Downloaded 84 times

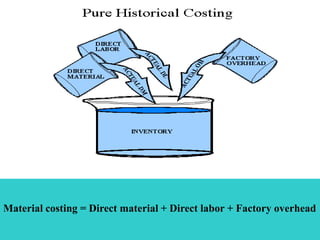

This report summarizes Bisleri International's material costing and strategies to reduce costs. It provides an overview of the company and its products. Material costs typically represent 65-70% of production costs. The report analyzes Bisleri's material costing methodology and identifies areas for cost reduction, including labor costs, vendor selection, inventory management, and procurement savings. It recommends opportunities like price restructuring, periodic purchasing during price lows, and perpetual inventory tracking to optimize material management and lower costs. Effective material control and cost reduction are crucial to ensure steady supply and production for the company.