Downloaded 824 times

![shareholders

(iii) shareholders holding not less than [three-

fourths] in value of the shares in the

amalgamating company or companies (other

than shares already held therein immediately

before the amalgamation by, or by a nominee

for, the amalgamated company or its

subsidiary)

become shareholders of the amalgamated

company by virtue of the amalgamation,](https://image.slidesharecdn.com/taxissuesinmergersandacquisitions-101109003500-phpapp01/75/Tax-issues-in-mergers-and-acquisitions-10-2048.jpg)

![Credit for tax paid

Case Law –Modipon Ltd. Vs DCIT [1995]

54ITD 433(Del)

Benefit of any tax paid as Advance Tax

or Tax deducted at Source of the

amalgamating company would be available

for adjustment against the income of the

amalgamated company consequent

inclusion of such income of the

amalgamating company as income of the

amalgamated company after amalgamation.](https://image.slidesharecdn.com/taxissuesinmergersandacquisitions-101109003500-phpapp01/75/Tax-issues-in-mergers-and-acquisitions-26-2048.jpg)

This document discusses various tax issues that arise in mergers and acquisitions under Indian tax law. It covers topics like the meaning of amalgamation, capital gains tax exemptions for amalgamations, treatment of losses and depreciation for the amalgamated company, international tax issues like transfer pricing and thin capitalization. It provides an overview of the key domestic tax provisions around amalgamations, demergers and slump sales. It also gives a brief introduction to concepts of international taxation like offshore financial centers and their implications.

Introduction to tax issues in M&A, including structure of the presentation, domestic tax provisions, and international taxation basics.

Focus on types of restructuring, such as organic and inorganic, including details on amalgamation definitions and implications for property, liabilities, and shareholders.

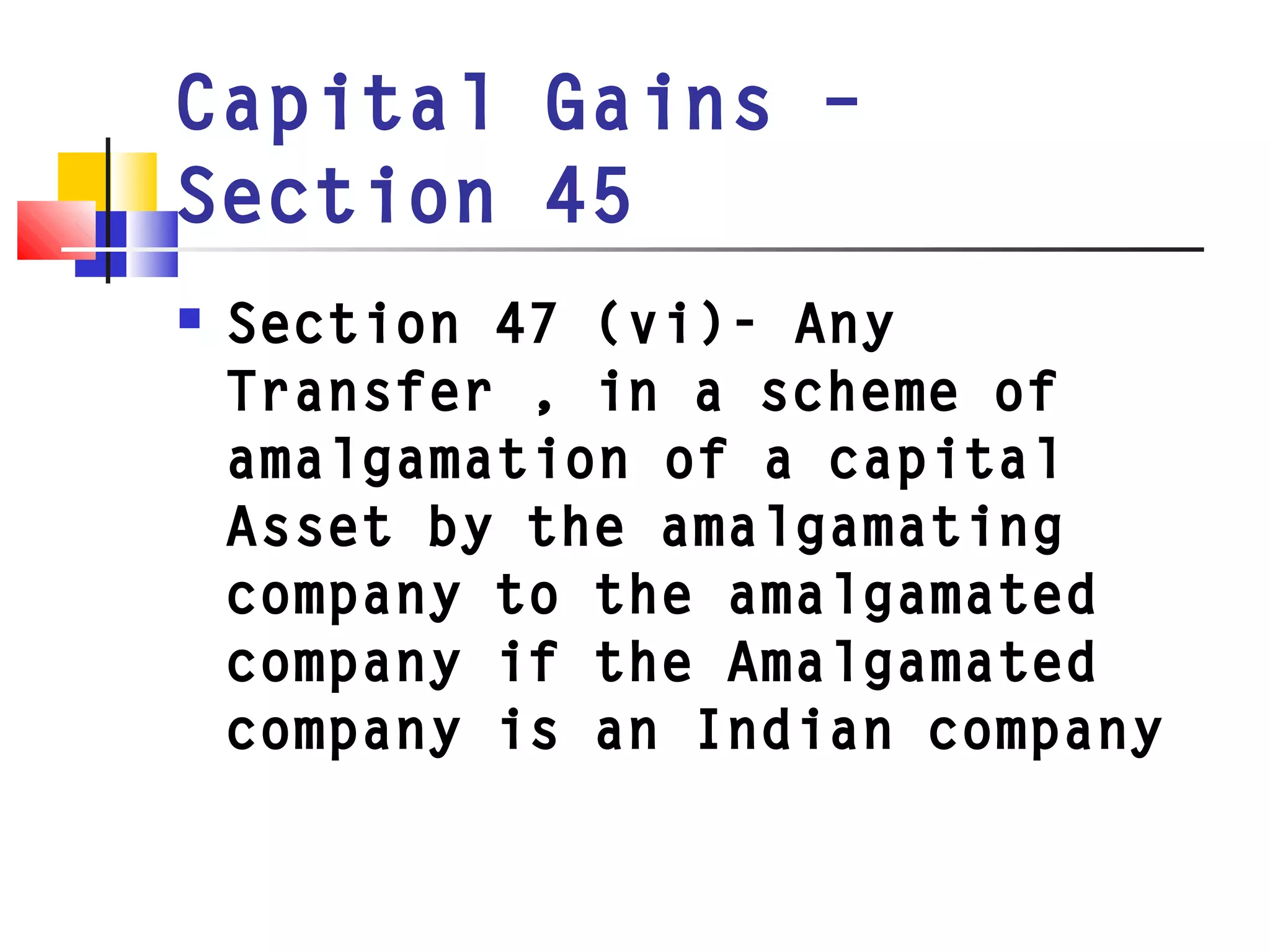

Details exceptions in amalgamation, capital gains taxation under Section 45, and subsequent transfer regulations including combined asset cost and indexation.

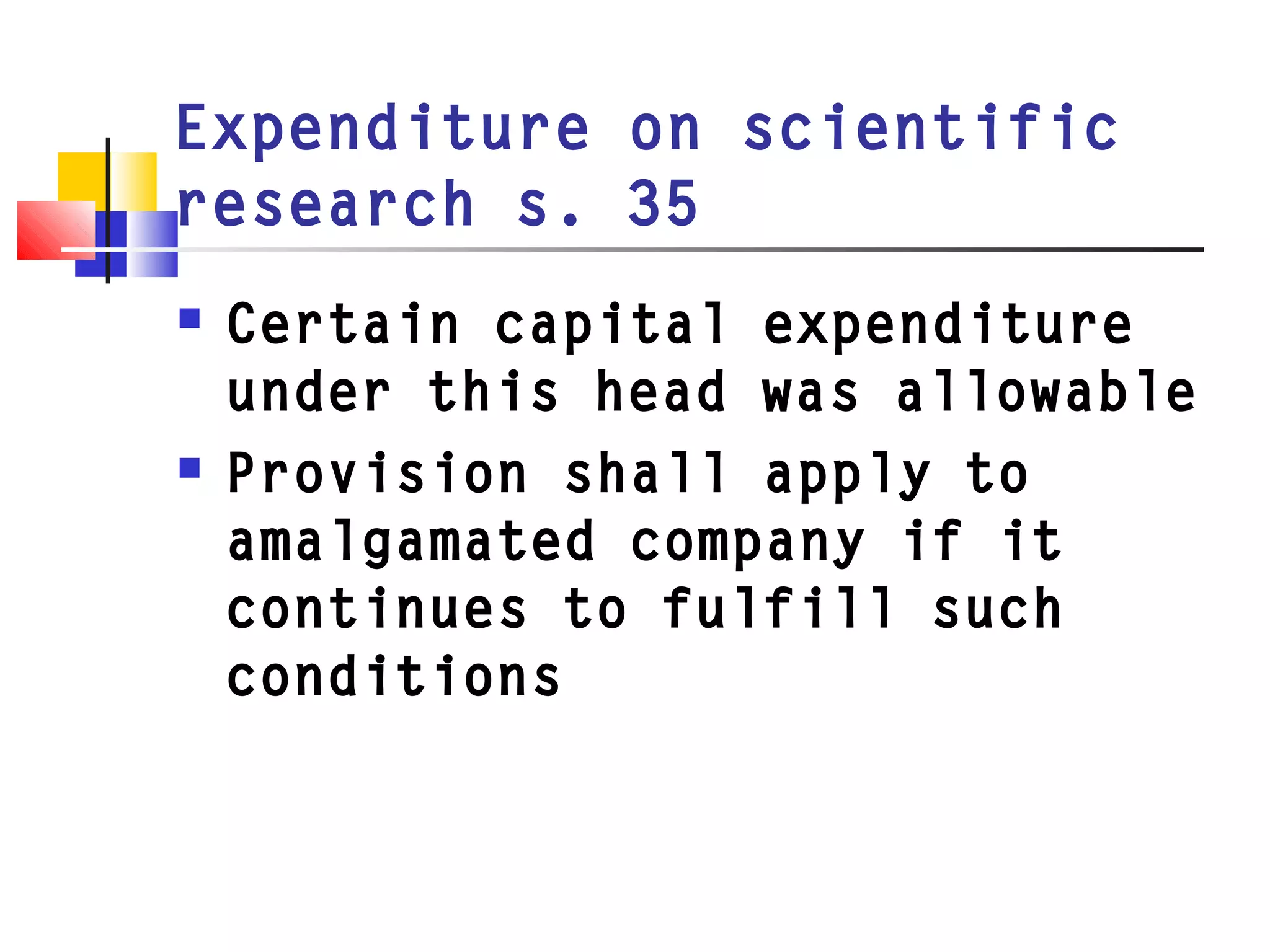

Discussion on admissibility of expenses, investment and development allowances, scientific research deductions, and handling of accumulated losses post-amalgamation.

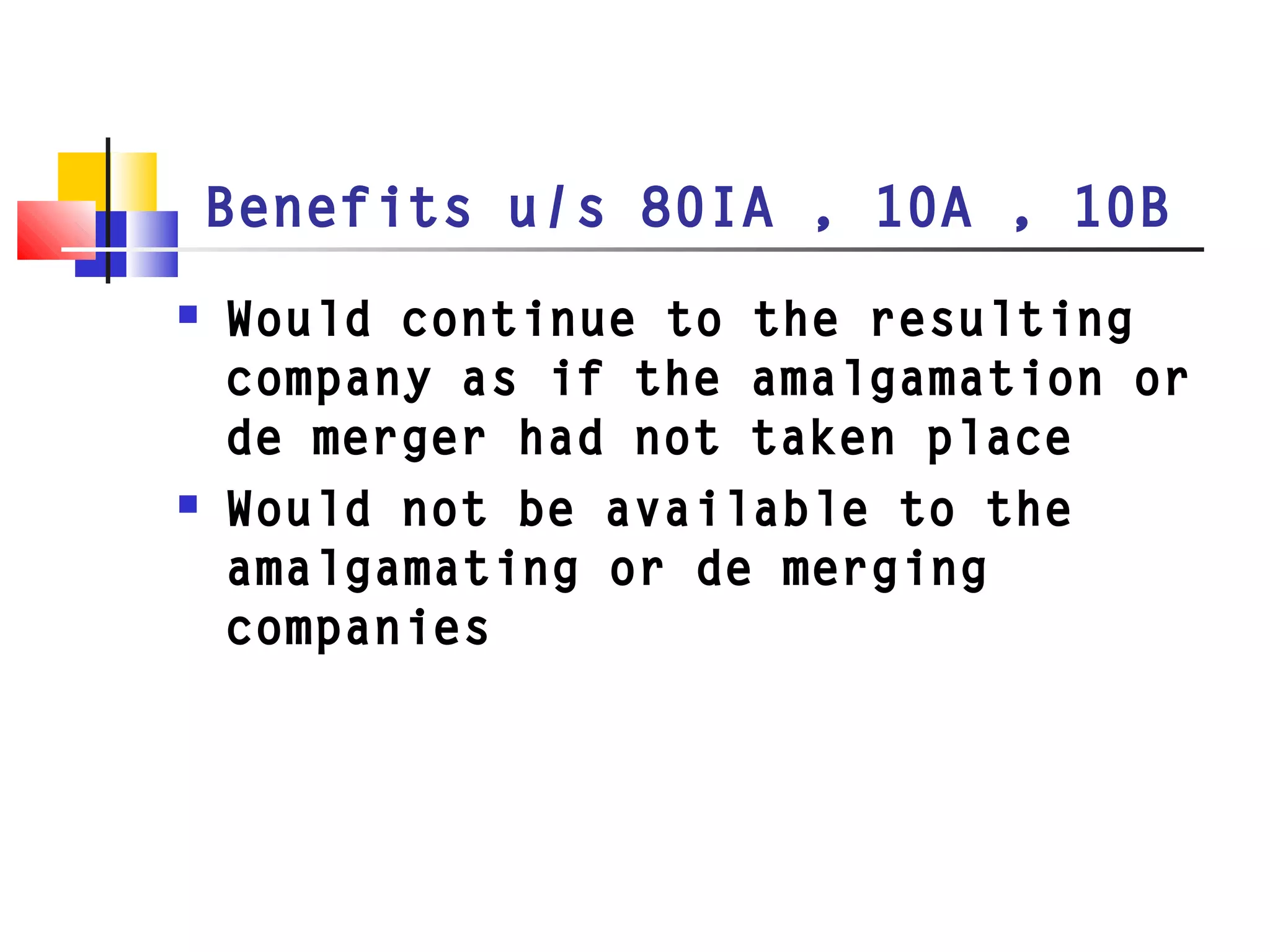

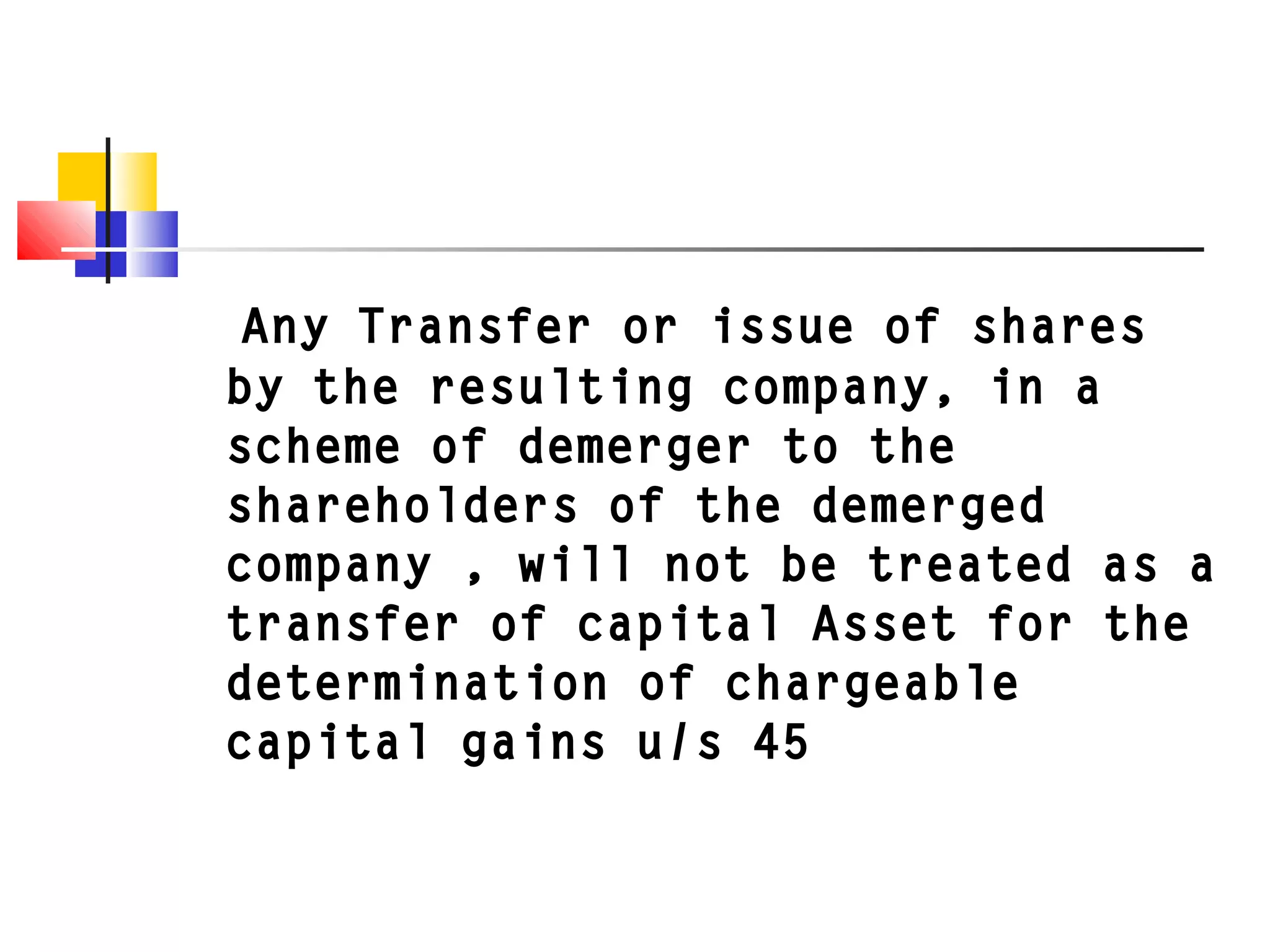

Explanation of tax treatment under the IT Act for demergers, including the carry-forward of losses and tax implications on share transfers.

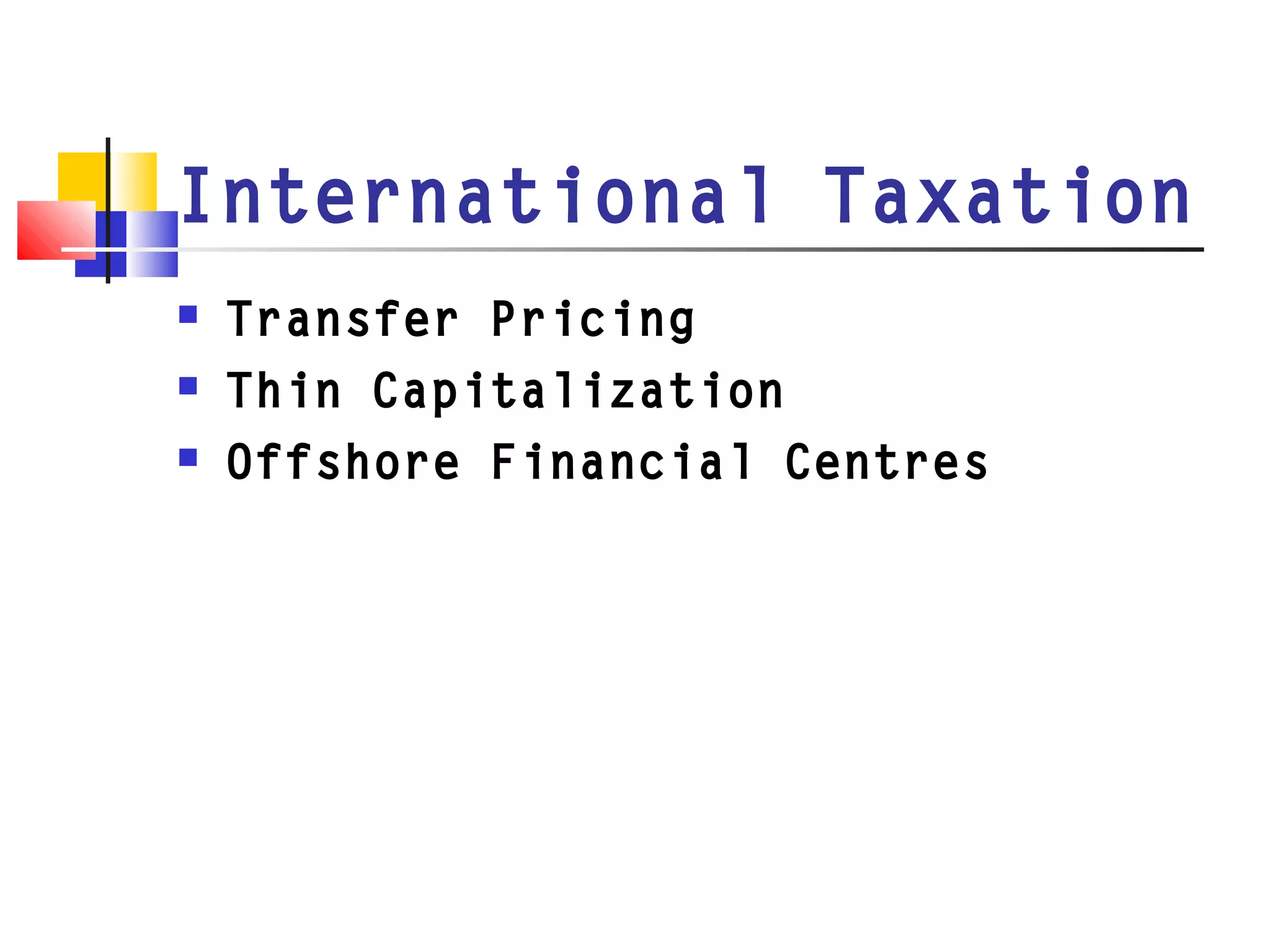

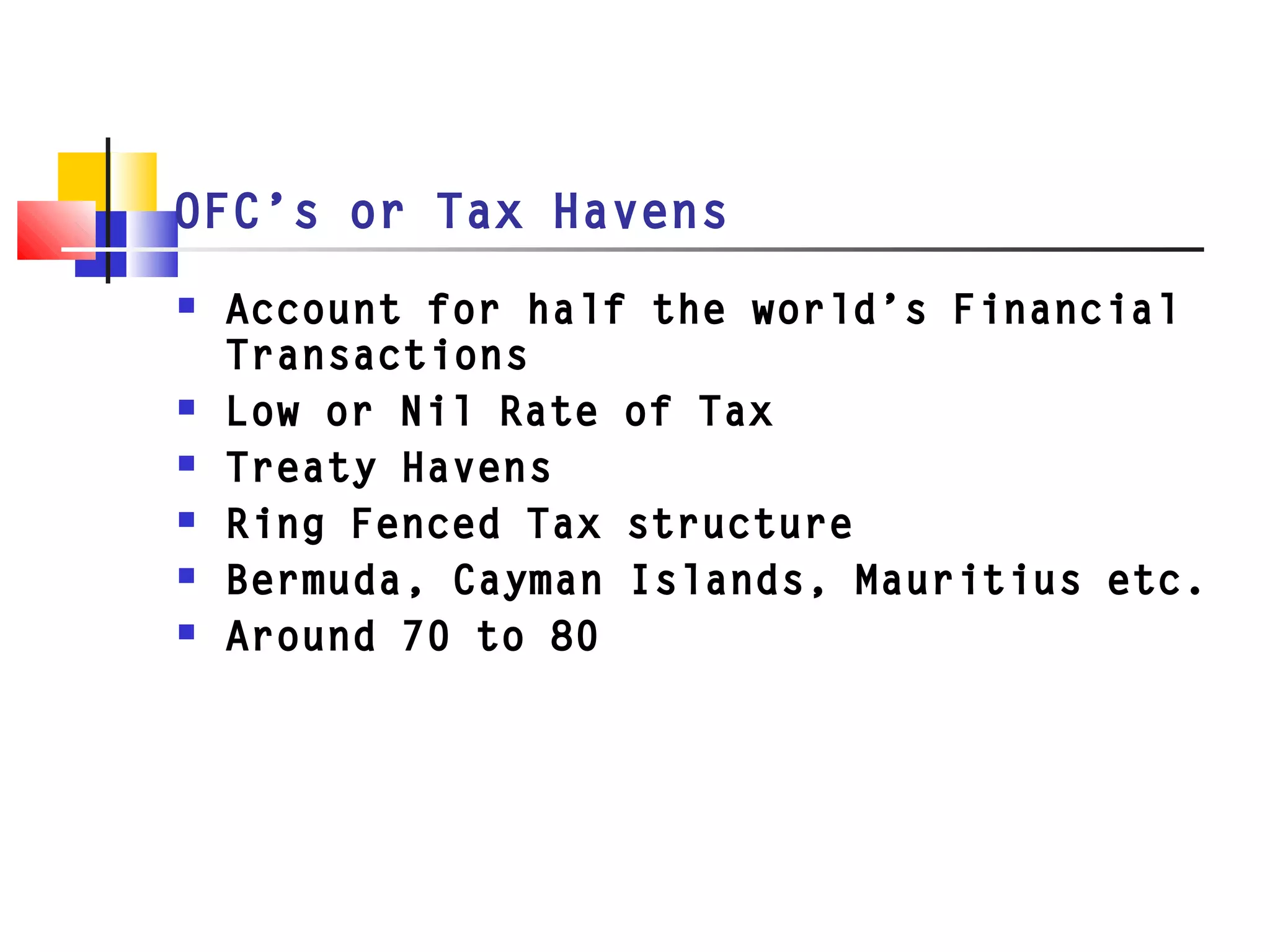

Definition of slump sales, international taxation concepts including transfer pricing, thin capitalization, and offshore financial centers.

![Tax[1]](https://cdn.slidesharecdn.com/ss_thumbnails/tax1-091005072254-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)