Downloaded 38 times

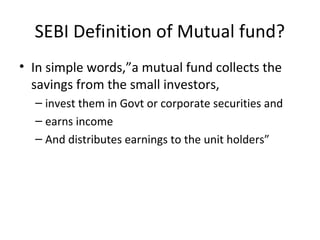

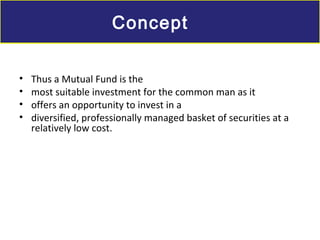

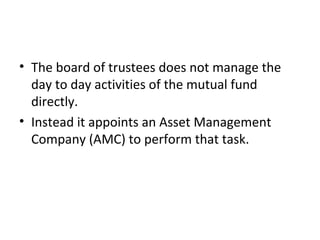

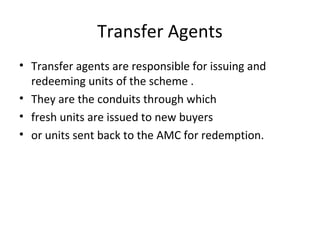

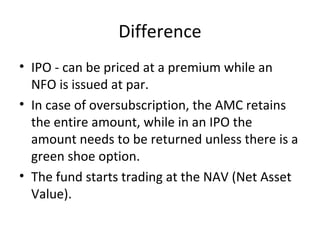

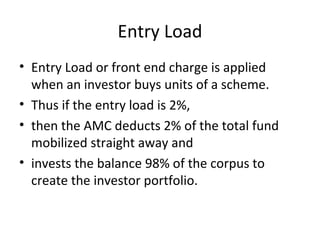

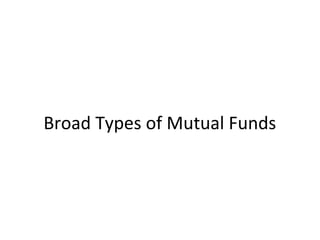

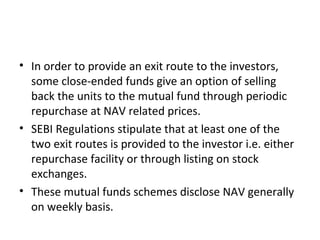

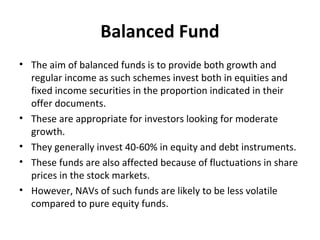

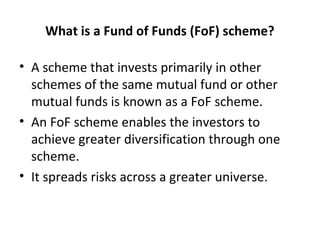

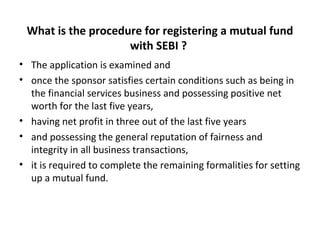

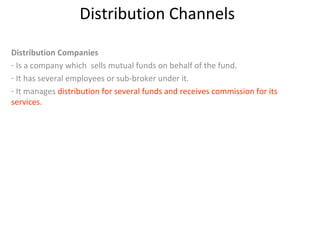

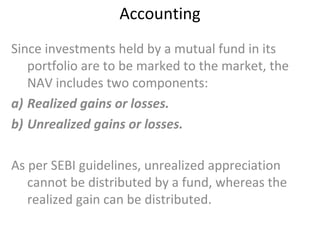

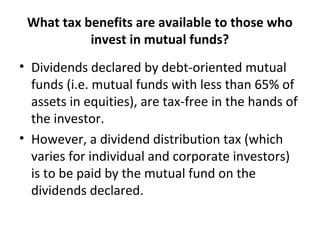

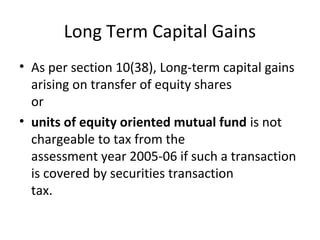

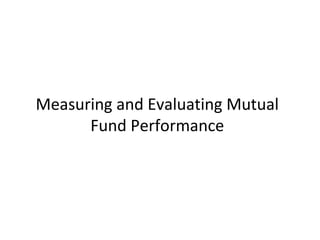

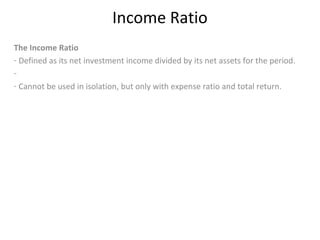

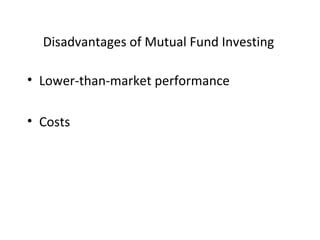

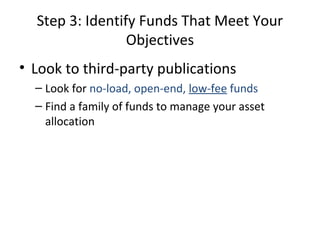

![Different Performance Measures

Change in NAV

-most commonly used by investors to evaluate fund performance and most

commonly published by fund managers.

-NAV Change in absolute terms:

(NAV at the end of period) – (NAV at the beginning of period)

NAV Change in percentage terms:

(Absolute change in NAV/NAV at the beginning of period) * 100

Annualised NAV Change:

{[(Absolute Change in NAV/NAV at the beginning)/months covered]*12}*100](https://image.slidesharecdn.com/mutualfundsnew-101108232745-phpapp02/85/Mutual-funds-new-75-320.jpg)

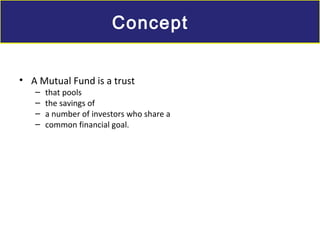

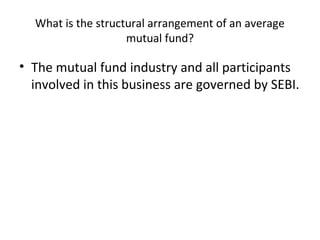

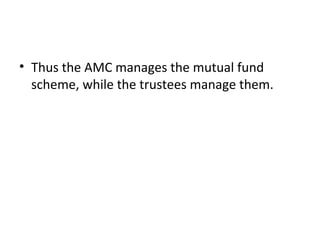

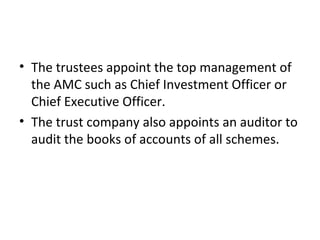

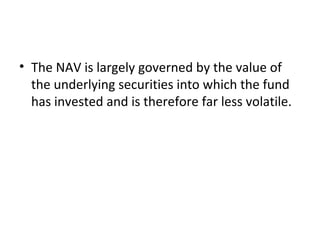

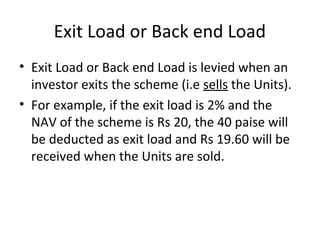

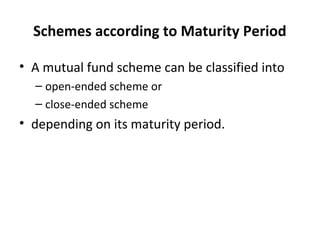

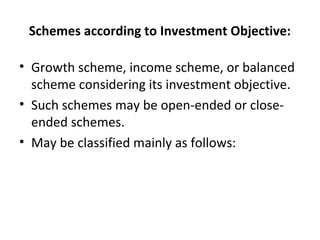

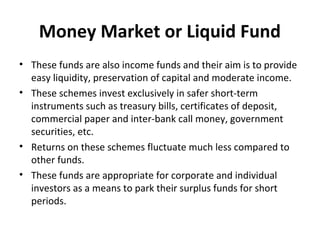

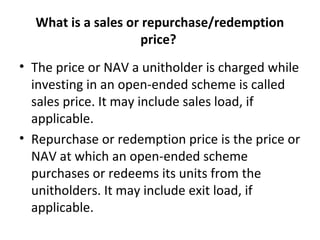

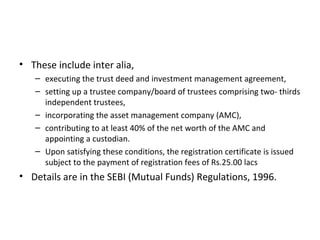

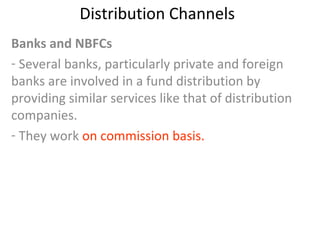

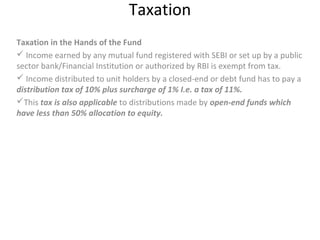

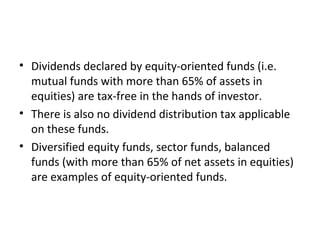

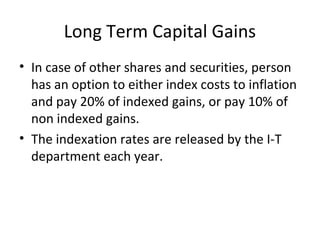

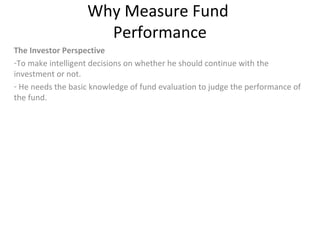

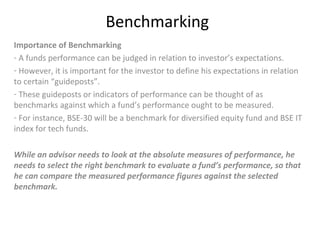

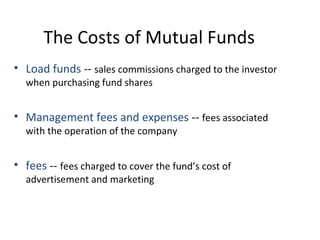

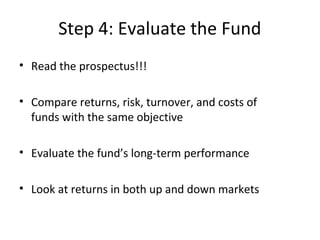

![Different Performance

Measures

No, percentage NAV change cannot give a correct picture as it does not take

into account the interim dividends paid. The correct measure here is Total

Return Method.

Total Return Method

- It takes into account the dividends paid in the interim period and is suitable for

all types of funds.

- It must be interpreted in the light of market conditions and investment

objective of the fund.

- Its limitation is that it ignores the fact that distributed dividends also get

reinvested if received during the year.

Total Return is:

[(Distributions + Change in NAV)/NAV at the beginning of the period]* 100](https://image.slidesharecdn.com/mutualfundsnew-101108232745-phpapp02/85/Mutual-funds-new-76-320.jpg)

1. A mutual fund is a trust that pools savings from investors and invests them in stocks, bonds, and other securities. 2. SEBI regulates mutual funds in India and defines a mutual fund as a trust formed by a sponsor to raise money through the sale of units to the public and invest in securities. 3. The money collected is invested in capital market instruments and the income earned is shared by unit holders proportionate to their investment. This provides investors an opportunity to invest in a diversified basket of securities at low cost.