Downloaded 1,228 times

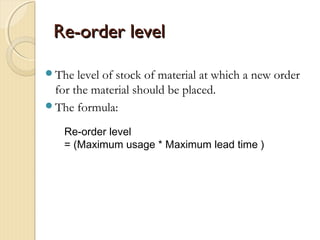

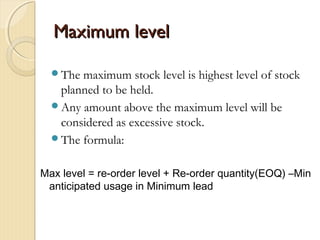

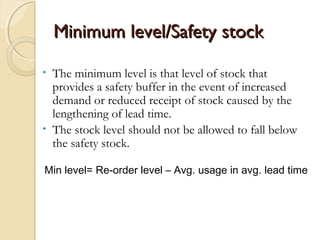

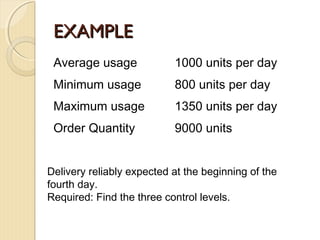

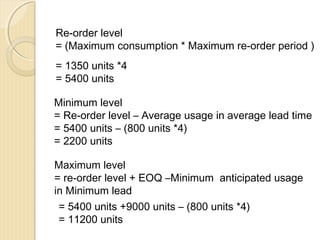

This document discusses materials management and inventory control. It defines key terms like materials, inventory, and material control. The objectives of material control are to have the right materials available when needed and to purchase efficiently. Different methods for valuing stock are described, including FIFO, LIFO, weighted average, and specific identification. The economic order quantity formula is provided to determine optimal order sizes. Level setting establishes maximum, minimum, and reorder levels to avoid overstocking or understocking. An example calculation demonstrates how to determine these three control levels.