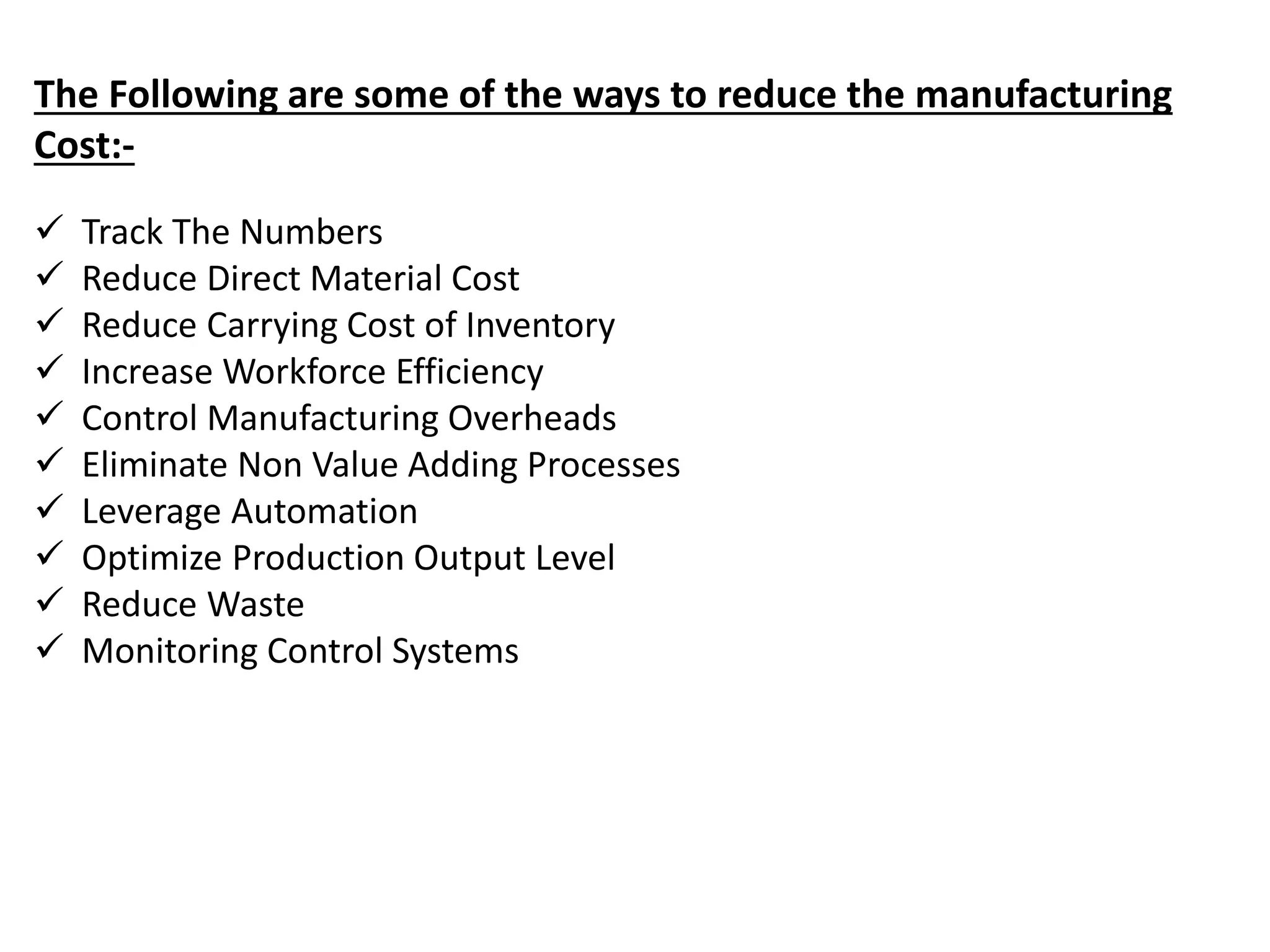

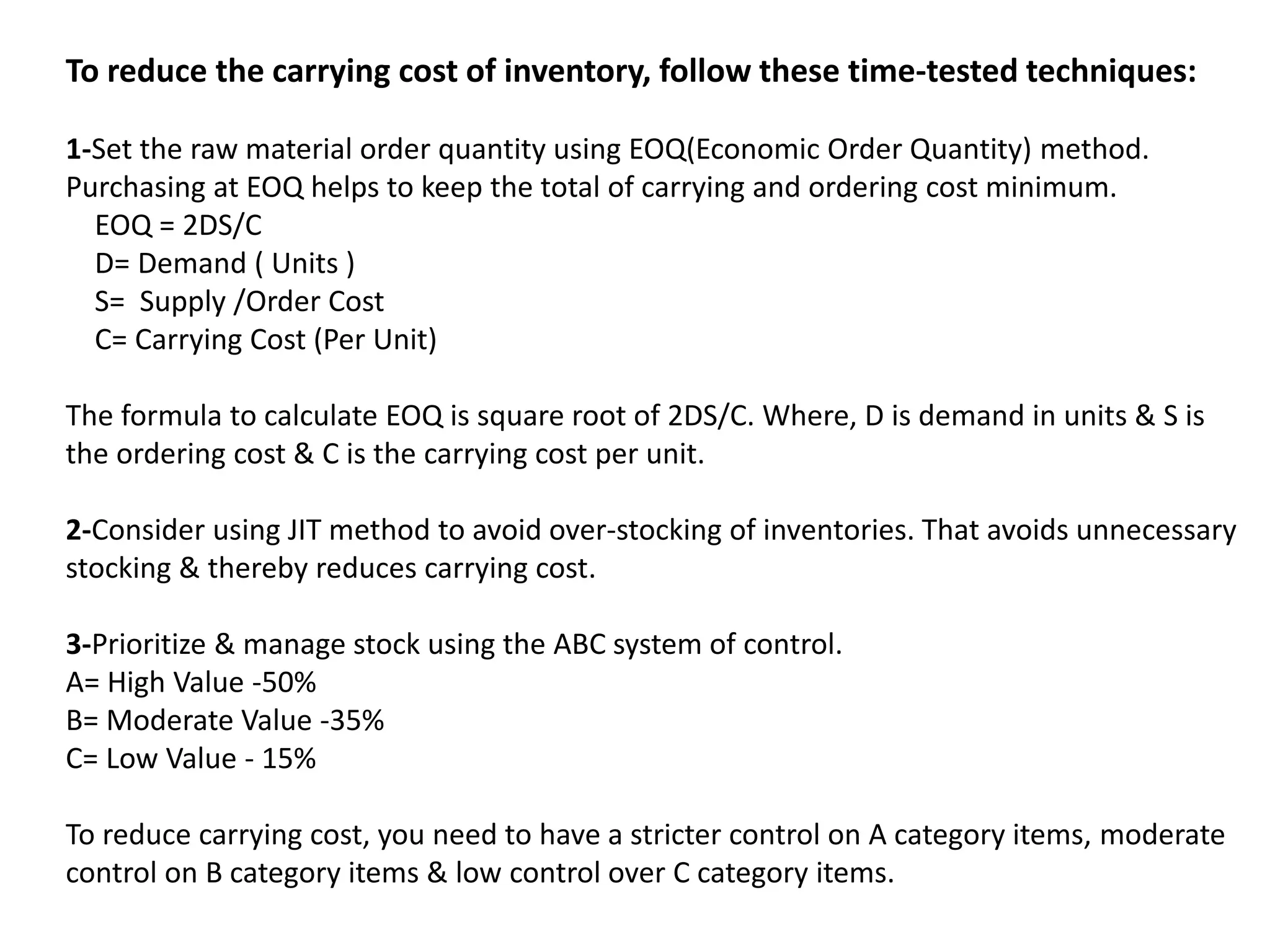

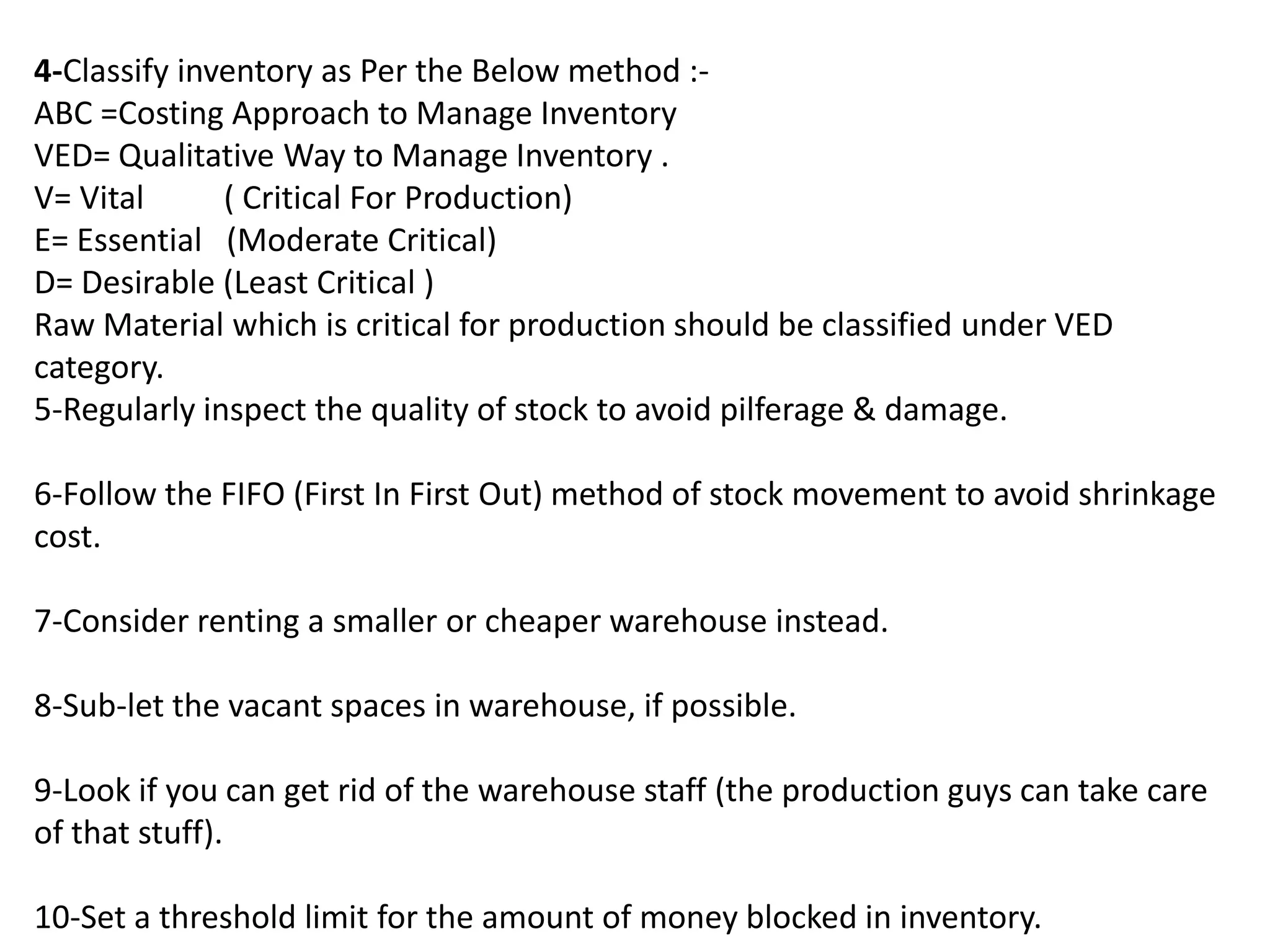

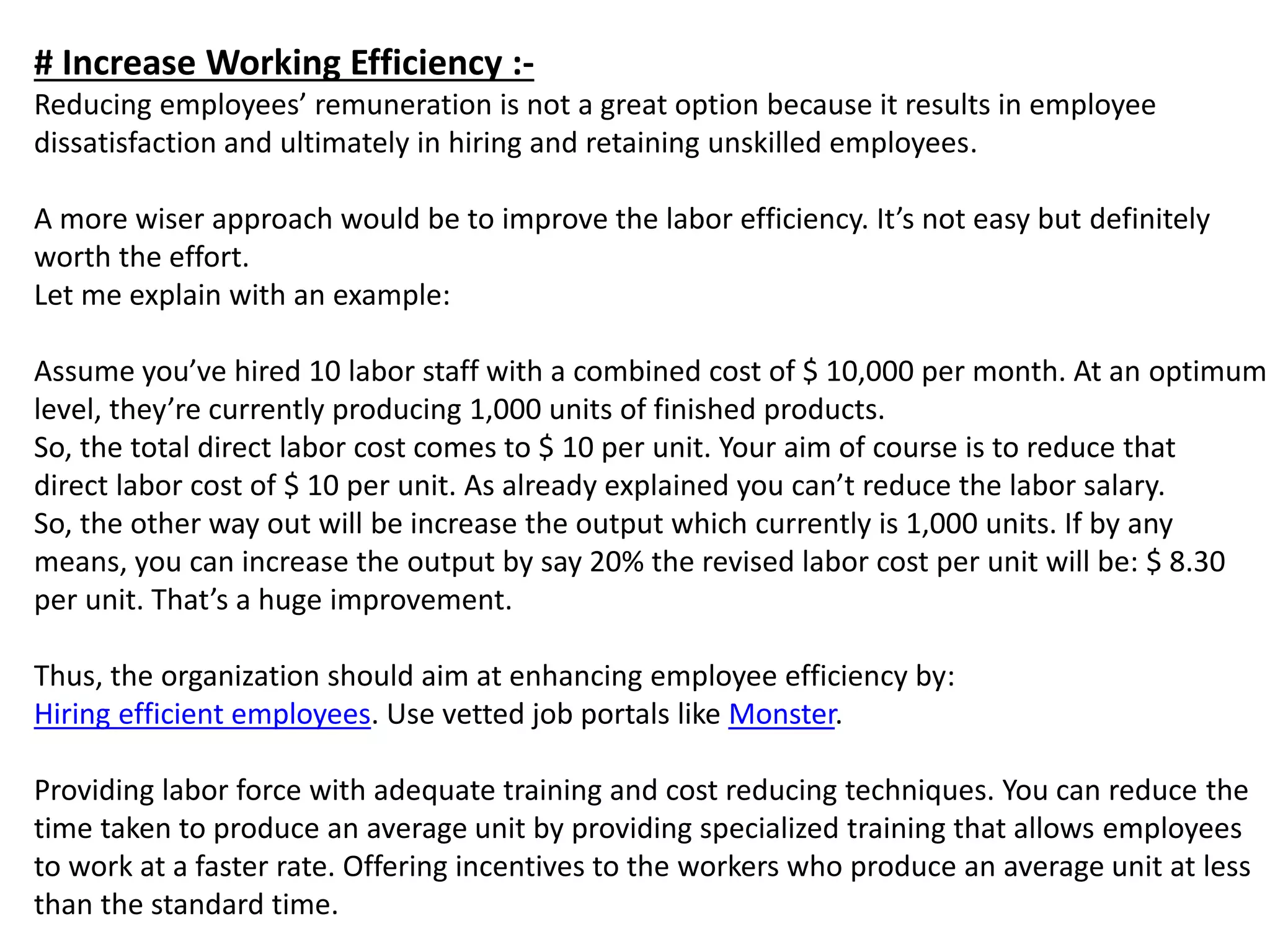

This document discusses ways to reduce production costs in a manufacturing business. It begins by defining manufacturing and production costs, which include direct material costs, direct labor costs, and manufacturing overheads. It then provides examples of calculating production costs and provides several techniques to reduce costs, including tracking production metrics, reducing direct material and inventory carrying costs, improving workforce efficiency, controlling overheads, eliminating non-value-adding processes, leveraging automation, optimizing production levels, reducing waste, and implementing control systems. The key recommendations are to track costs closely, negotiate lower material prices, optimize inventory levels, and control overhead spending.