Downloaded 28 times

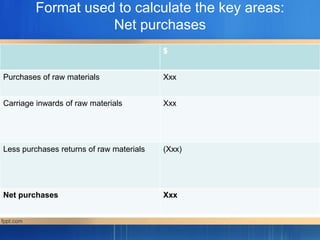

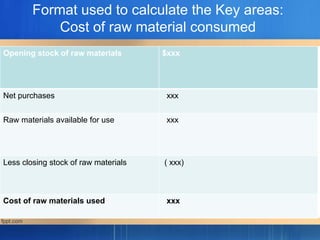

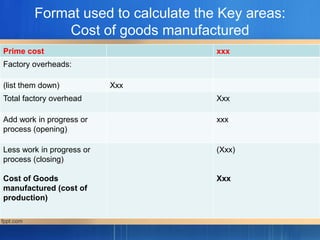

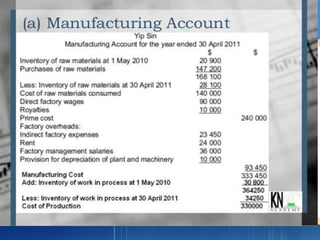

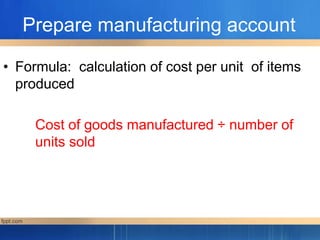

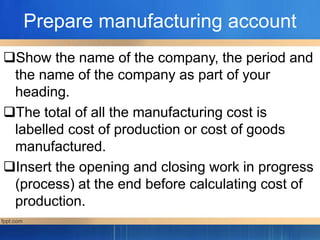

The document discusses preparing manufacturing accounts to calculate the unit cost of items produced. It provides: 1) A manufacturing account calculates the cost of producing completed goods by tracking raw material costs, direct wages, factory overheads and work-in-progress. 2) Key areas of the manufacturing process like raw material consumption, prime costs, factory overheads and cost of goods manufactured are calculated. 3) The complete manufacturing account format should show these key areas and the unit cost of production is calculated by dividing total cost of goods manufactured by the number of units sold.