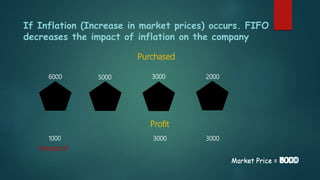

This document discusses inventory valuation methods. It explains that inventory includes raw materials, work in progress, and finished goods. The two main inventory valuation methods are LIFO (last in, first out) and FIFO (first in, first out). Under LIFO, the most recently produced goods are sold first, lowering costs when prices are rising. FIFO sells older goods first, which prevents expiration of inventory and decreases the impact of inflation. The document provides examples to illustrate how inventory quantities and costs are tracked under each method.