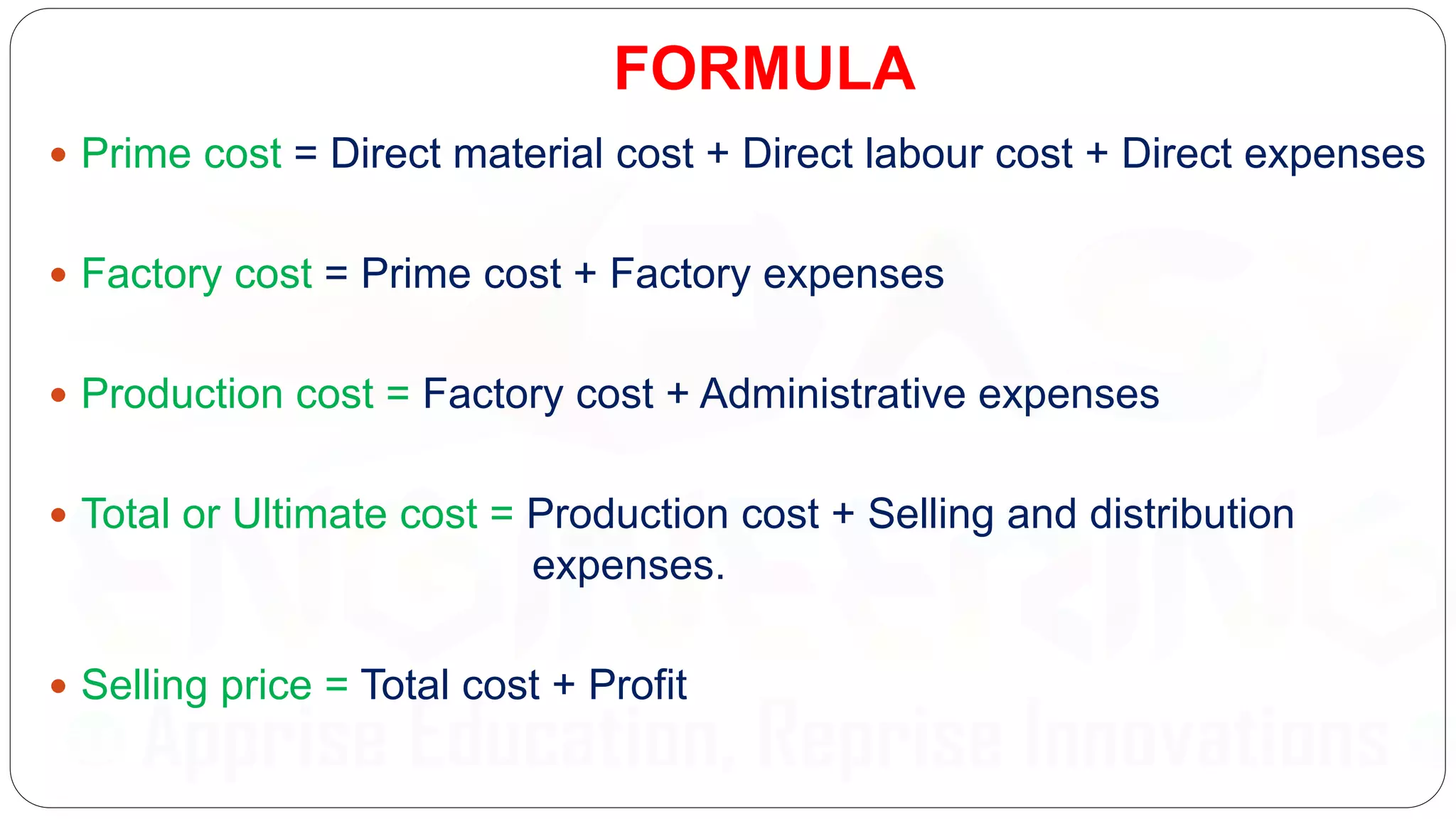

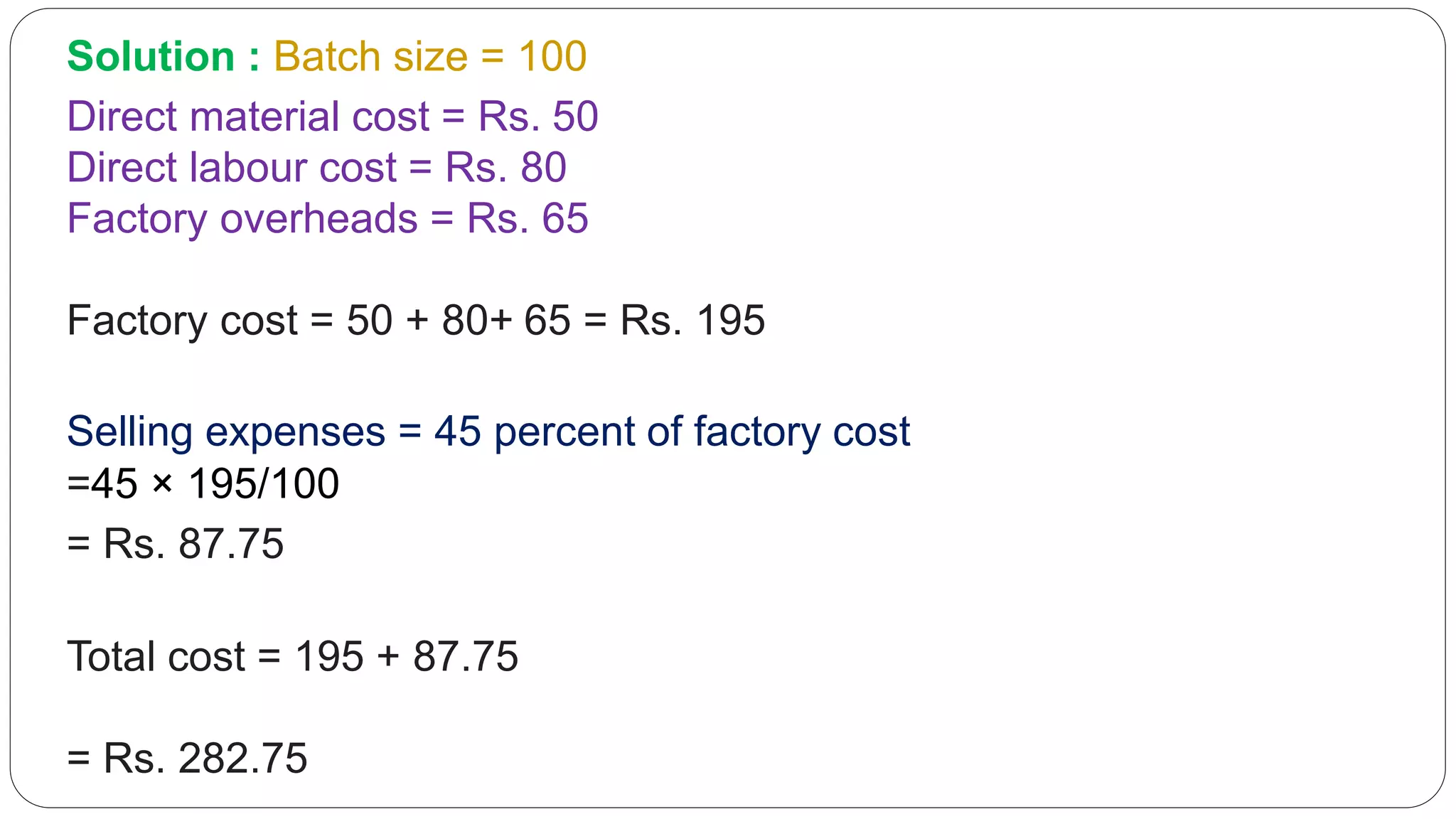

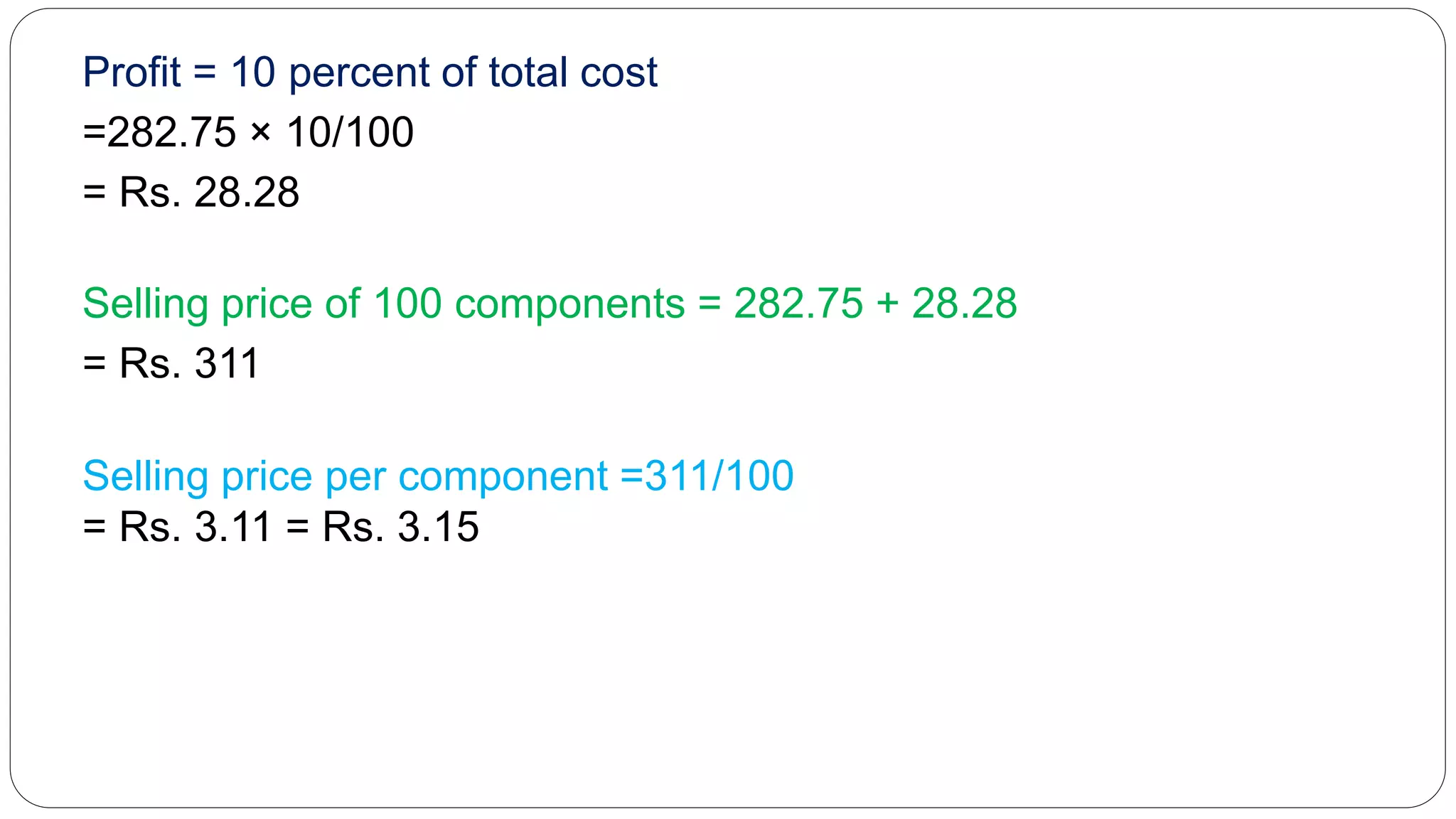

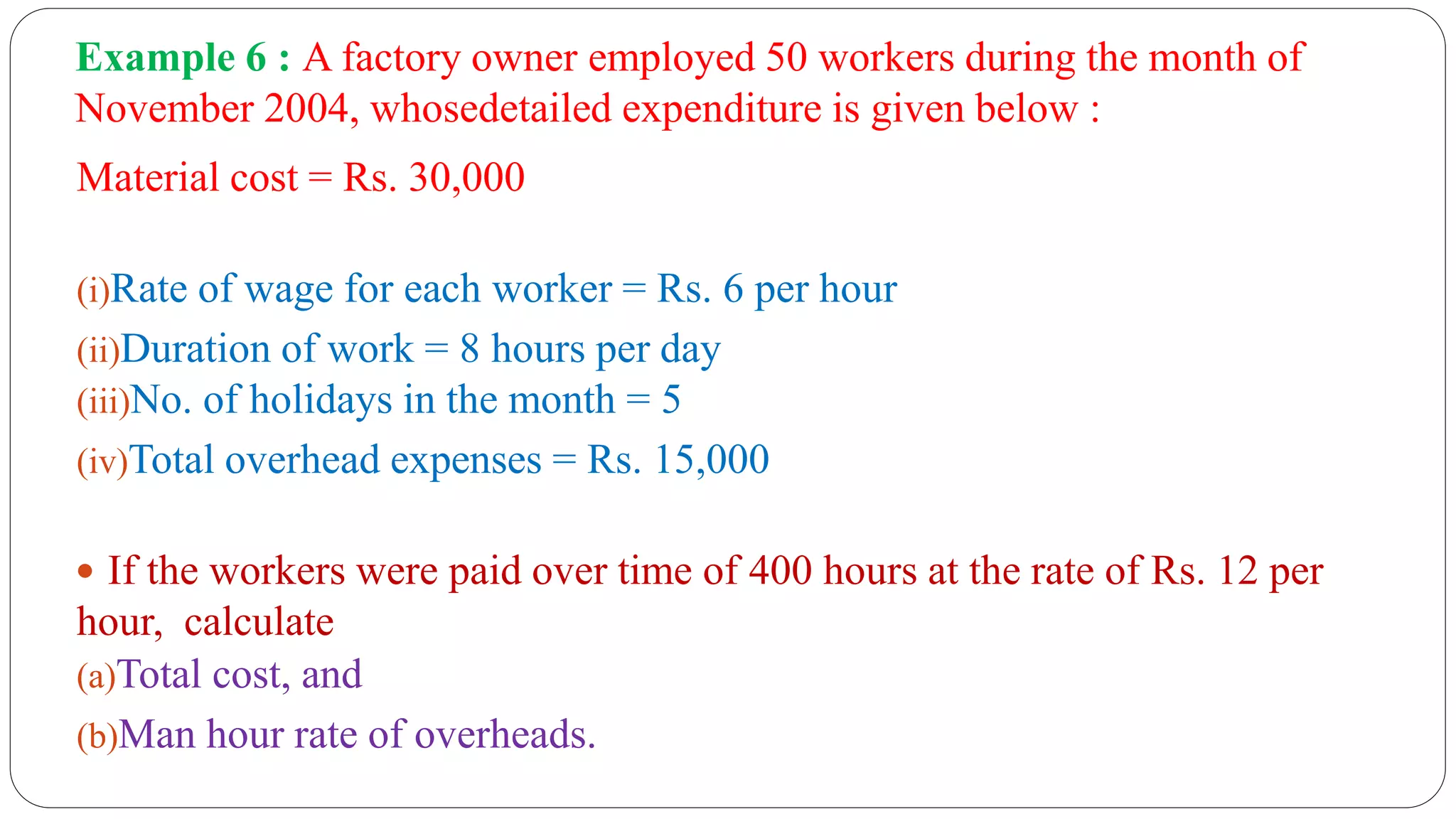

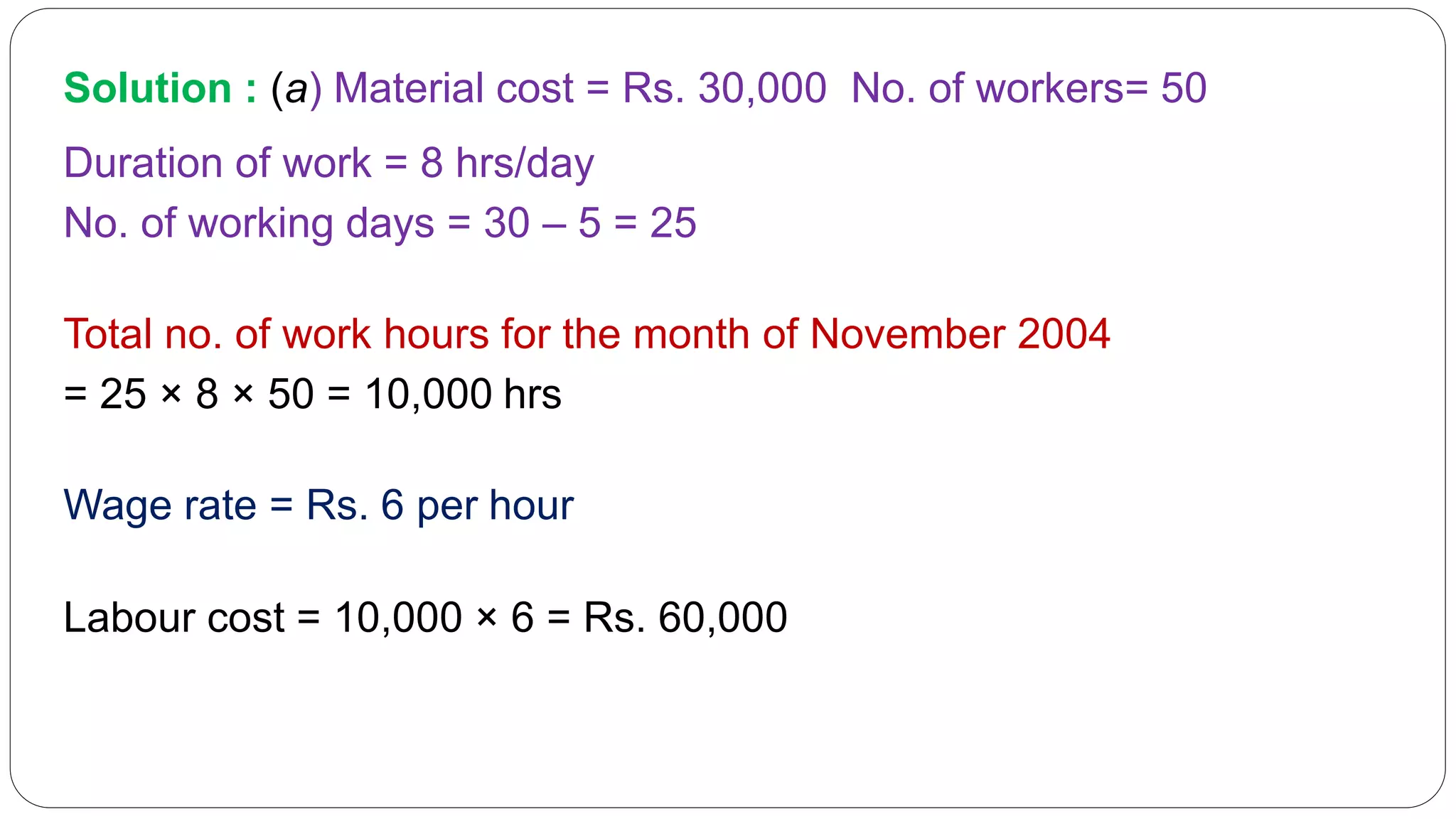

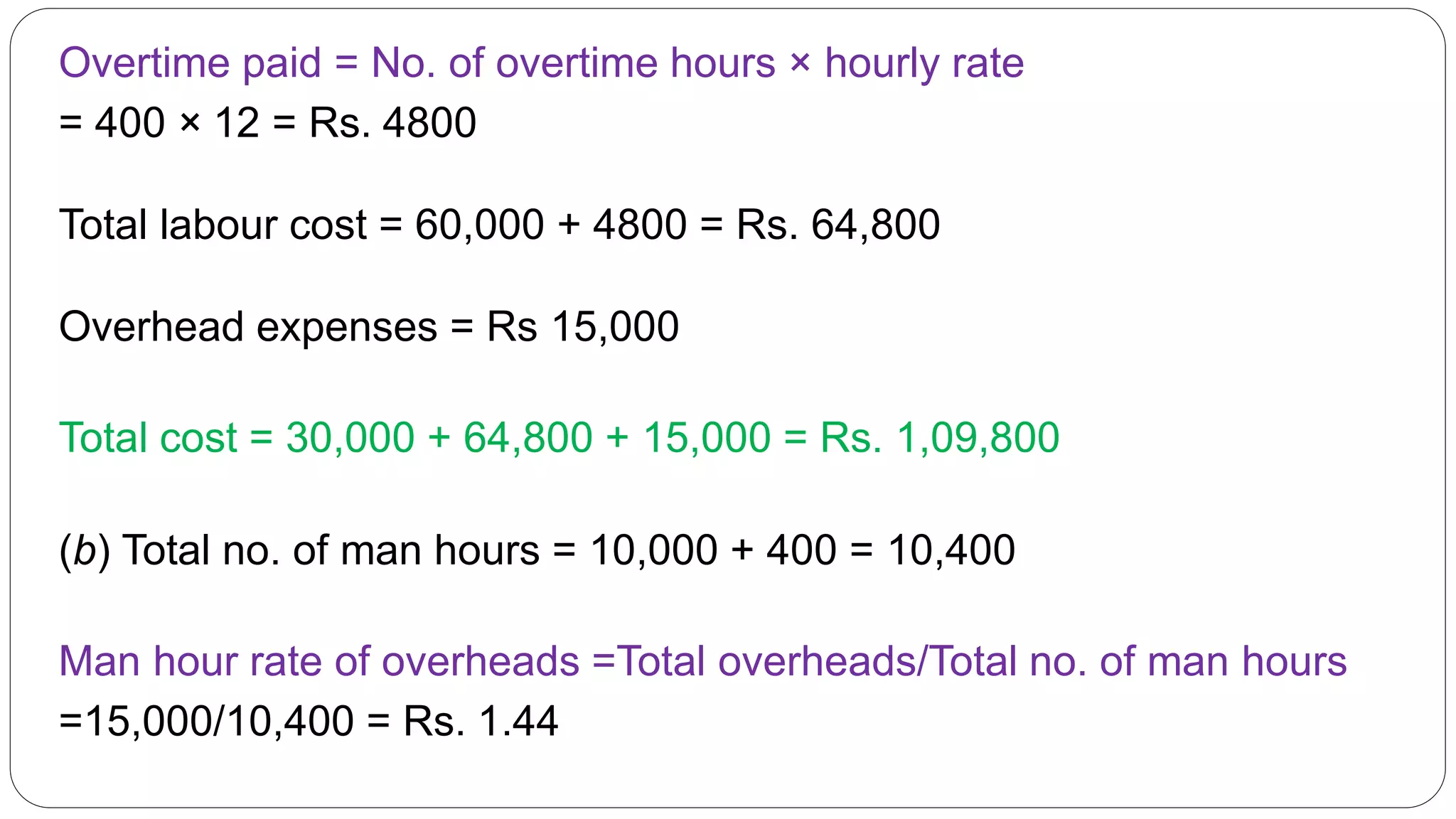

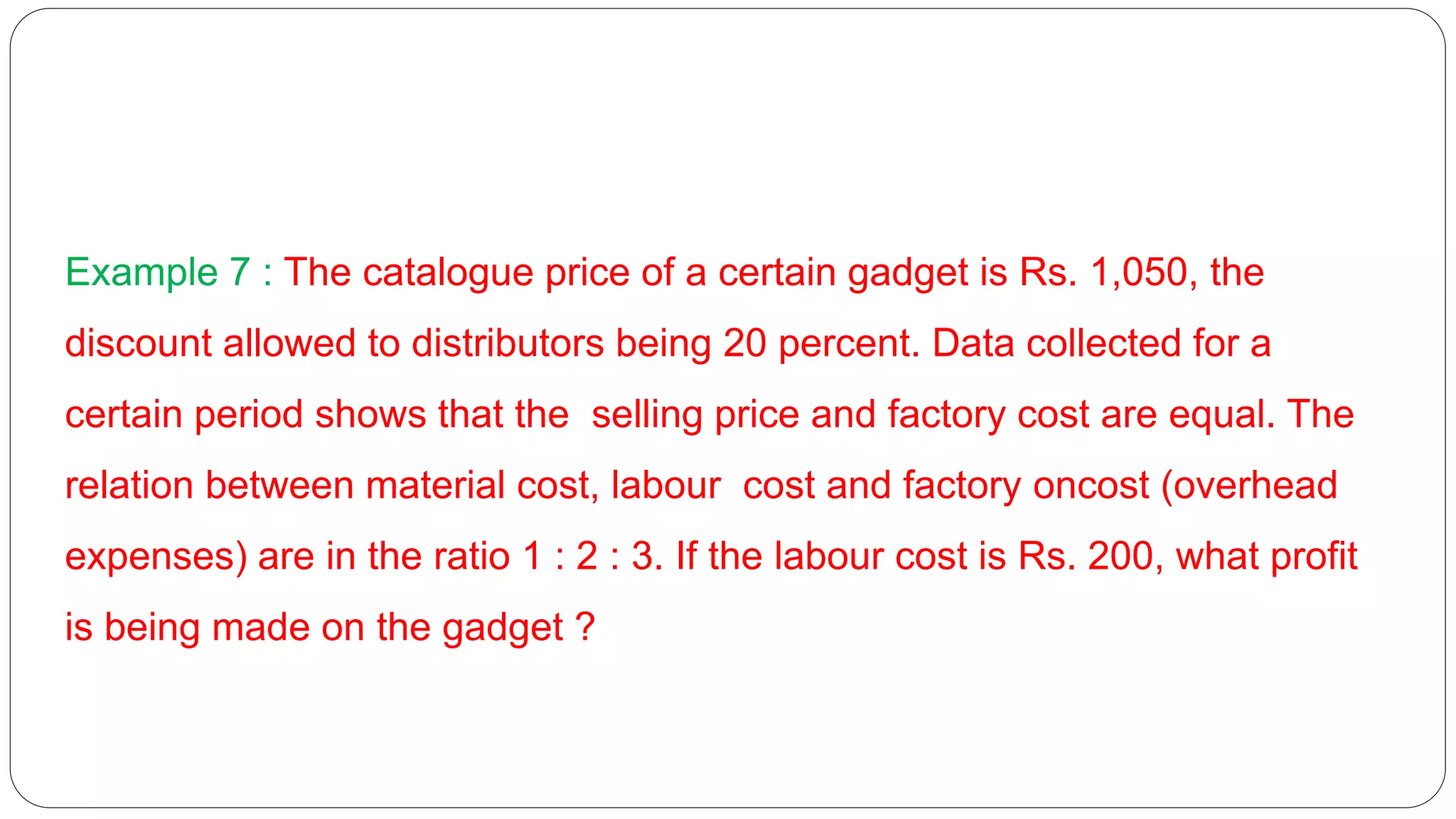

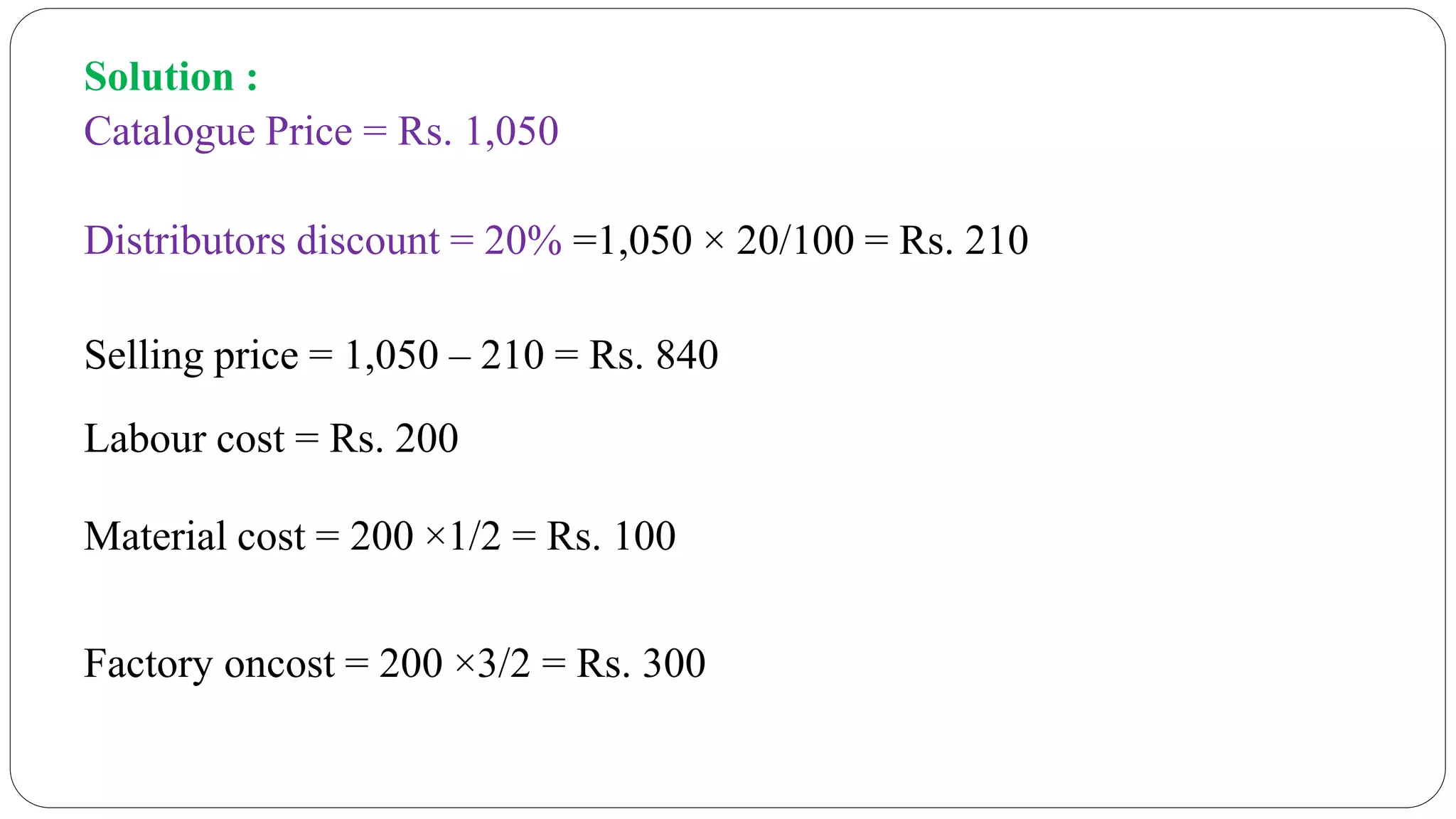

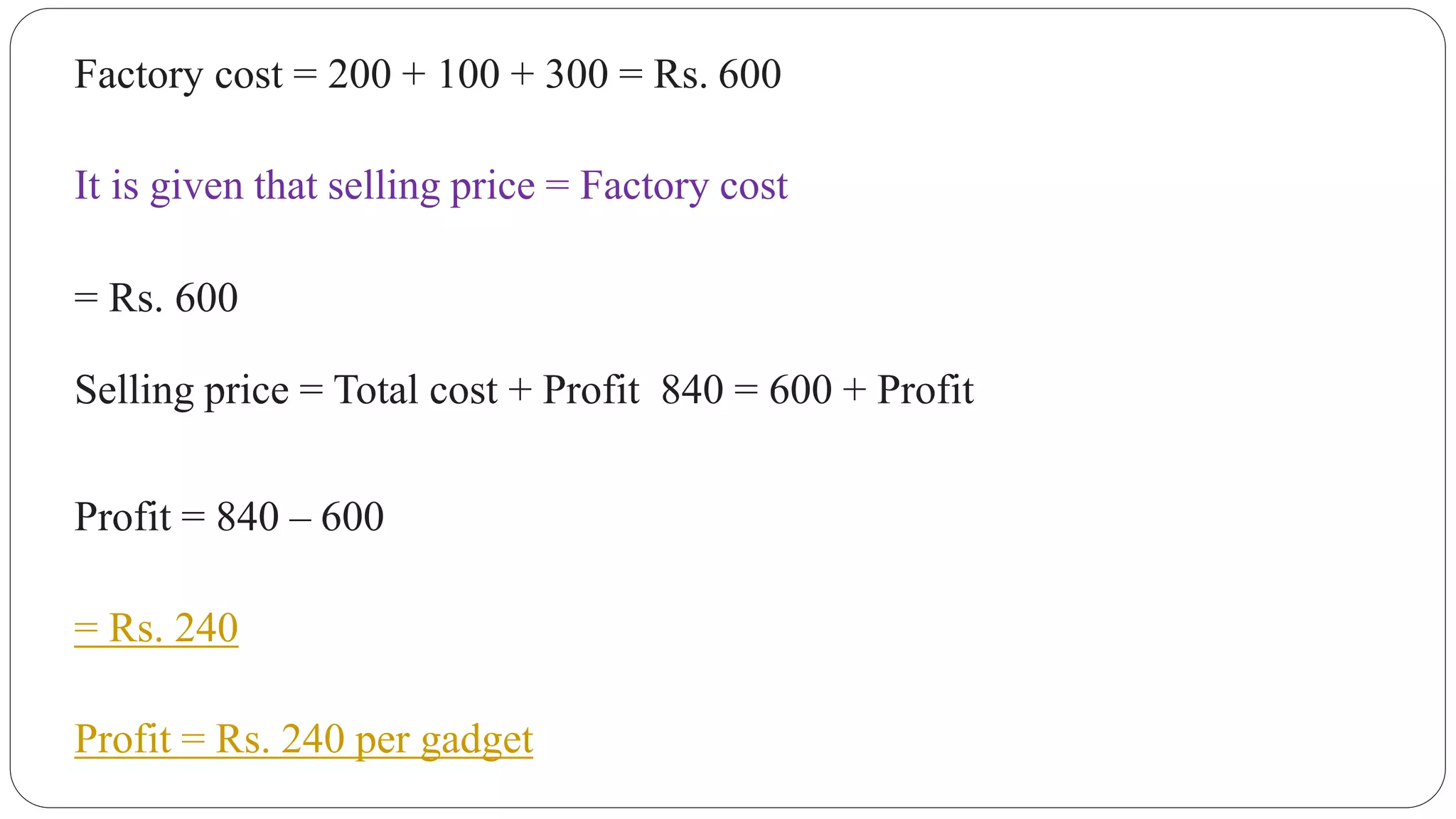

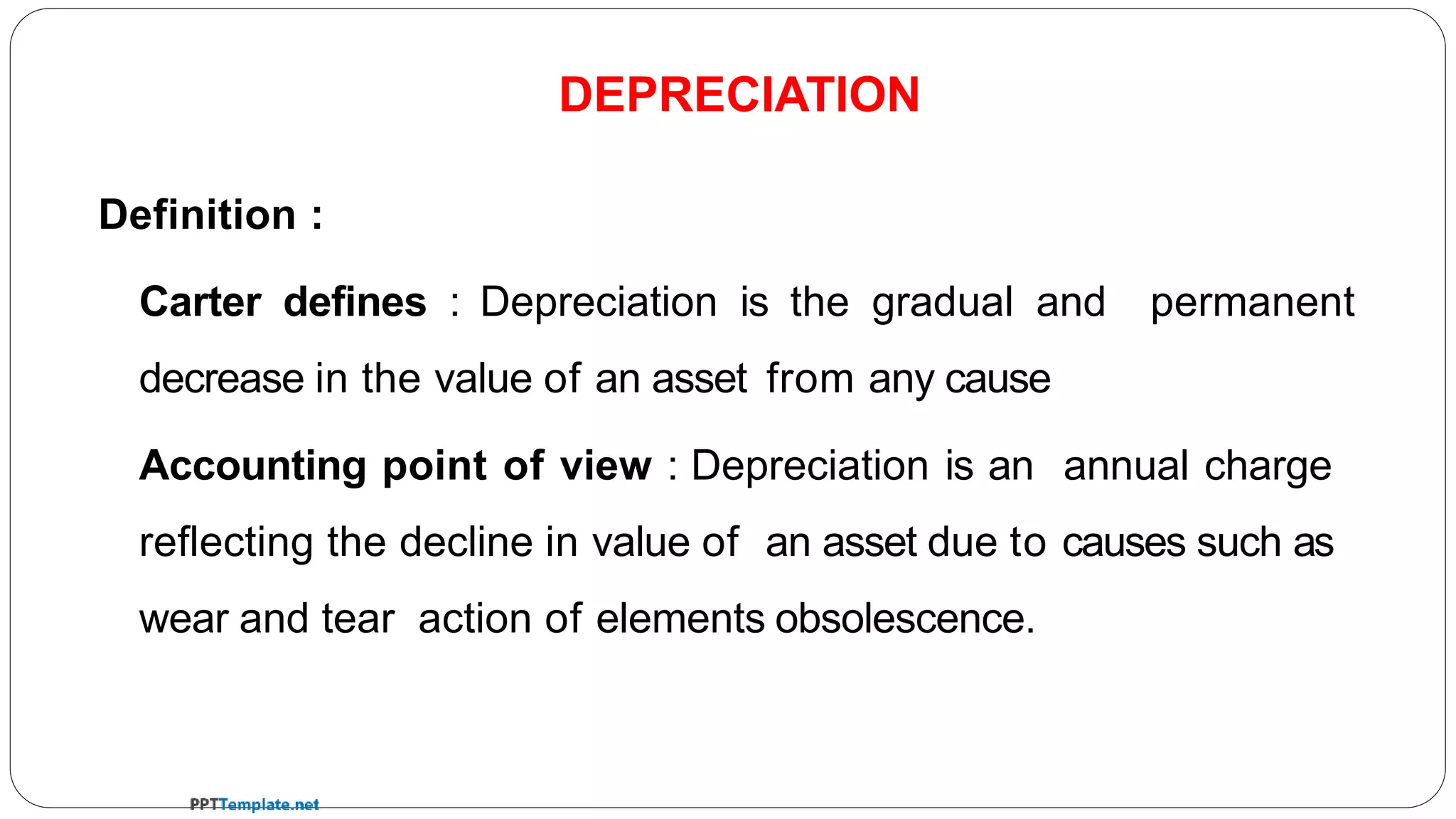

This document is an introduction to cost estimation in manufacturing, detailing its significance, methods, and procedures. It covers various costing methods, including unit, job, and process costing, and provides a structured process for estimating costs associated with labor, materials, and overhead. Additionally, the document outlines crucial elements of cost estimation, different types of estimates, and practical examples for calculating costs and selling prices.

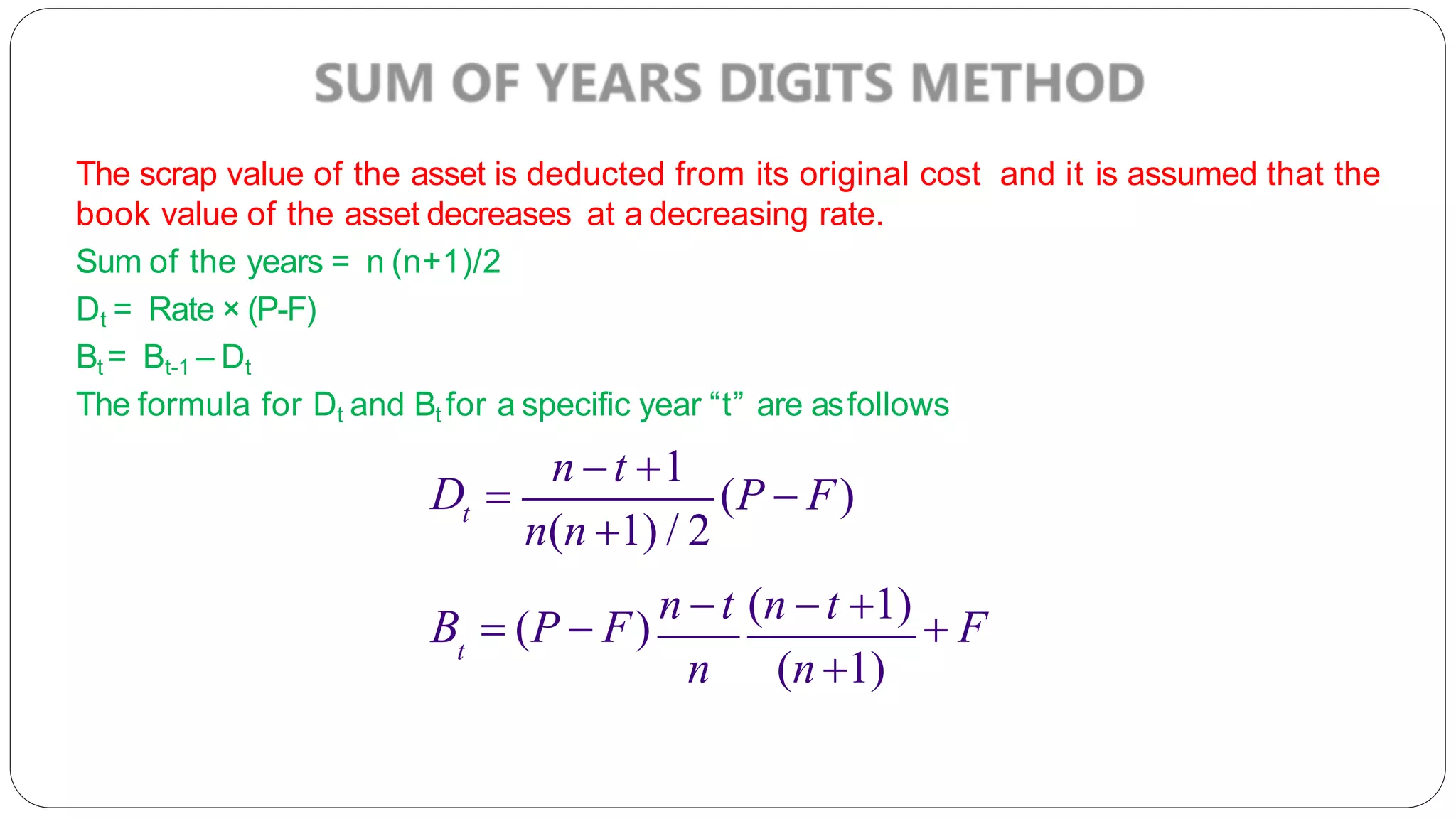

![t t

n

i1

B B D P t[P F ]

t

n

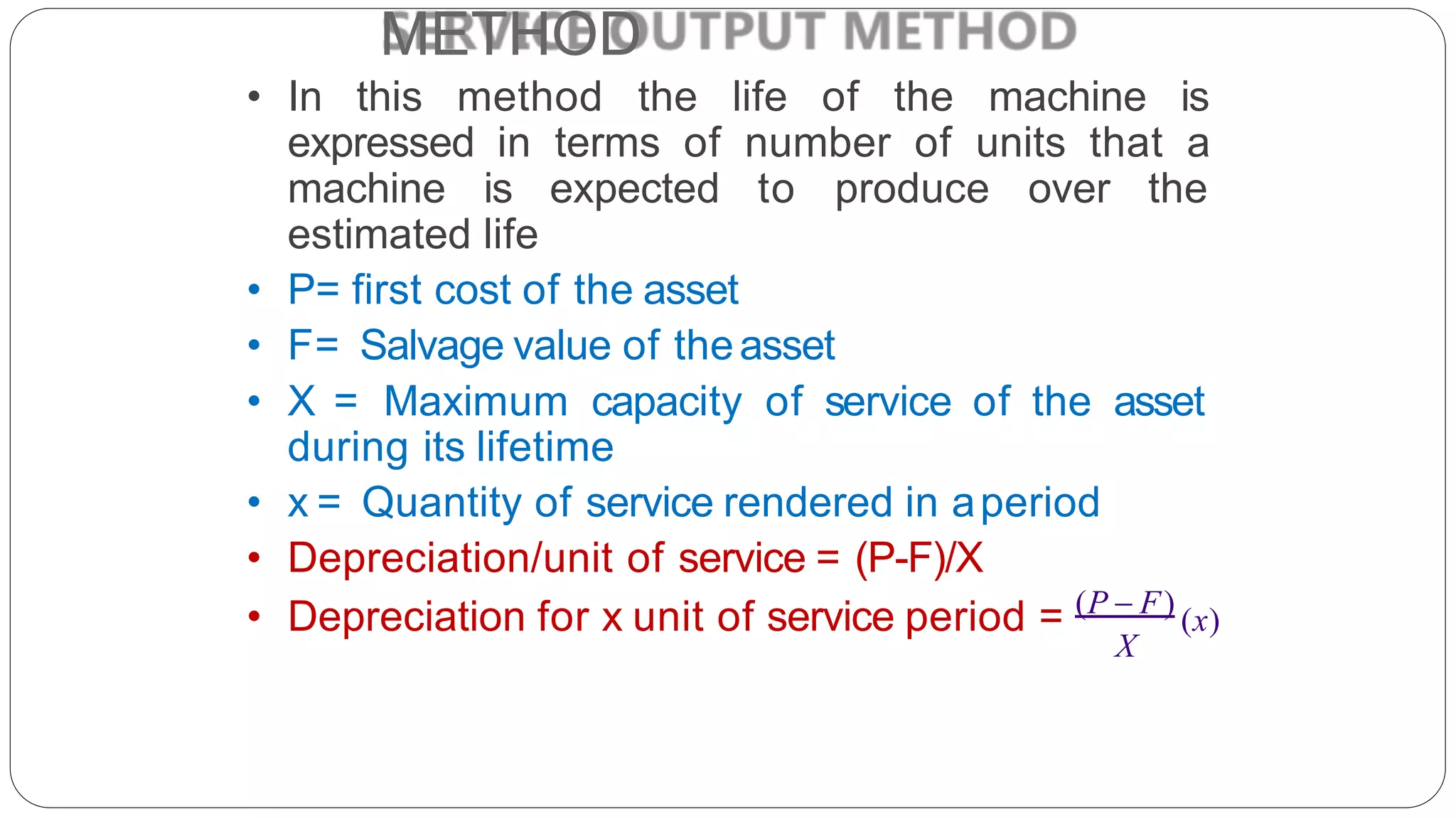

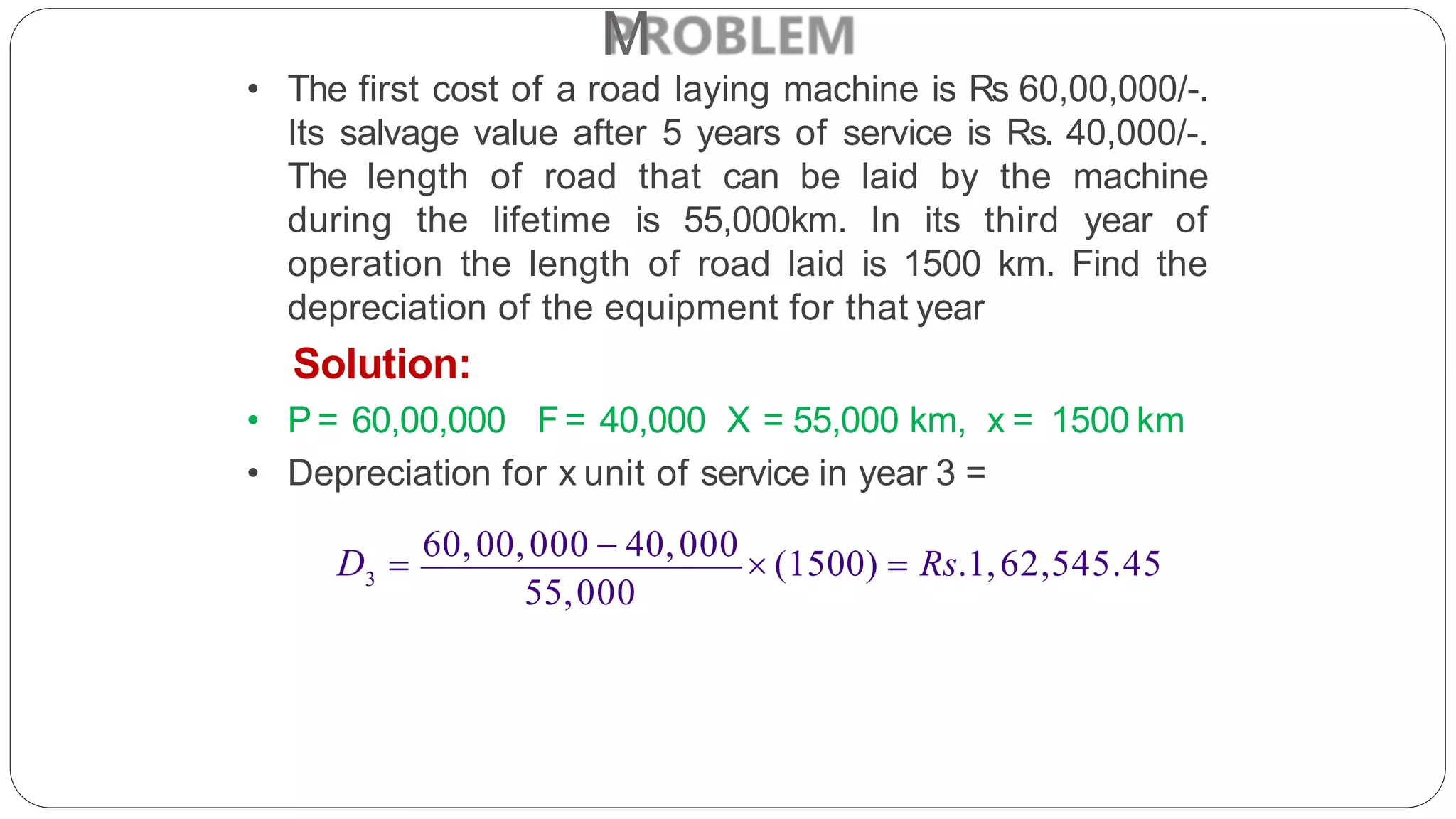

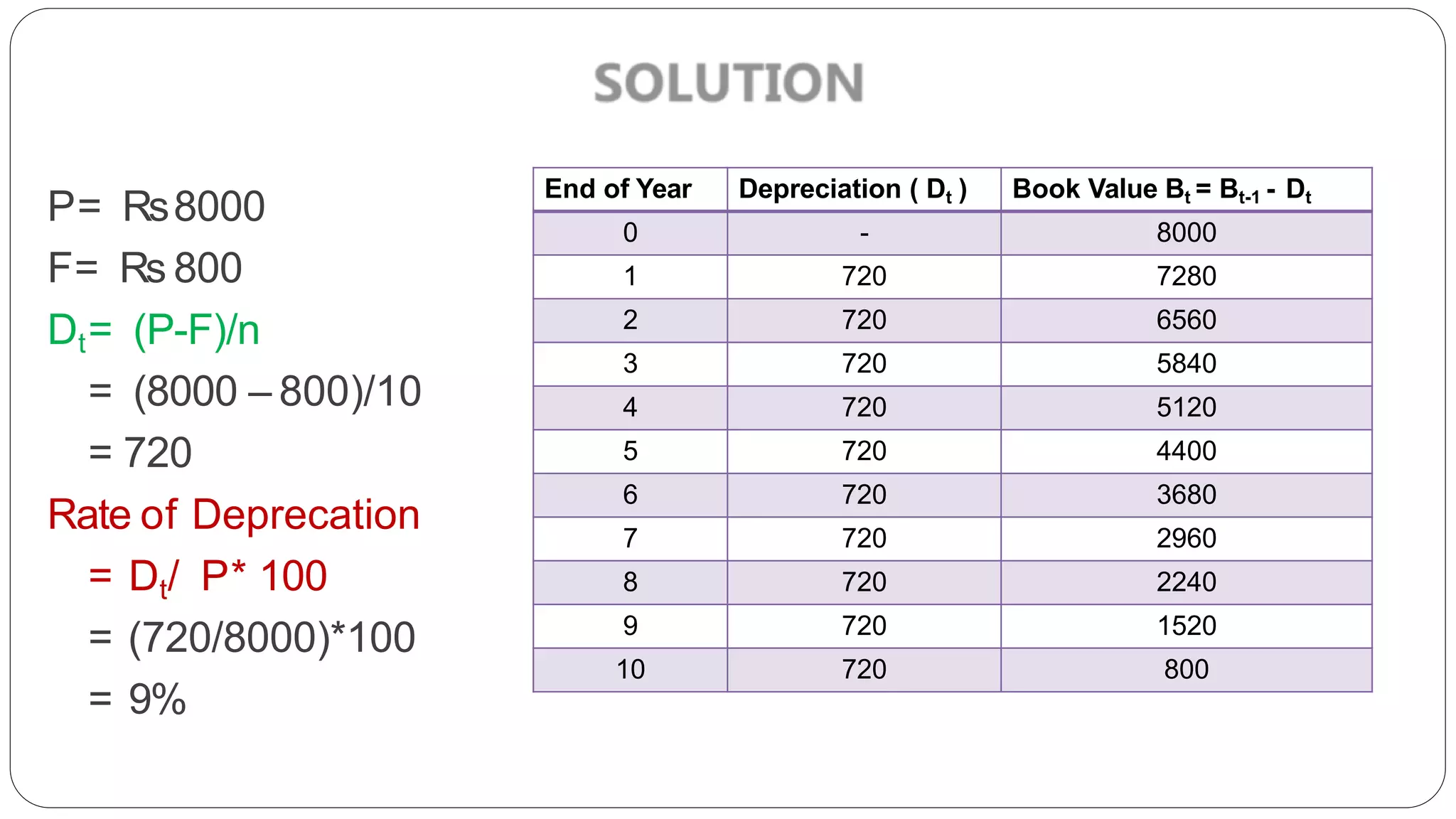

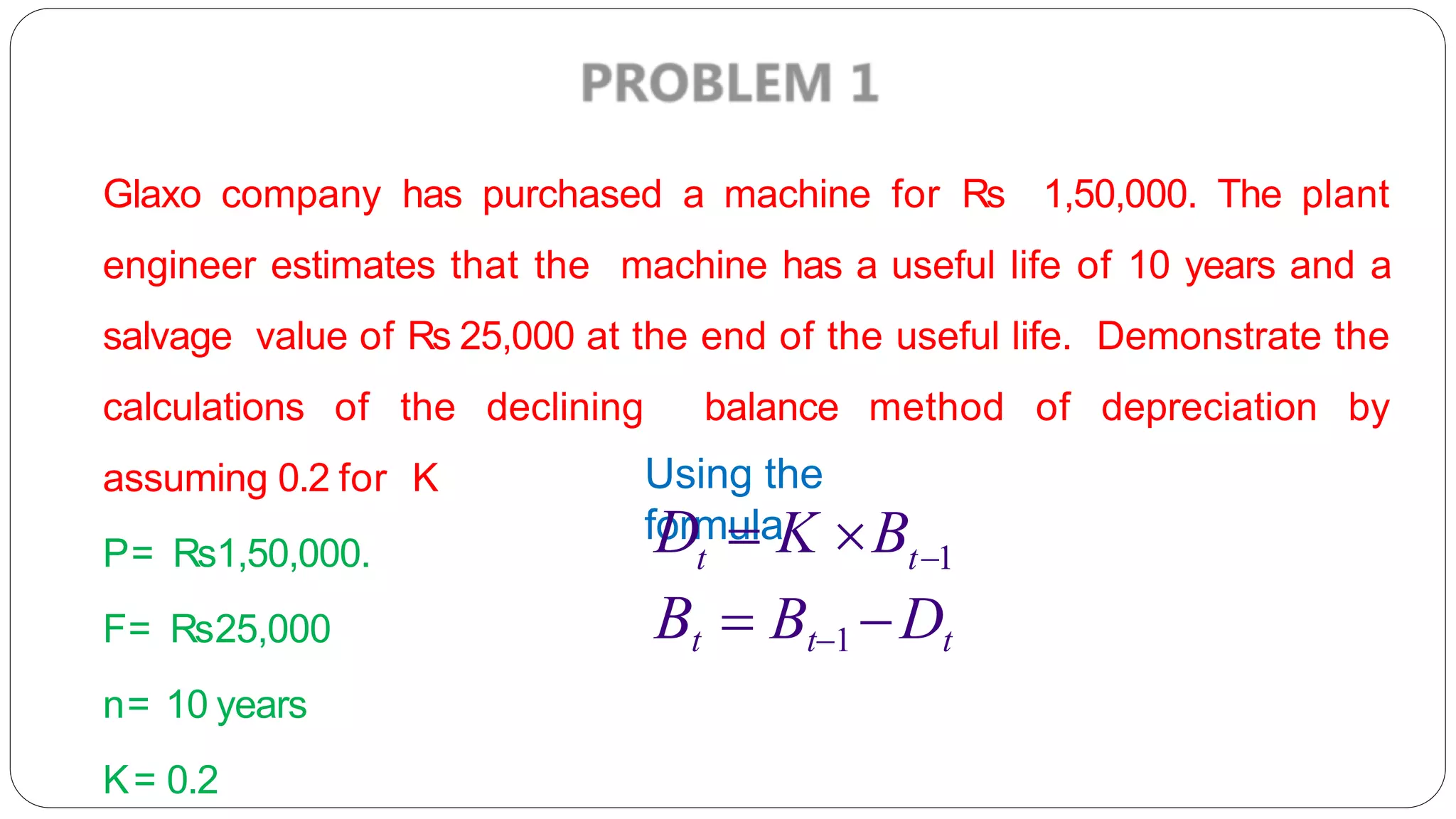

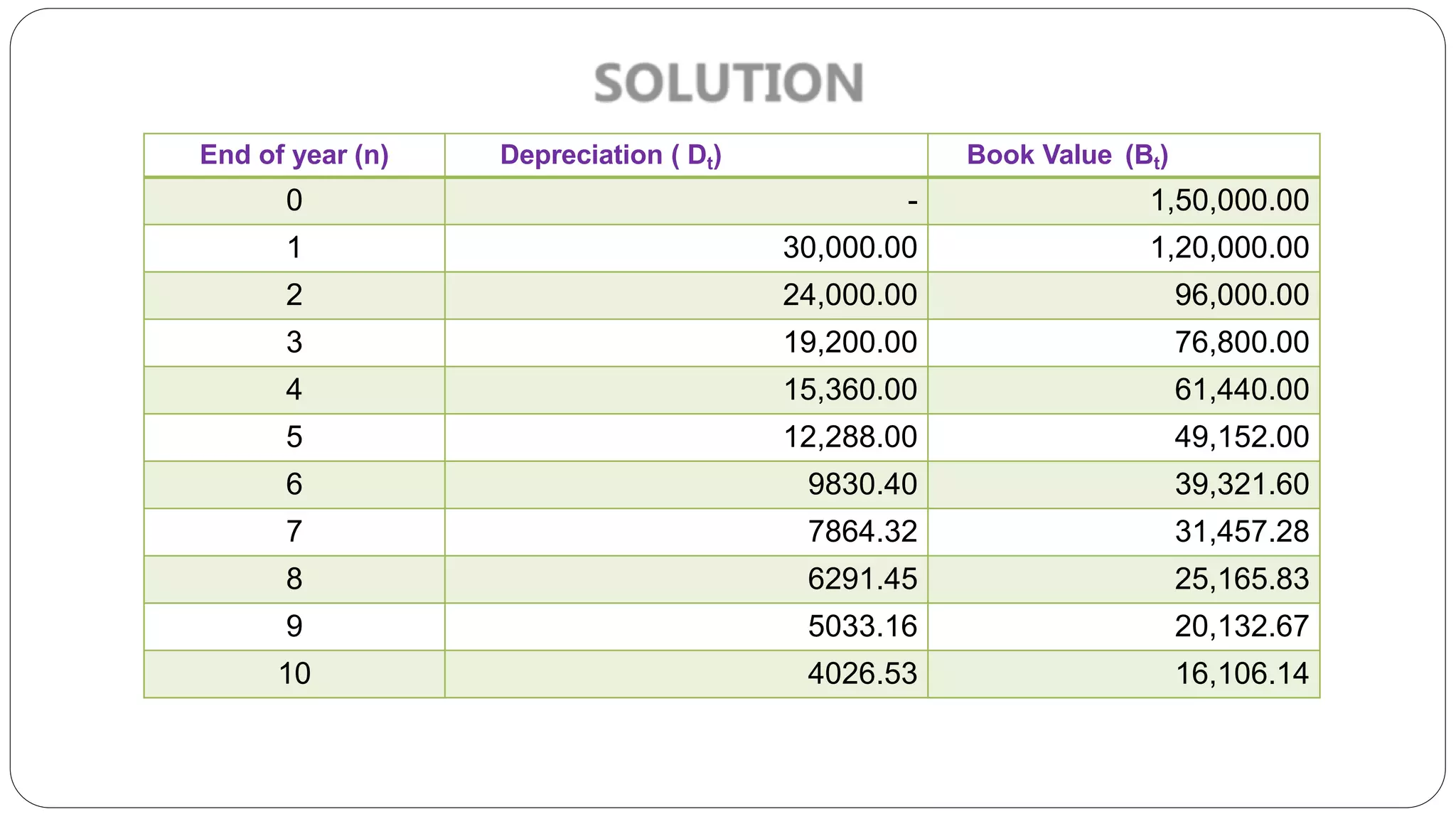

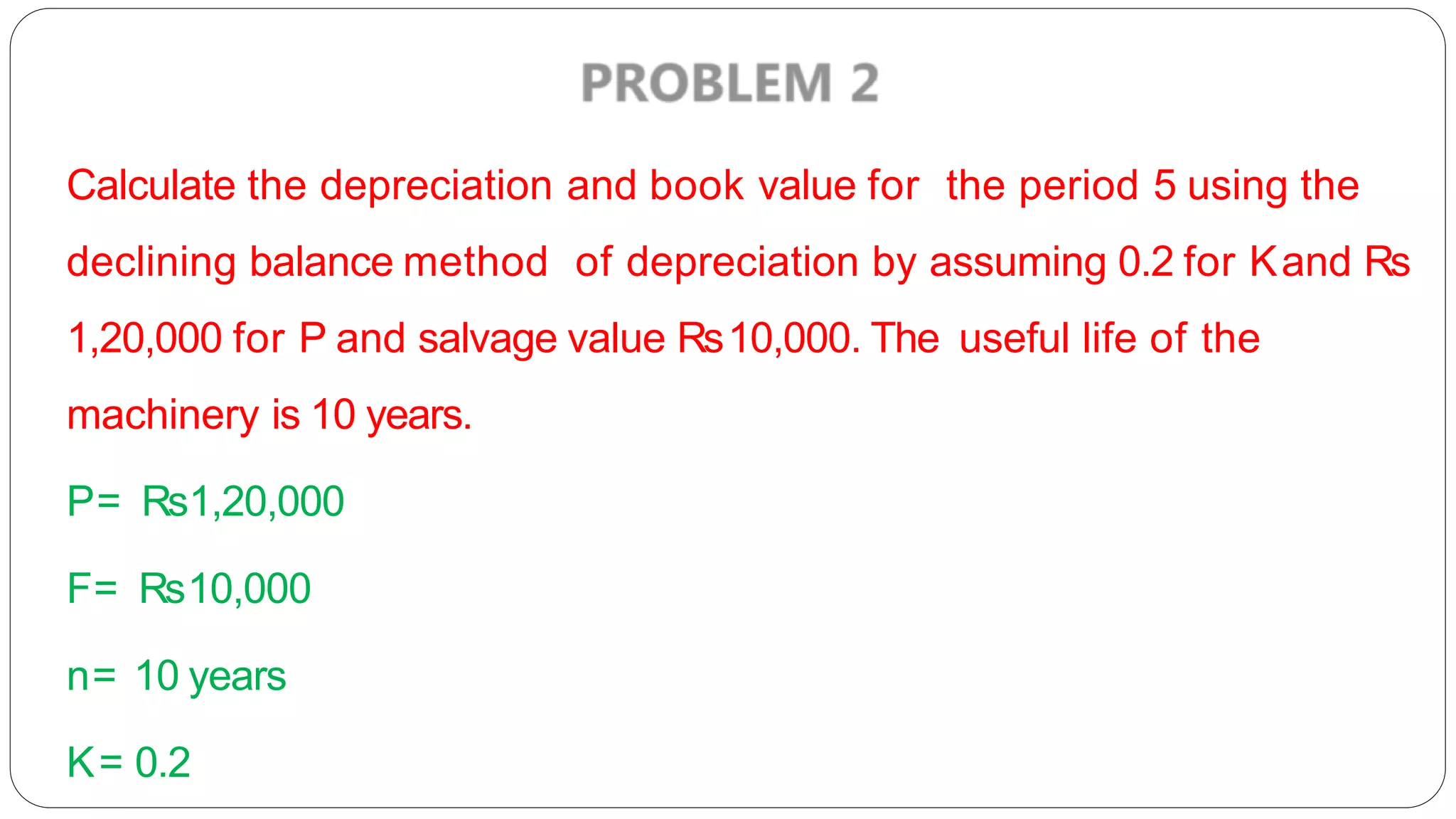

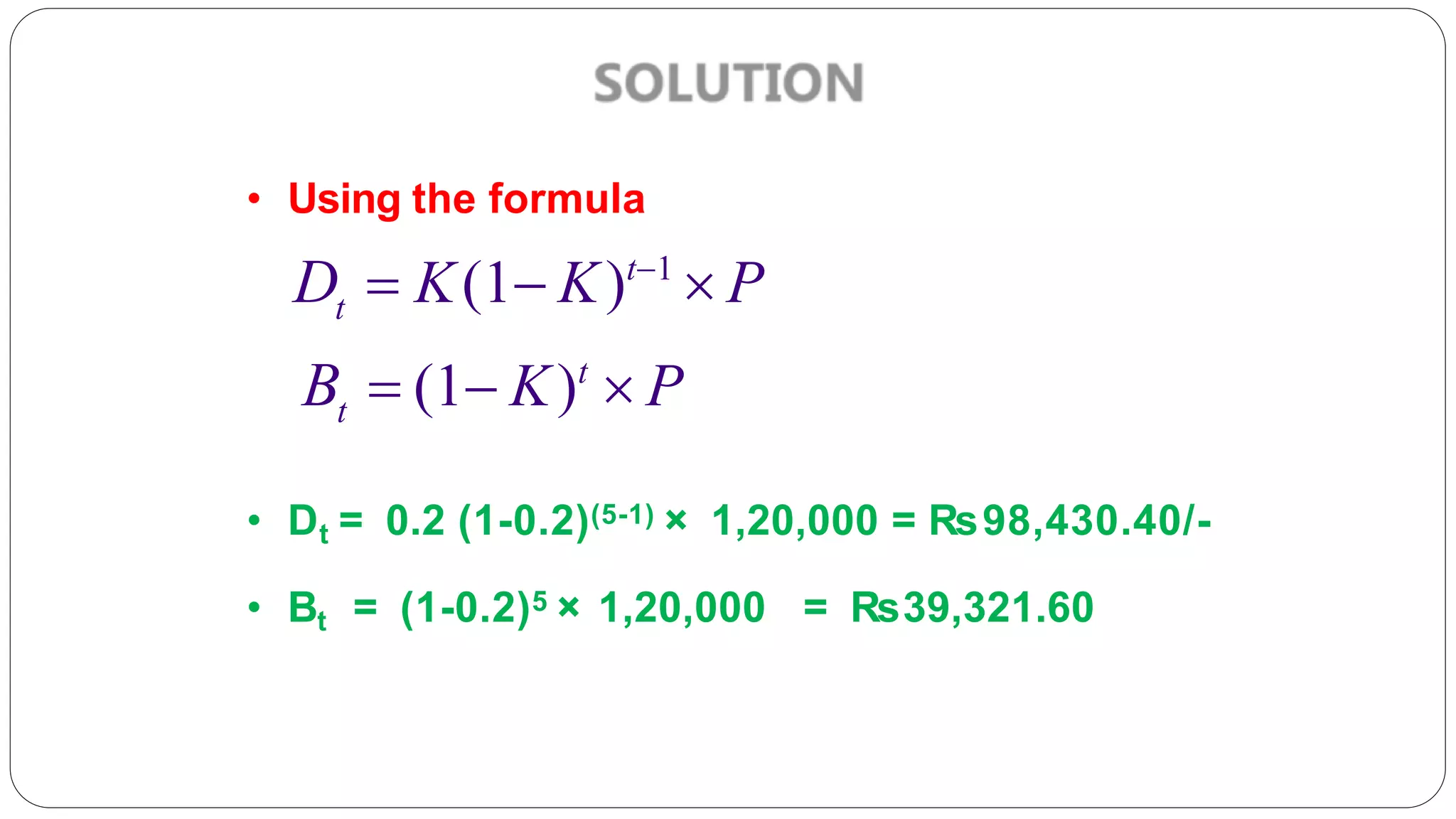

P= First cost of theasset

F= Salvage value of the asset

n = Life of the asset

Bt = Book value of the asset at the end of the periodti

Dt = Depreciation amount for the time period t

D

[P F]

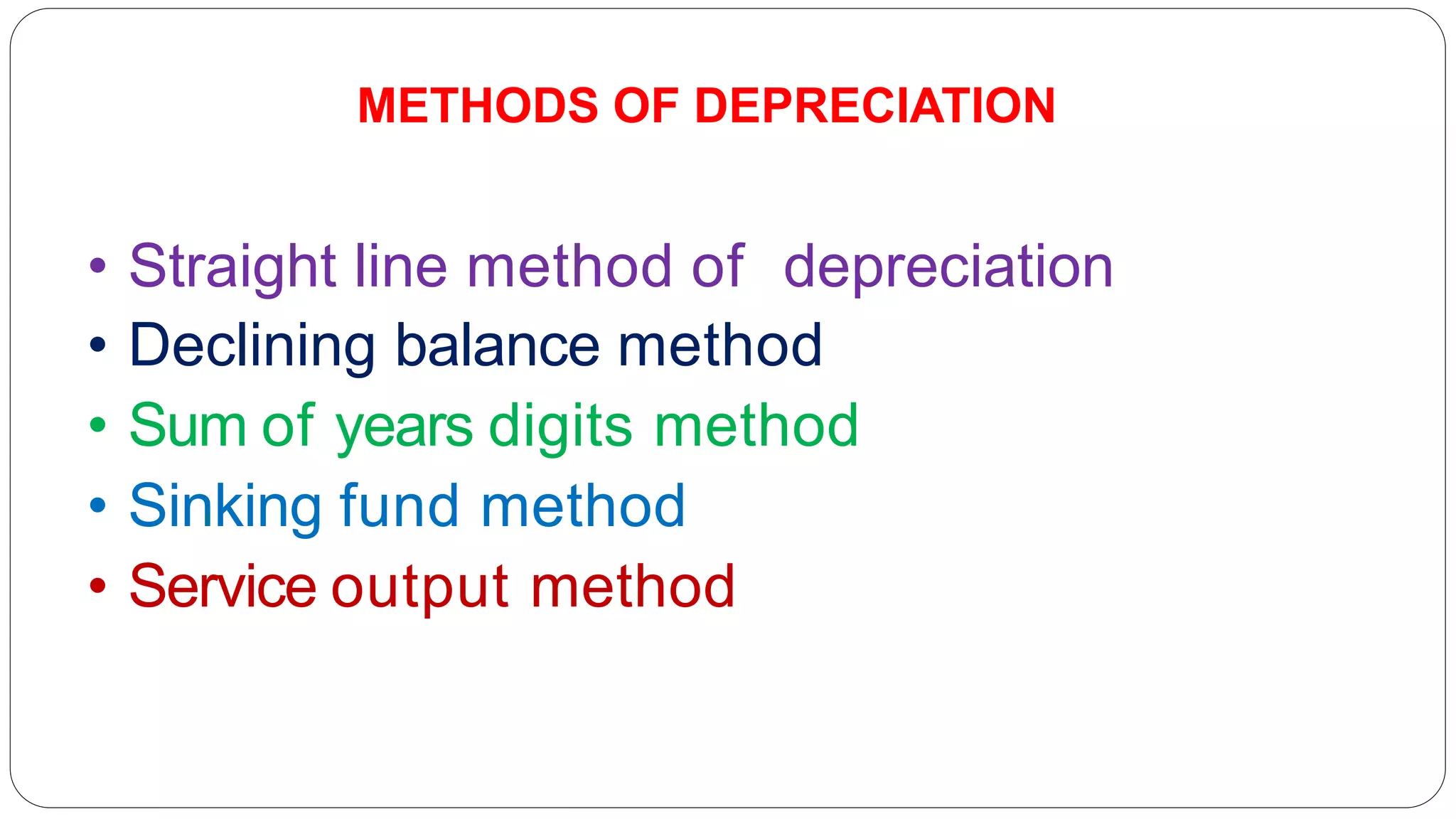

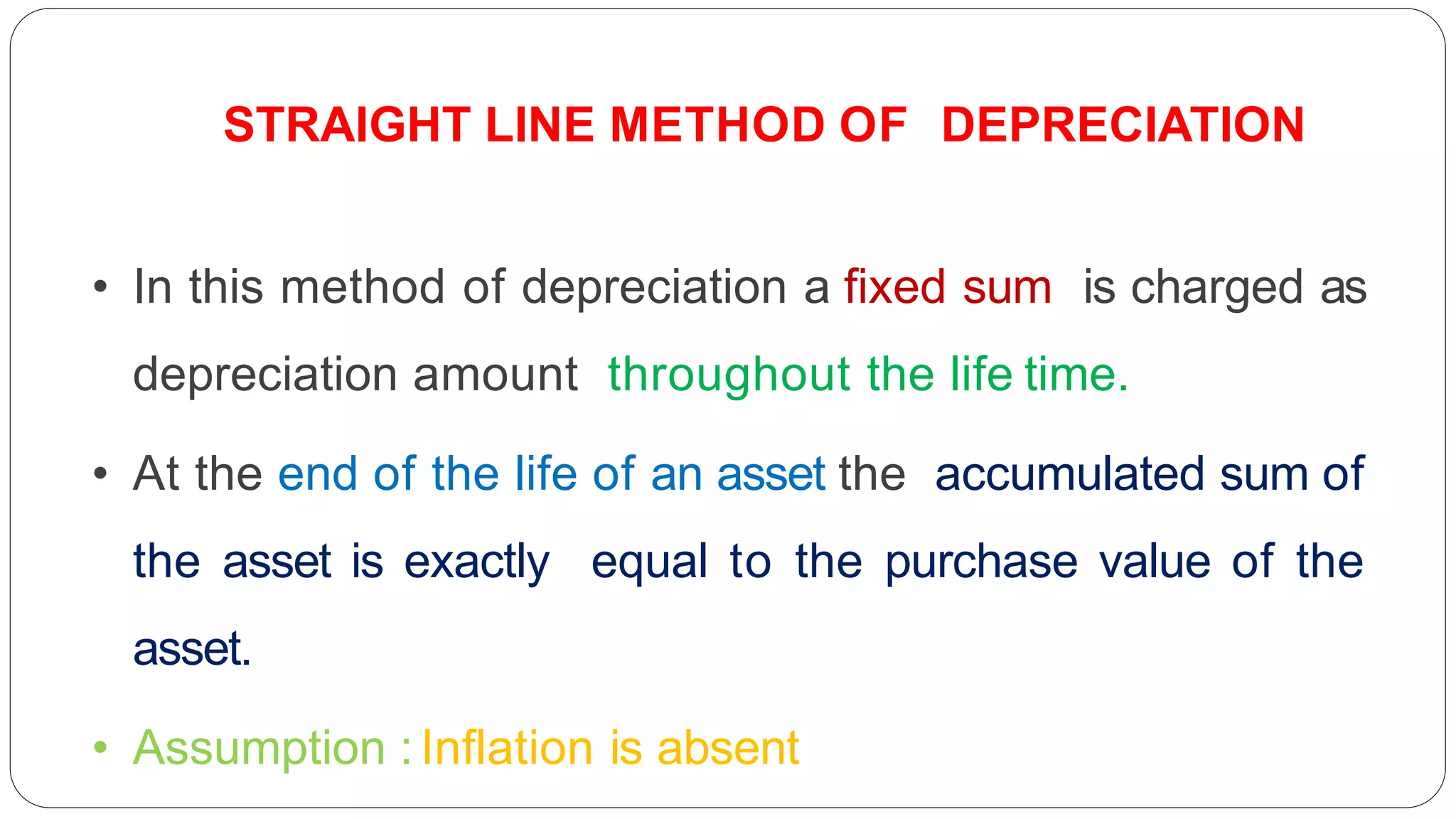

STRAIGHT LINE METHOD OF DEPRECIATION

Rate of Deprecation = Dt/ P* 100](https://image.slidesharecdn.com/ppceunit3-211117103659/75/PPCE-unit-3-ME8793-PROCESS-PLANNING-AND-COST-ESTIMATION-54-2048.jpg)

![P= Rs24,000 + Rs1000 = 25000

F= Rs5000/-

n = 10years

Dt = (P-F)/n = (25000-5000)/10 = 2000

Bt = 25,000 – 6 × (25000-5000)/10

Bt= Rs.13,000/-

n

t i 1 t

B B D P t [ P F ]](https://image.slidesharecdn.com/ppceunit3-211117103659/75/PPCE-unit-3-ME8793-PROCESS-PLANNING-AND-COST-ESTIMATION-58-2048.jpg)

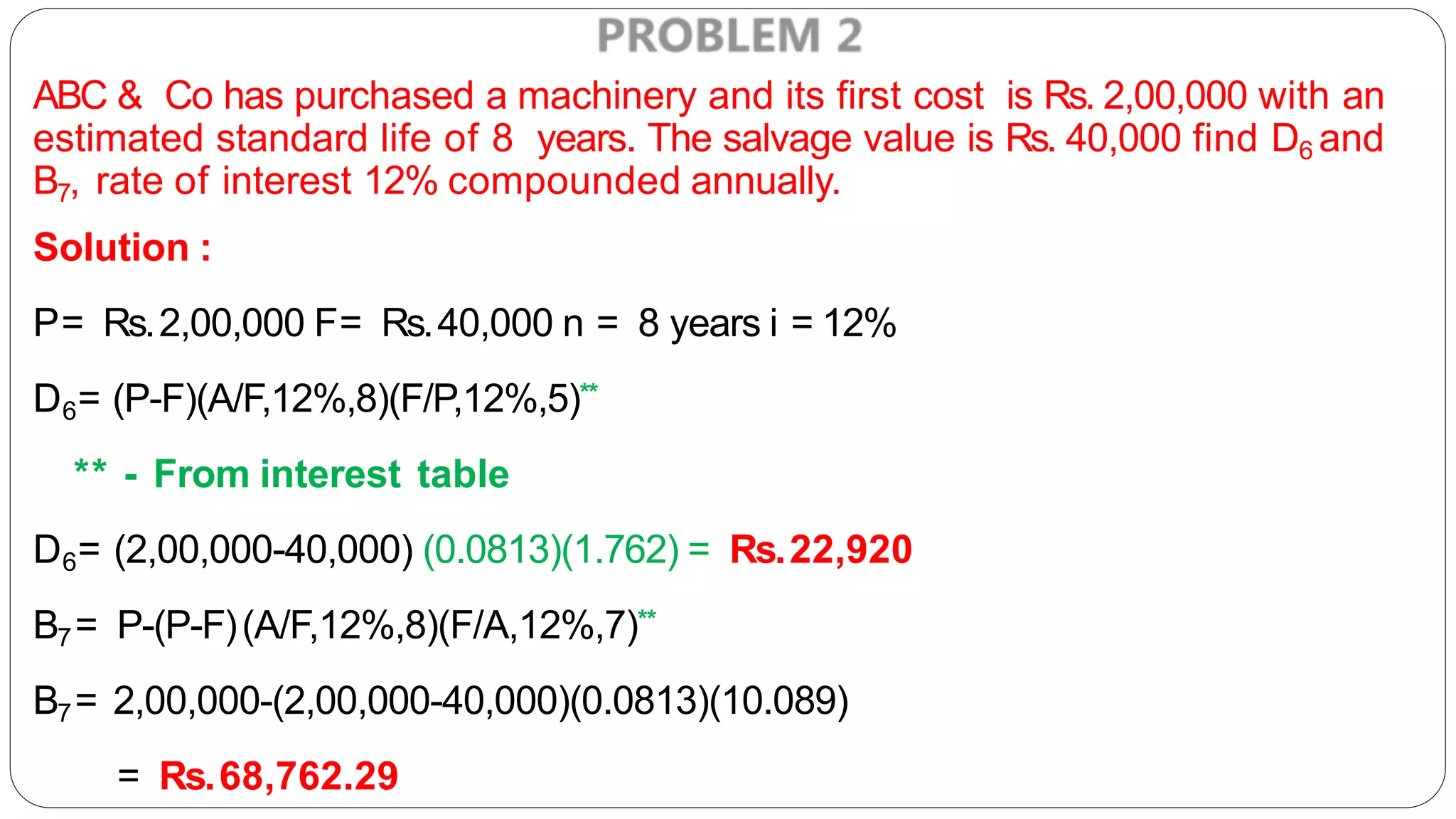

![P= first cost of the asset

F= salvage value of the asset

n= life of the asset

i = Rate of return compounded annually

A = Annual equivalent amount

Bt = Book value of the asset at the end of the period ‘t’

Dt = Depreciation amount at the end of the period ‘t’.

The loss of value of the asset (P-F) is made available in the form of

cumulative depreciation amount

A = (P-F)[A/F, i, n]

The fixed sum depreciated at the end of every time period earns an interest at

the rate of i% compounded annually

Dt = (P-F)(A/F, i ,n)(F/P,i,t-1)

Bt = P-(P-F)(A/F, i,n)(F/P,i,t-1)](https://image.slidesharecdn.com/ppceunit3-211117103659/75/PPCE-unit-3-ME8793-PROCESS-PLANNING-AND-COST-ESTIMATION-70-2048.jpg)

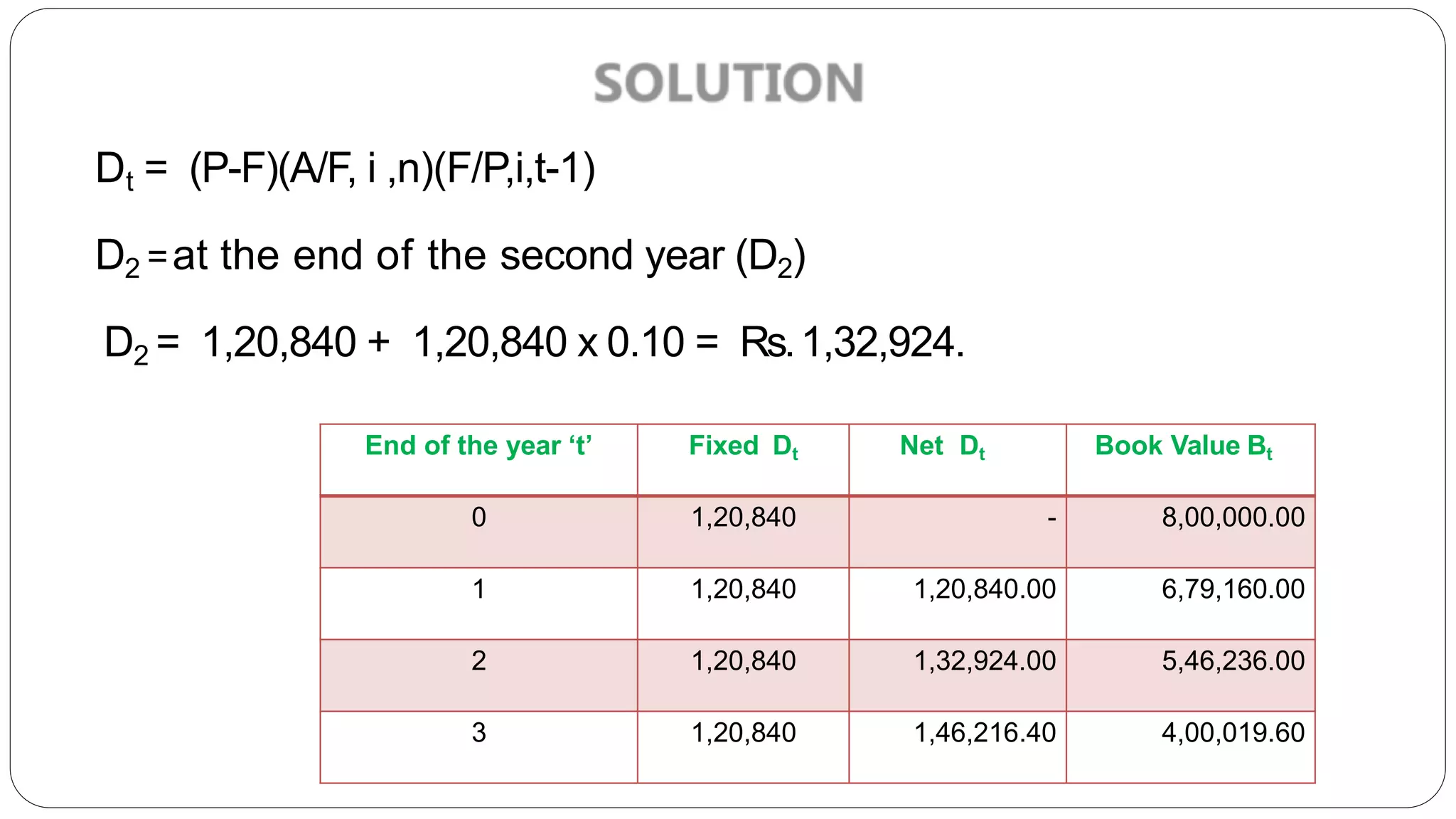

![P= Rs. 8,00,000

F = Rs.4,00,000

n = 3years

i = 10%

A = (P-F)[A/F, i, n]

A = (8,00,000-4,00,000) [A/F,10%,3] value from interest table is substituted

A = (8,00,000-4,00,000) x 0.3021 = Rs.1,20,840

Dt = (P-F)(A/F, i,n)(F/P,i,t-1)

Bt = P-(P-F)(A/F, i,n)(F/P,i,t)](https://image.slidesharecdn.com/ppceunit3-211117103659/75/PPCE-unit-3-ME8793-PROCESS-PLANNING-AND-COST-ESTIMATION-72-2048.jpg)