Cost determination

• Itinvolves calculating the cost of resource

inputs like materials, labor, and overhead,

which is essential for pricing, profit

assessment, and cost control.

3.

2.1 Materials

Accounting forstock (inventory) cost movements

❑Commonly Used Classifications of Manufacturing Costs

● Three terms commonly used when describing manufacturing costs

are direct material costs, direct manufacturing labor costs, and

indirect manufacturing costs.

1. Direct material costs are the acquisition costs of all materials that

eventually become part of the cost object (work in process and then

finished goods) and can be traced to the cost object in an

economically feasible way.

● Acquisition costs of direct materials include purchase price, freight in

charges, sales taxes, and custom duties etc.

4.

Cont.

2. Direct manufacturinglabor costs include the compensation of

all manufacturing labor that can be traced to the cost object (work

in process and then finished goods) in an economically feasible

way. Examples include wage or salary paid to machine operators

and assembly-line workers who convert direct materials purchased

to finished goods.

3.Indirect manufacturing costs are all manufacturing costs

that are related to the cost object (work in process and then

finished goods) but cannot be traced to that cost object in an

economically feasible way.

5.

Cont.

Examples includesupplies, indirect

materials such as lubricants, indirect

manufacturing labor such as plant

maintenance and cleaning labor, plant

rent, plant insurance, property taxes on the

plant, plant depreciation, and the

compensation plant managers.

This cost category is also referred

to asmanufacturing overhead costs

or factory overhead costs.

6.

The Flow ofInventoriable Costs and Period Costs

● Manufacturing-Sector Example- To illustrate the flow of

inventoriable costs and period costs through the balance

sheet and income statement of a manufacturing company,

the cost data for ABC manufacturing company is taken.

● Inventorable costs go through the balance sheet accounts of

work-in-process inventory and finished goods inventory before

entering cost of goods sold in the income statement.

● Period costs are expensed directly in the income statement

7.

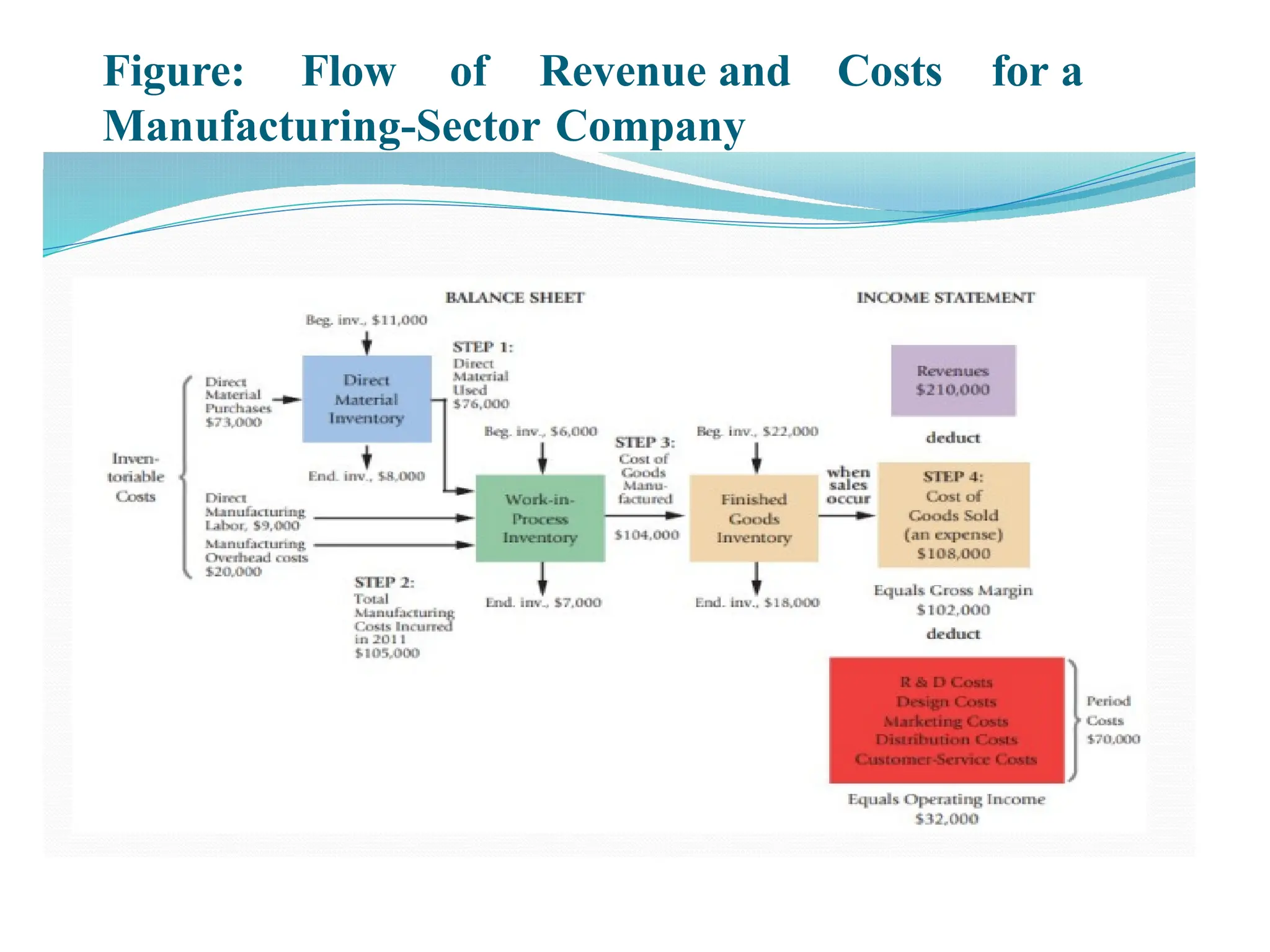

Figure: Flow ofRevenue and Costs for a

Manufacturing-Sector Company

8.

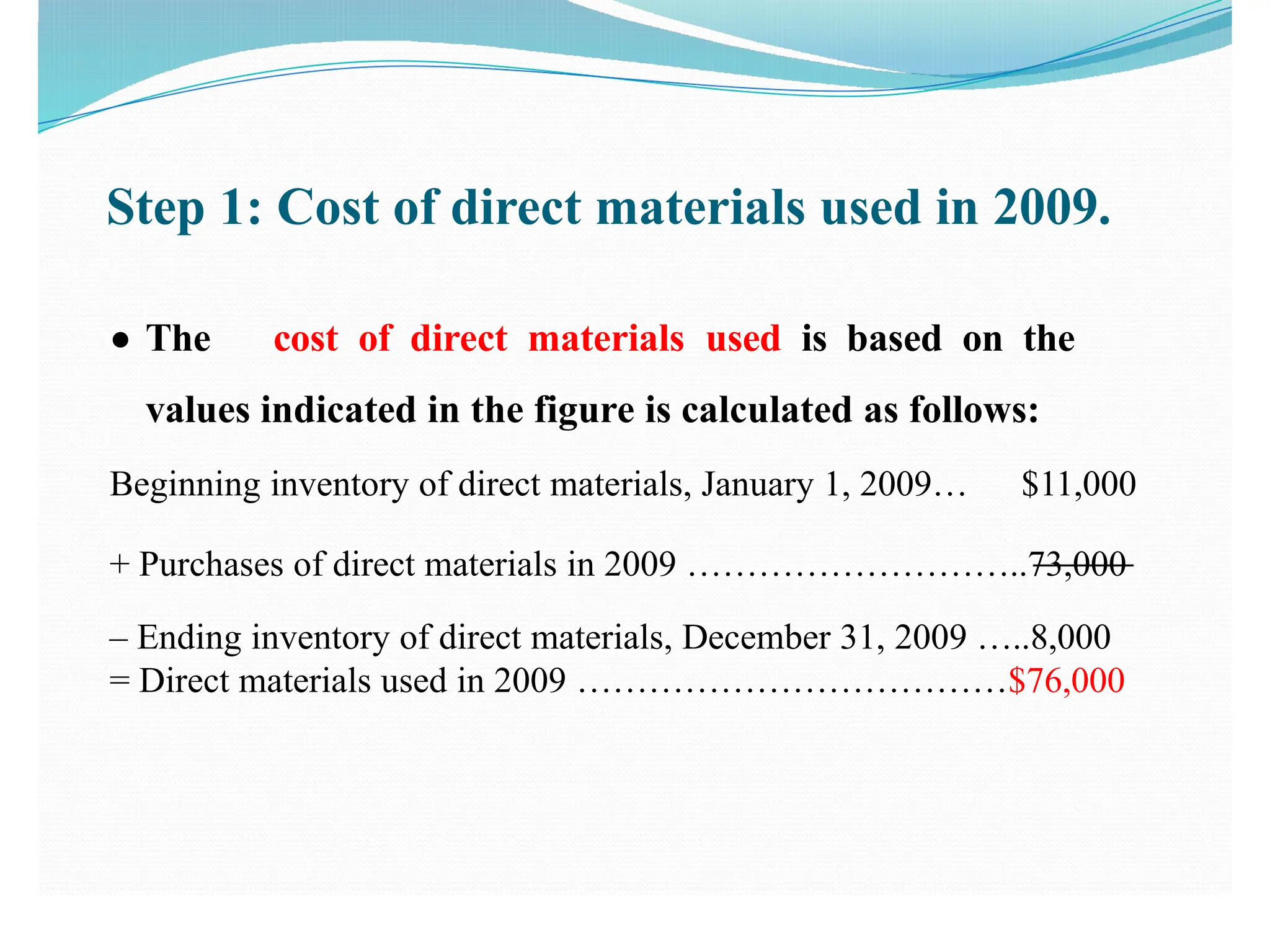

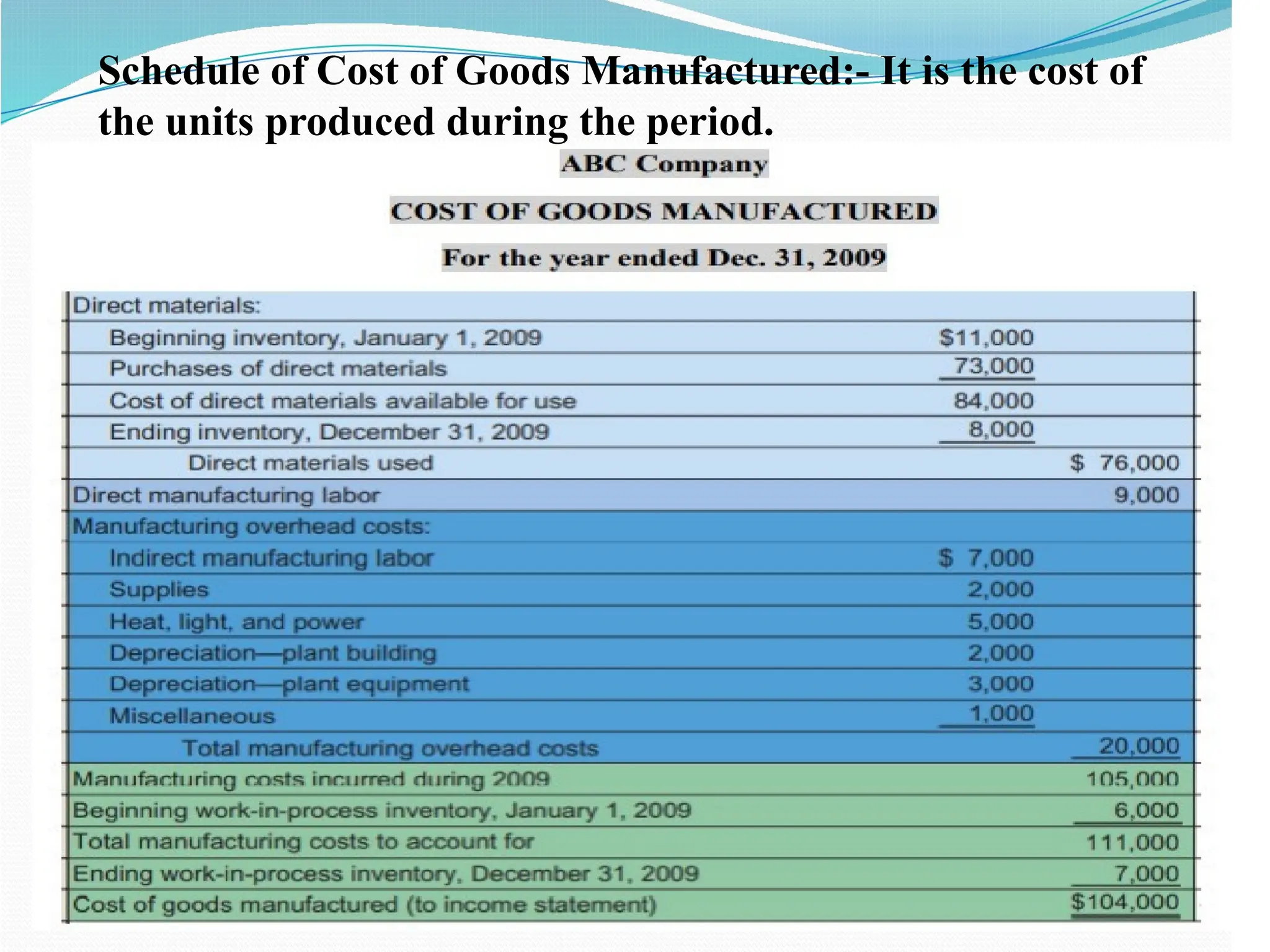

Step 1: Costof direct materials used in 2009.

● The cost of direct materials used is based on the

values indicated in the figure is calculated as follows:

Beginning inventory of direct materials, January 1, 2009… $11,000

+ Purchases of direct materials in 2009 ………………………..73,000

– Ending inventory of direct materials, December 31, 2009 …..8,000

= Direct materials used in 2009 ………………………………$76,000

9.

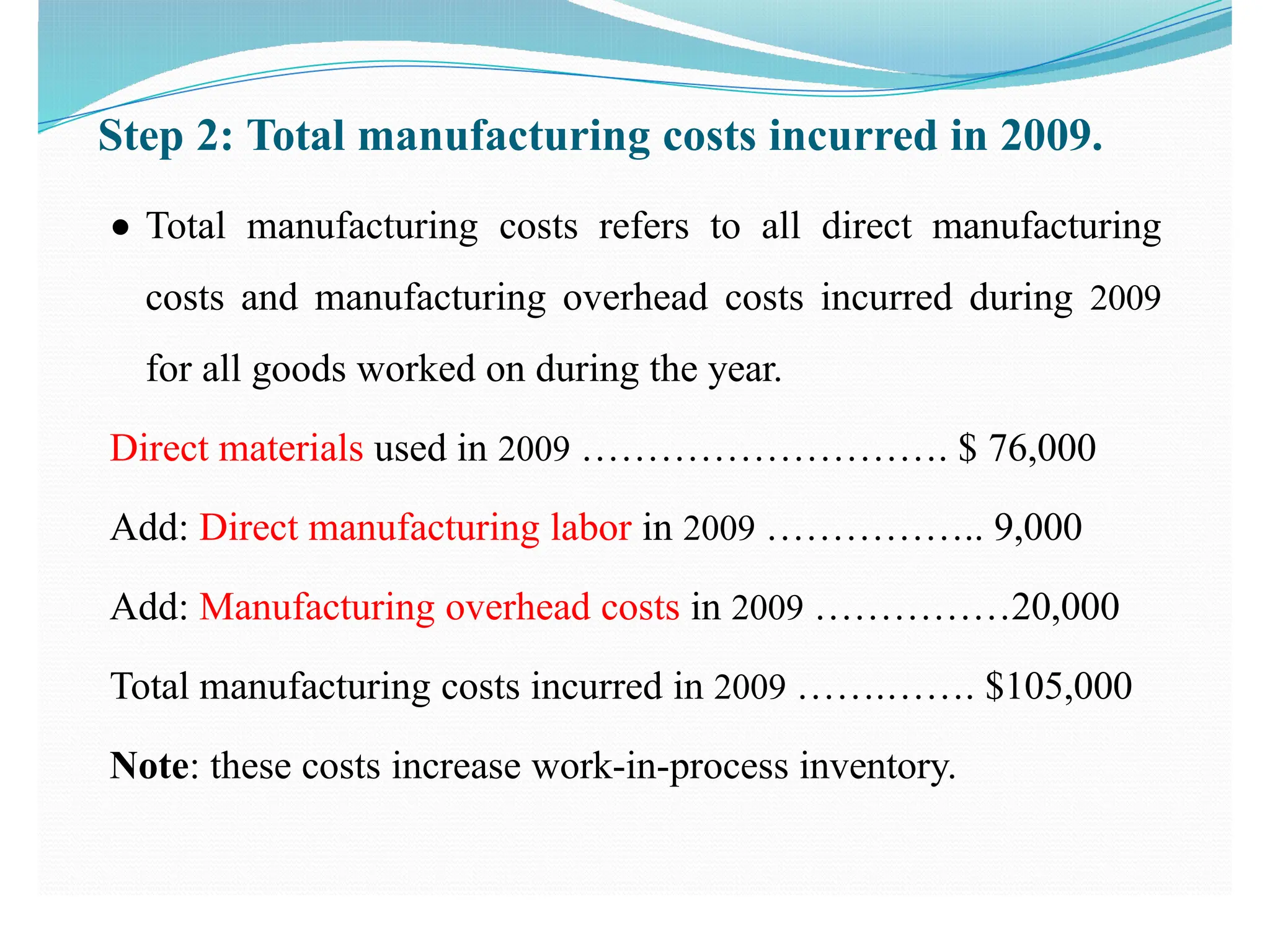

Step 2: Totalmanufacturing costs incurred in 2009.

● Total manufacturing costs refers to all direct manufacturing

costs and manufacturing overhead costs incurred during 2009

for all goods worked on during the year.

Direct materials used in 2009 ………………………. $ 76,000

Add: Direct manufacturing labor in 2009 …………….. 9,000

Add: Manufacturing overhead costs in 2009 ……………20,000

Total manufacturing costs incurred in 2009 …….……. $105,000

Note: these costs increase work-in-process inventory.

10.

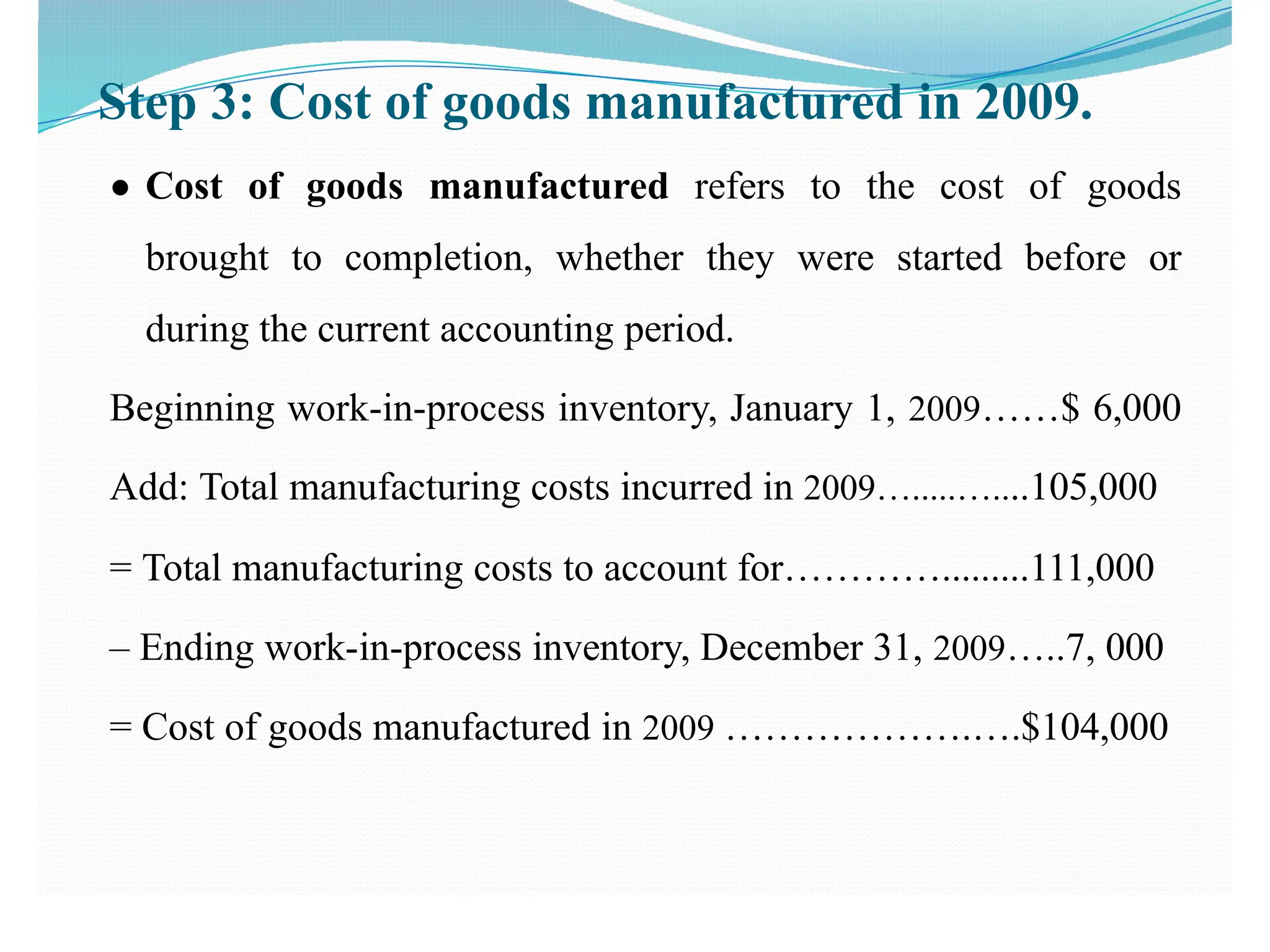

Step 3: Costof goods manufactured in 2009.

● Cost of goods manufactured refers to the cost of goods

brought to completion, whether they were started before or

during the current accounting period.

Beginning work-in-process inventory, January 1, 2009……$ 6,000

Add: Total manufacturing costs incurred in 2009….....…....105,000

= Total manufacturing costs to account for………….........111,000

– Ending work-in-process inventory, December 31, 2009…..7, 000

= Cost of goods manufactured in 2009 ……………….….$104,000

11.

Schedule of Costof Goods Manufactured:- It is the cost of

the units produced during the period.

12.

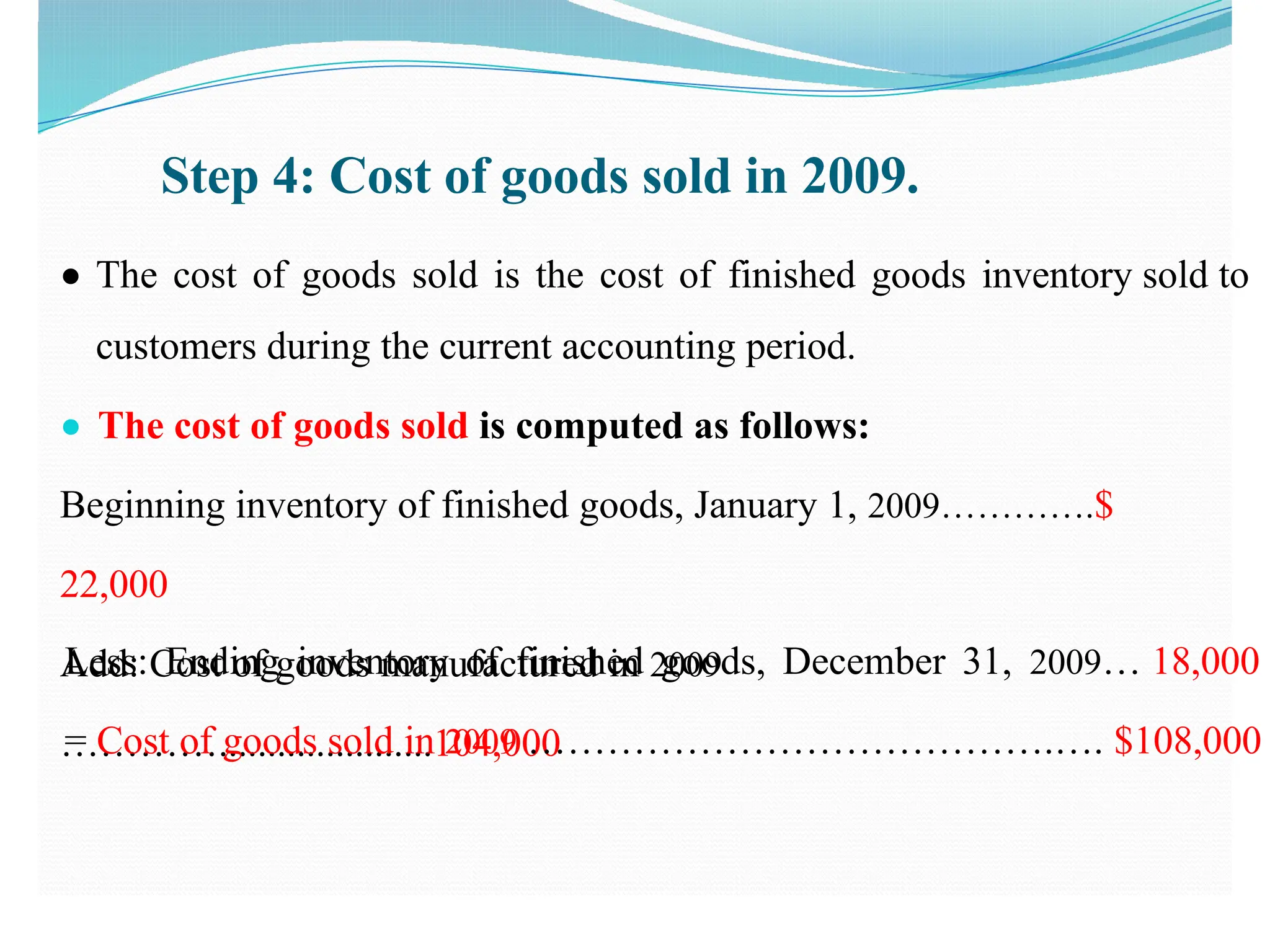

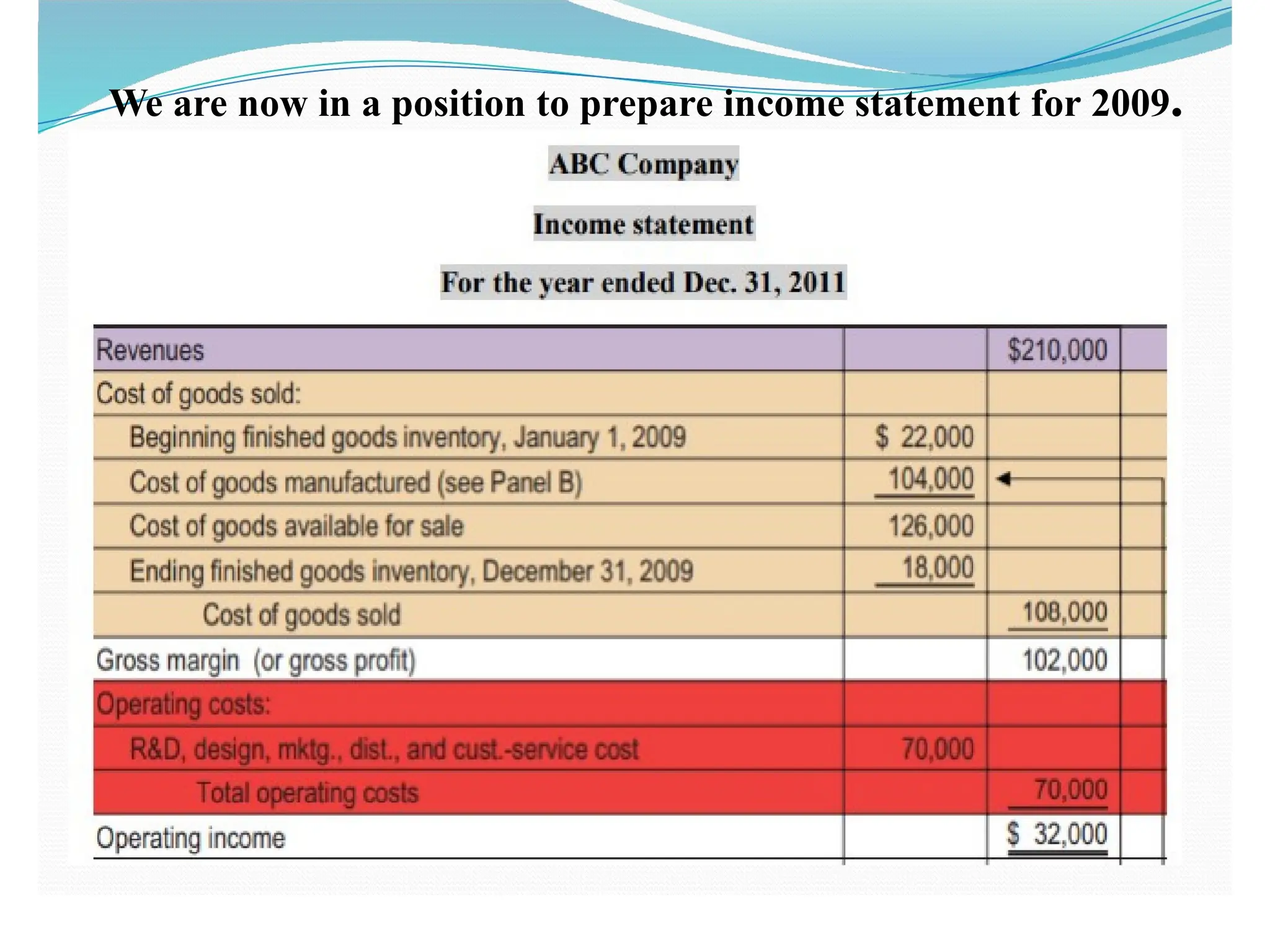

Step 4: Costof goods sold in 2009.

● The cost of goods sold is the cost of finished goods inventory sold to

customers during the current accounting period.

● The cost of goods sold is computed as follows:

Beginning inventory of finished goods, January 1, 2009………….$

22,000

Add: Cost of goods manufactured in 2009

…………......................104,000

Less: Ending inventory of finished goods, December 31, 2009… 18,000

= Cost of goods sold in 2009 ………………………………….…. $108,000

13.

We are nowin a position to prepare income statement for 2009.

14.

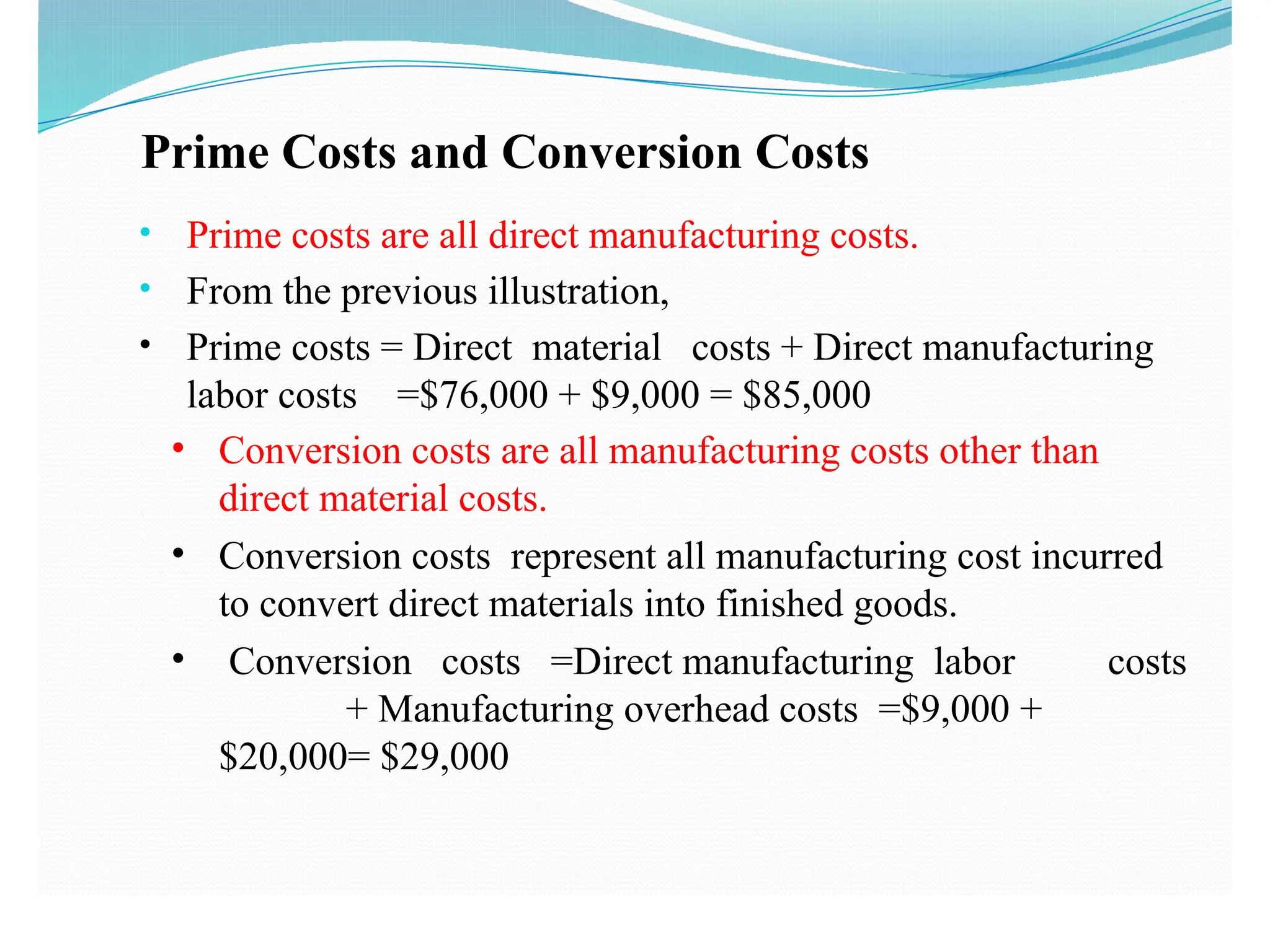

Prime Costs andConversion Costs

• Prime costs are all direct manufacturing costs.

• From the previous illustration,

• Prime costs = Direct material costs + Direct manufacturing

labor costs =$76,000 + $9,000 = $85,000

• Conversion costs are all manufacturing costs other than

direct material costs.

• Conversion costs represent all manufacturing cost incurred

to convert direct materials into finished goods.

• Conversion costs =Direct manufacturing labor costs

+ Manufacturing overhead costs =$9,000 +

$20,000= $29,000

15.

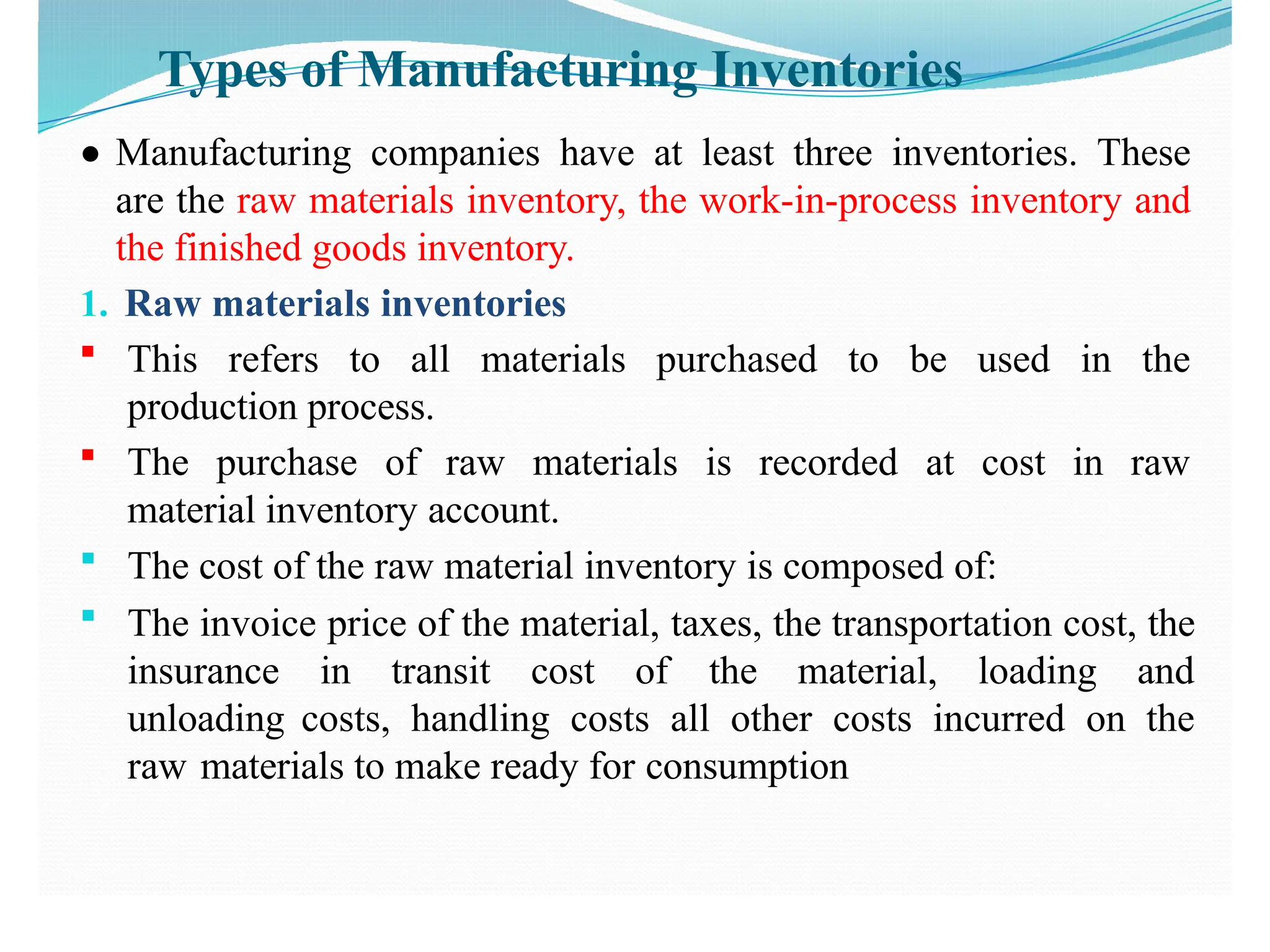

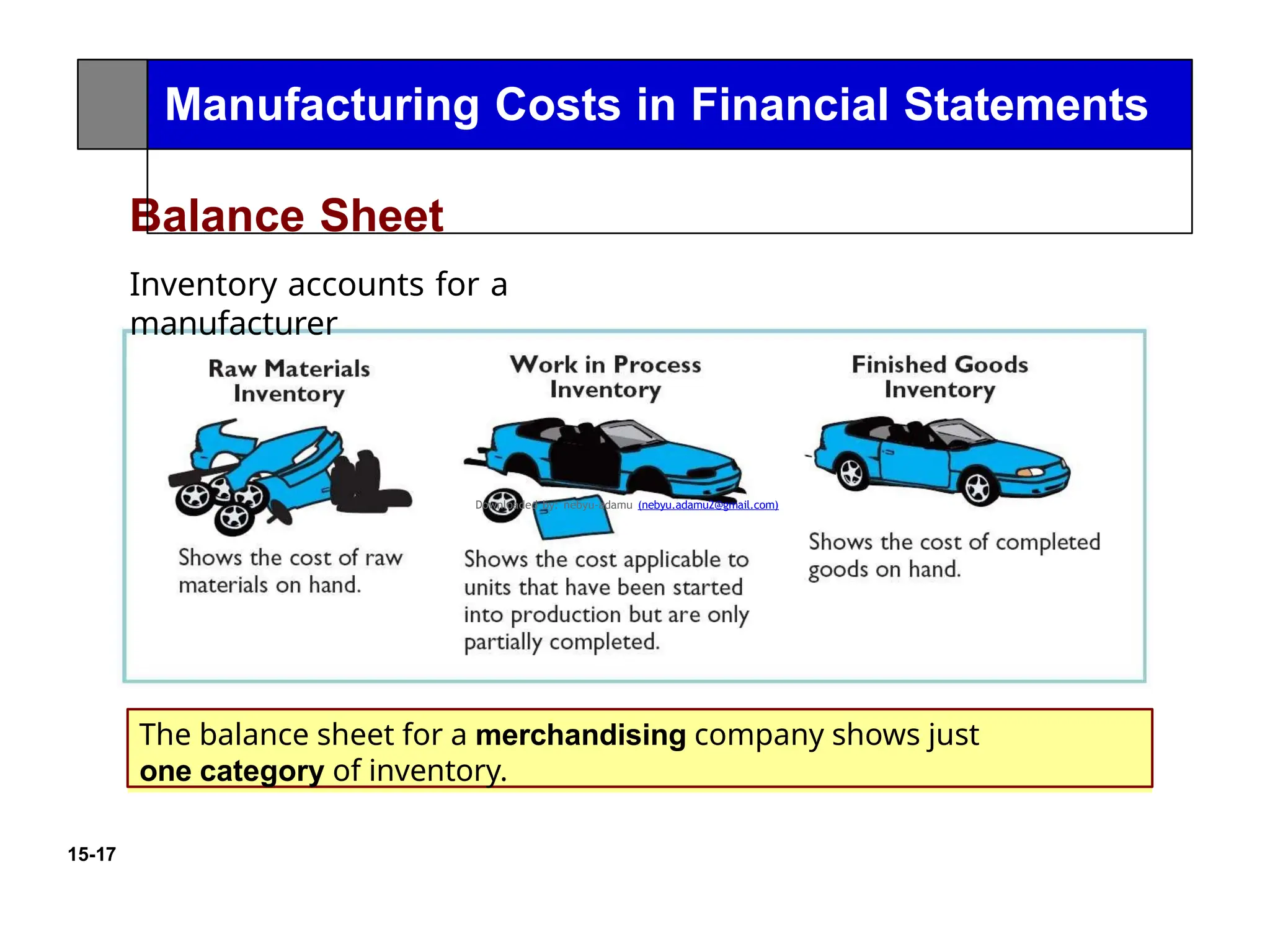

Types of ManufacturingInventories

● Manufacturing companies have at least three inventories. These

are the raw materials inventory, the work-in-process inventory and

the finished goods inventory.

1. Raw materials inventories

This refers to all materials purchased to be used in the

production process.

The purchase of raw materials is recorded at cost in raw

material inventory account.

The cost of the raw material inventory is composed of:

The invoice price of the material, taxes, the transportation cost, the

insurance in transit cost of the material, loading and

unloading costs, handling costs all other costs incurred on the

raw materials to make ready for consumption

16.

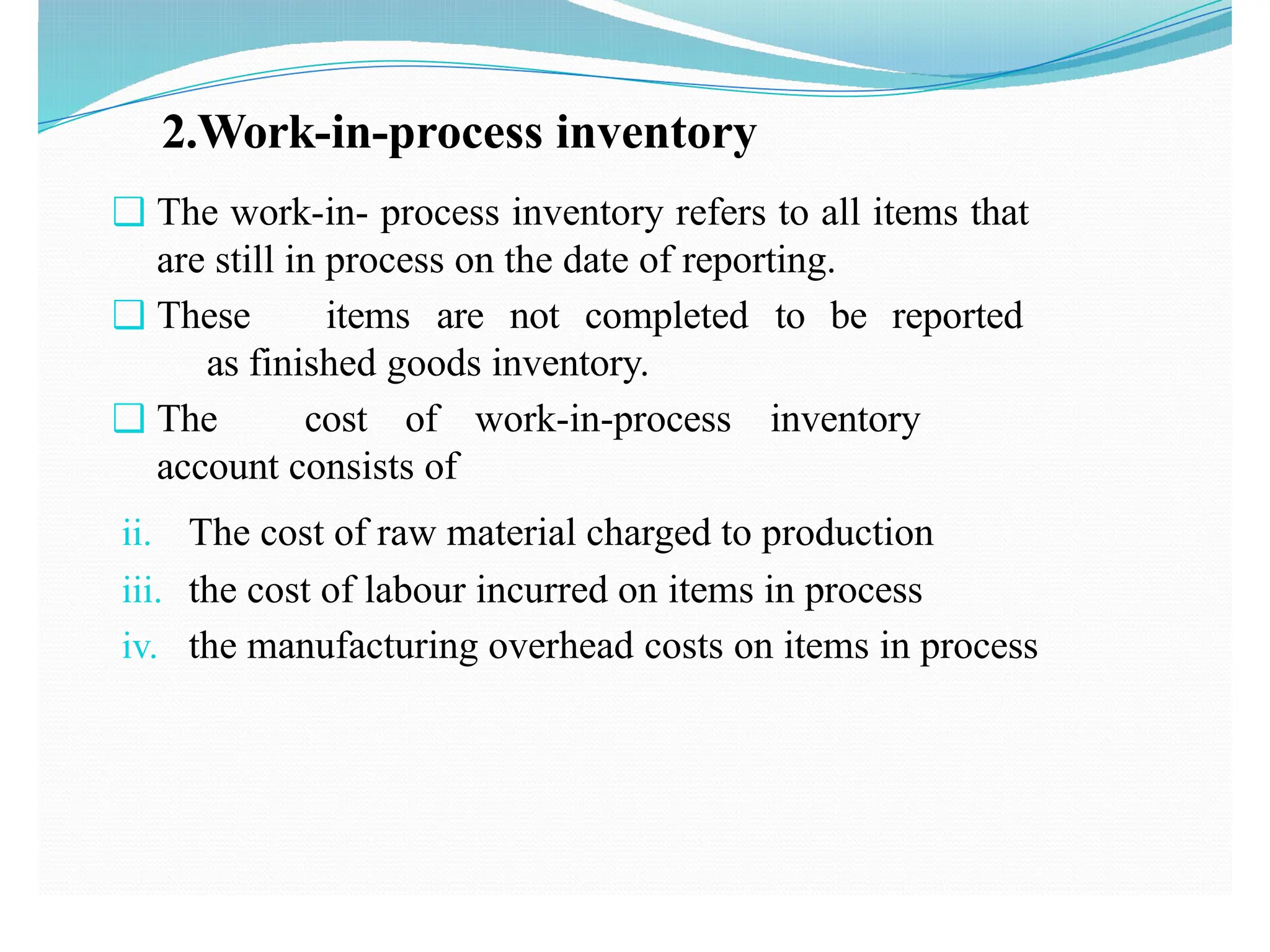

2.Work-in-process inventory

❑ Thework-in- process inventory refers to all items that

are still in process on the date of reporting.

❑ These items are not completed to be reported

as finished goods inventory.

❑ The cost of work-in-process inventory

account consists of

ii. The cost of raw material charged to production

iii. the cost of labour incurred on items in process

iv. the manufacturing overhead costs on items in process

17.

3. Finished goods

inventory

●The finished goods inventory account is used to record

cost of fully completed goods but not yet sold to

customers.

The cost of finished goods inventory is composed of:-

i. applicable cost of raw materials

ii. applicable cost of labour

iii. applicable cost of manufacturing overheads

● Note that these costs are the total required costs

to complete the production process.

18.

15-17

Balance Sheet

Inventory accountsfor a

manufacturer

The balance sheet for a merchandising company shows just

one category of inventory.

Manufacturing Costs in Financial Statements

Downloaded by: nebyu-adamu (nebyu.adamu2@gmail.com)

19.

1.Accounting for materials

●As you know manufacturing process involves conversion of

raw materials in to completed finished goods.

● Accounting for materials is, therefore, critical to determine the

proper cost of a product.

● There are two major group of materials used in manufacturing

process, the direct materials and indirect materials.

● Accounting for materials involves making entries for the

purchase of raw materials, the return of defective materials to

the suppliers and the issuance of raw materials in to production.

20.

Purchasing raw materials

A purchase requisition is a form that records a

request for materials to be purchased.

This form must indicate at least the following

information:-

• Product description and quantity

• The purpose that the material is purchased,

• Price

• Name of the supplier etc.

21.

Cont.

● Once thesupplier is selected, the next stage is to prepare the purchase

order.

● A purchase order is a business form that records items requested from

the supplier.

● The purchase order must indicate at least the following

important

information.

● The type of material to be purchased.

● The full address of the supplier.

● The purchase requisition number.

● Delivery date and term of purchase.

● Price and quantity of the material to be purchased.

22.

Cont.

● The followingjournal entries will be made when raw materials are

purchased.

● To record the purchase of materials for cash:

Raw materials inventory…………………xx

Cash………………………..…………………….xx

● To record purchase of materials on account:

Raw materials inventory ………………………..XX

Account payable …………………………………………..XX

23.

Issuing materials toproduction

• When materials are taken from the stock room and issued to the production process, the

raw materials are divided into two categories, direct and indirect.

• Direct materials are those that become an identifiable part of the manufactured

product where as, indirect materials are needed in the production process, but not an

identifiable part of the finished product.

• Although both direct and indirect materials are grouped together as raw materials when

they are purchased.

• They are classified separately when they are issued to production.

• Direct materials issued to production are recorded in the work- in-process inventory

account.

• Indirect materials issued to production are recorded initially in the factory over head

control account.

24.

Cont.

● The journalentries to record the issuance of raw materials to production

and return of defective materials to the seller are out lined as

follows:-

● To record issuance of raw materials to production:

Work in process inventory (direct)………..……….XX

Factory overhead account (indirect)…………….….XX

Raw material inventory………………………….

…XX

● to record detective materials returned to the

seller by receiving

credit

Accounting payable…..……………….XX

Raw Materials inventory ……………….XX

● to record defective materials returned to the seller by receiving cash

Cash…………..……………………………XX

Raw materials inventory ……………….XX

25.

Material Control

● Materialcontrol is a system which ensures that right quality of

material is available in the right quantity at the right time and

right place with the right amount of investment.

● The two basic aspects of materials control are (1) the physical

control or safeguarding of materials and (2) control over

the investment in materials.

● Physical control protects materials from misuse or

misappropriation. Controlling the investment in materials

maintains

i. Limited access:-Only authorized personnel should have

access to materials storage areas.

ii. Segregation of duties:-the following functions should be segregated:

purchasing, receiving, storage, use, and recording.

iii. Accuracy in recording:-accurate recording of the purchase

and issuance of materials.

appropriate quantities of materials in inventory.

❑Physical Control of Materials

26.

Cont.

❑Controlling the Investmentin Materials:-An inventory of sufficient

size and variety for efficient operations must be maintained, but

the size should not be excessive in relation to scheduled

production needs.

❑To determine the quantity to be ordered, the cost of placing an order

(order costs) and the cost of carrying inventory in stock (carrying

costs) must be considered.

• To decide how much to order, you need to account for the ordering

costs and the inventory holding costs.

● Effective materials planning and control involve analyzing these factors

to decide:

i. When to place orders, and

ii. How many units to order.

27.

Accounting for StockLosses

• At some point, you're going to lose inventory due to

theft, damage or obsolescence.

• When this happens, the inventory loss should be recorded

a company's accounting book.

• To record the loss of inventory:

Loss on inventory……….………………xx

Inventory……………………………….xx

28.

1.Accounting for Labour

•In a manufacturing process, the raw materials are

converted into completed finished goods using labour and

manufacturing overheads.

• Accounting for labour is therefore, critical to determine

the proper cost of a product

• Labour cost is part of the cost of producing products of

an organization.

• It is necessary to know the amount or the cost of the labour

time spent on each product to determine the cost of a product.

29.

Cont.

• Documentation, calculationsand analysis of labour

costs are necessary for the following three main

reasons.

ii.

iii. For management accounting and inventory

valuations we need to allocate the labour cost of the

period to the products produced.

i. To calculate the correct gross pay and net pay for each

employee

For financial accountingpurposes

30.

Cont.

●There are differenttypes of documents used to identify labor

cost. The common ones are presented below.

●Clock cards:- is a document on

which the starting and finishing times of an employee

are recorded to ascertain total

actual attendance.

●Job card: - is a record of time spent on a job/product. it will

usually show the cost of labour hour incurred on a job/product

●A timesheet:- is a method for

recording the amount of a worker's time

spent on each job/product.

31.

Method Of RemunerationOf Workers

● The following methods are in use for the remuneration of workers:

i. Fixed salary

ii. Time rate or day rate:-This is a method of calculating wages based

on the hours of works put at work by each worker. Workers paid

according to the effective hours worked.

iii. Piece rate or piece Work. This is the method of remunerating workers

based on the number of work or piece of work done. This method

does not consider the time spent on the work.

iv. Differential piece work:-Taylor’s Differential Piece-Rate System

was introduced by F.W. Taylor, who believed that the workers should

be paid on the basis of their degree of efficiencies.

Remuneration of workers refers to the total compensation or payment

that employees receive in exchange for their work.

32.

Cont.

• Accounting forlabour in a cost accounting system

involves two procedures, recording the payroll and charging

the labour costs to production.

• To record a factory payroll, we debiting an account

called payroll account.

it is

• To charge labour costs to the production

process, necessary to determine the direct and indirect

labour costs.

33.

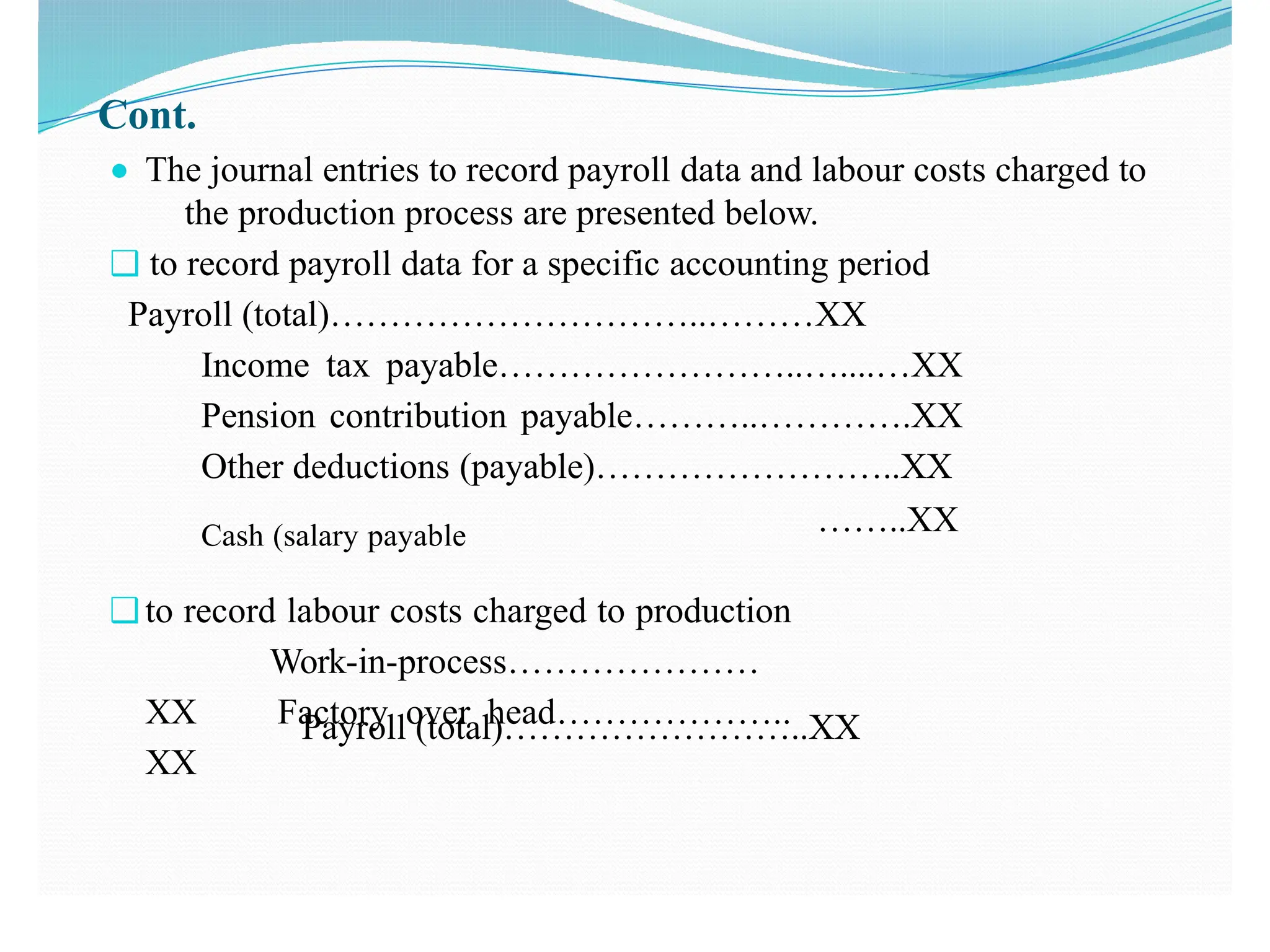

Cont.

● The journalentries to record payroll data and labour costs charged to

the production process are presented below.

❑ to record payroll data for a specific accounting period

Payroll (total)…………………………..………XX

Income tax payable……………………..…....…XX

Pension contribution payable………..………….XX

Other deductions (payable)……………………..XX

……..XX

Payroll (total)……………………..XX

Cash (salary payable

❑ to record labour costs charged to production

Work-in-process…………………

XX Factory over head………………..

XX

34.

Accounting for manufacturingoverheads costs

● Manufacting overhead costs are all manufacturing costs other than direct

material and direct labour costs. It includes indirect materials, indirect

labour costs and other costs attributable to production process such as

factory rent, utilities (power, heat, light, water etc.), supplies, property taxes

factory insurance, depreciation of factory machineries/ building and other

factory facilities etc.

● Manufacturing over head cost is one of the three manufacturing

cost elements.

● Accounting for manufacturing over head costs is, therefore, equally critical

to determine the proper cost of a product as it is for materials and labour.

35.

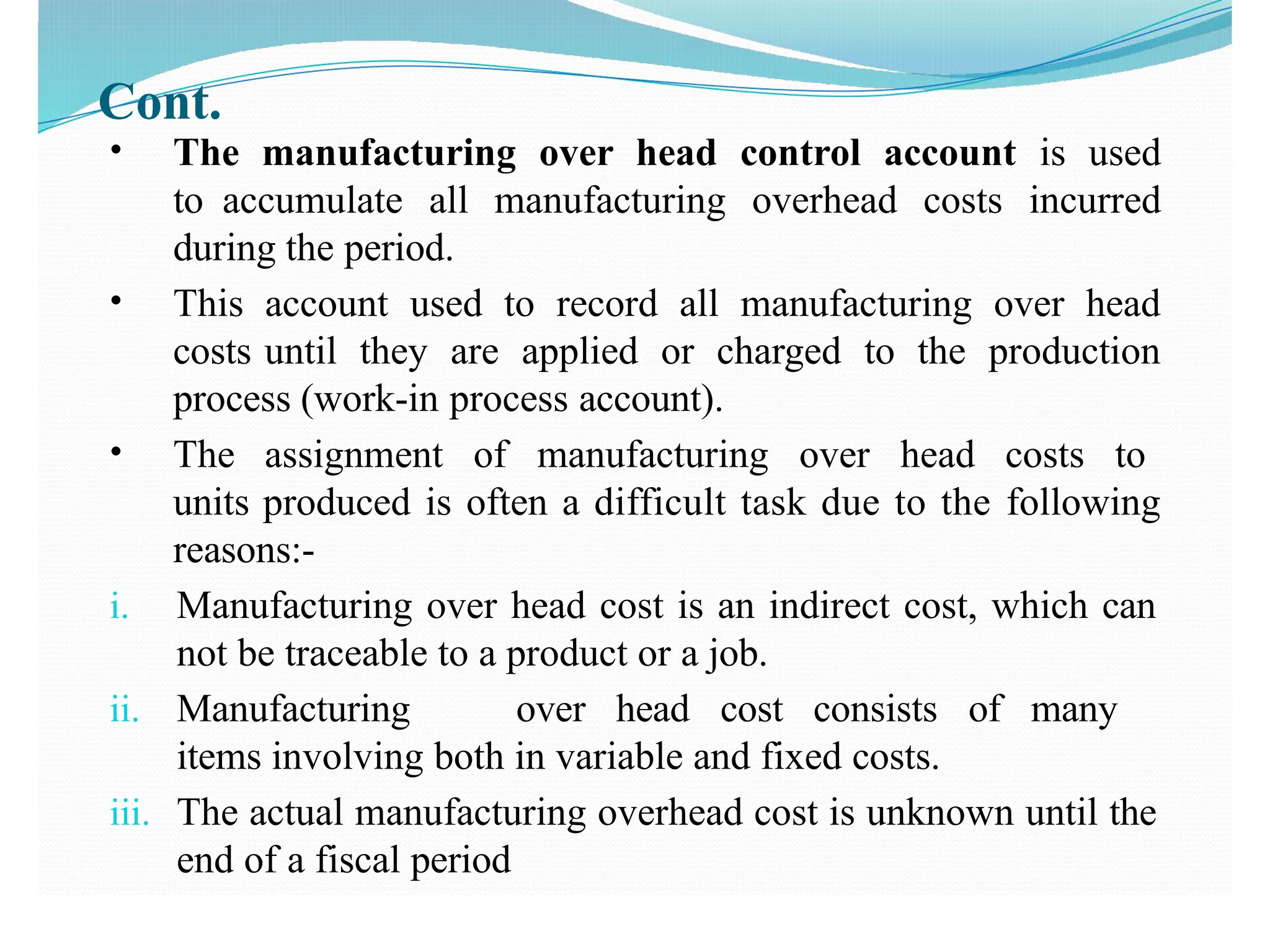

Cont.

• The manufacturingover head control account is used

to accumulate all manufacturing overhead costs incurred

during the period.

• This account used to record all manufacturing over head

costs until they are applied or charged to the production

process (work-in process account).

• The assignment of manufacturing over head costs to

units produced is often a difficult task due to the following

reasons:-

i. Manufacturing over head cost is an indirect cost, which can

not be traceable to a product or a job.

ii. Manufacturing over head cost consists of many

items involving both in variable and fixed costs.

iii. The actual manufacturing overhead cost is unknown until the

end of a fiscal period

36.

15-35

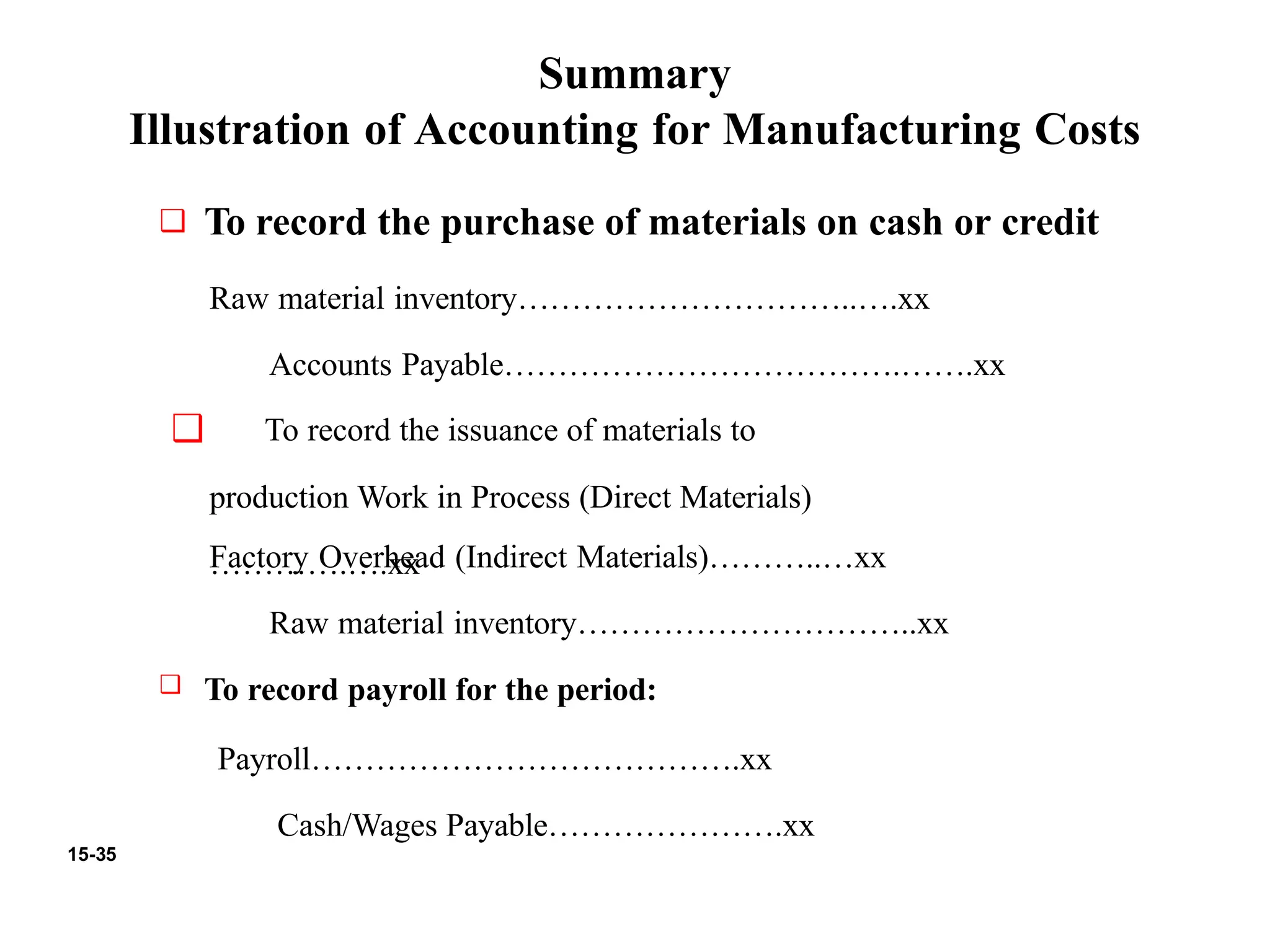

Summary

Illustration of Accountingfor Manufacturing Costs

❑ To record the purchase of materials on cash or credit

Raw material inventory…………………………..….xx

Accounts Payable……………………………….…….xx

❑ To record the issuance of materials to

production Work in Process (Direct Materials)

………….….xx

Factory Overhead (Indirect Materials)………..…xx

Raw material inventory…………………………..xx

❑ To record payroll for the period:

Payroll………………………………….xx

Cash/Wages Payable………………….xx

37.

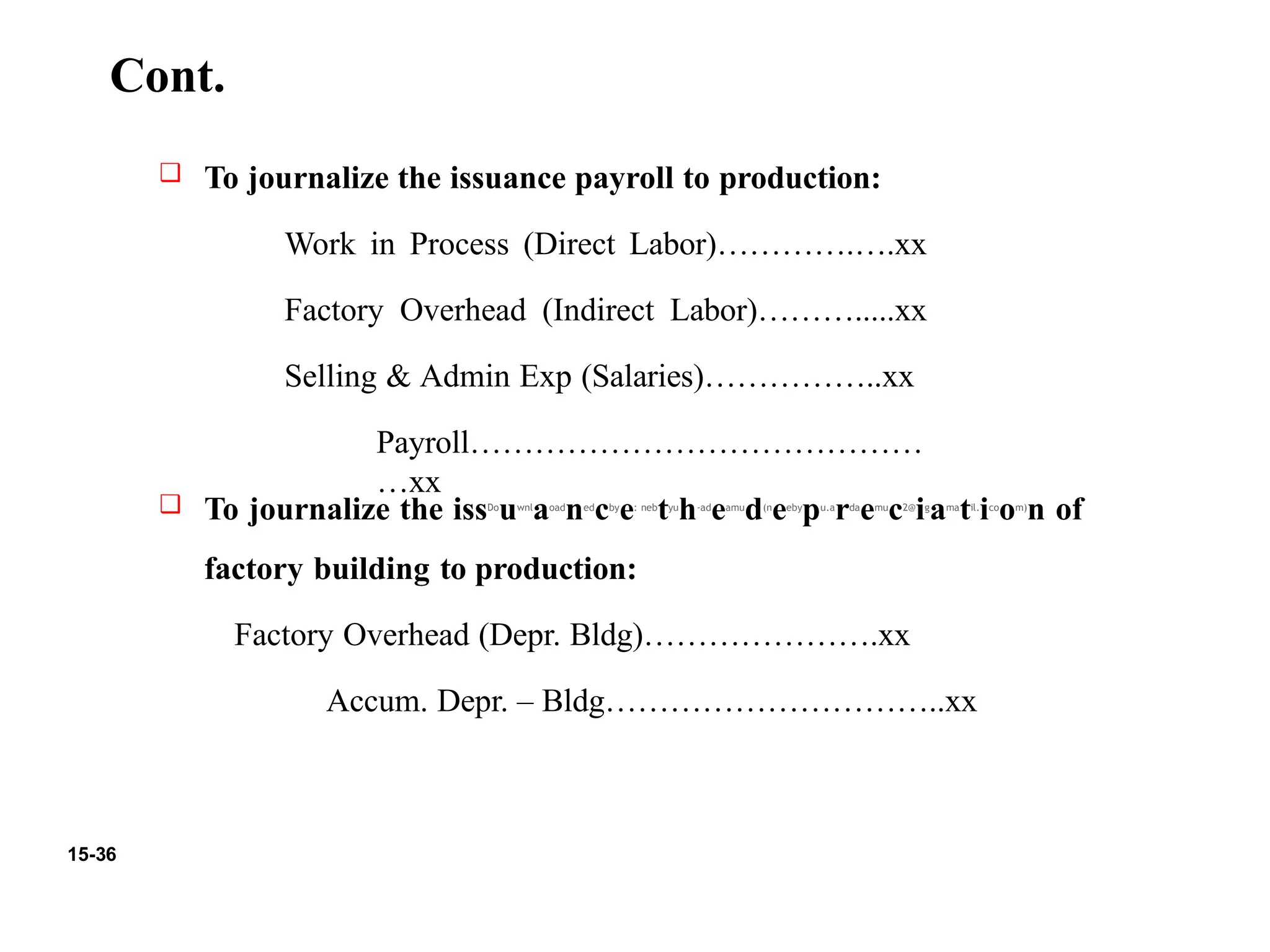

15-36

Cont.

To journalize theissDo

uwnl

aoad

ned

cby

e: neb

tyu

h-ad

eamu

d(n

eeby

pu.a

rda

emu

c2@

ig

ama

til.

ico

om)

n of

factory building to production:

Factory Overhead (Depr. Bldg)………………….xx

Accum. Depr. – Bldg…………………………..xx

❑ To journalize the issuance payroll to production:

Work in Process (Direct Labor)………….….xx

Factory Overhead (Indirect Labor)……….....xx

Selling & Admin Exp (Salaries)……………..xx

Payroll……………………………………

…xx

❑

38.

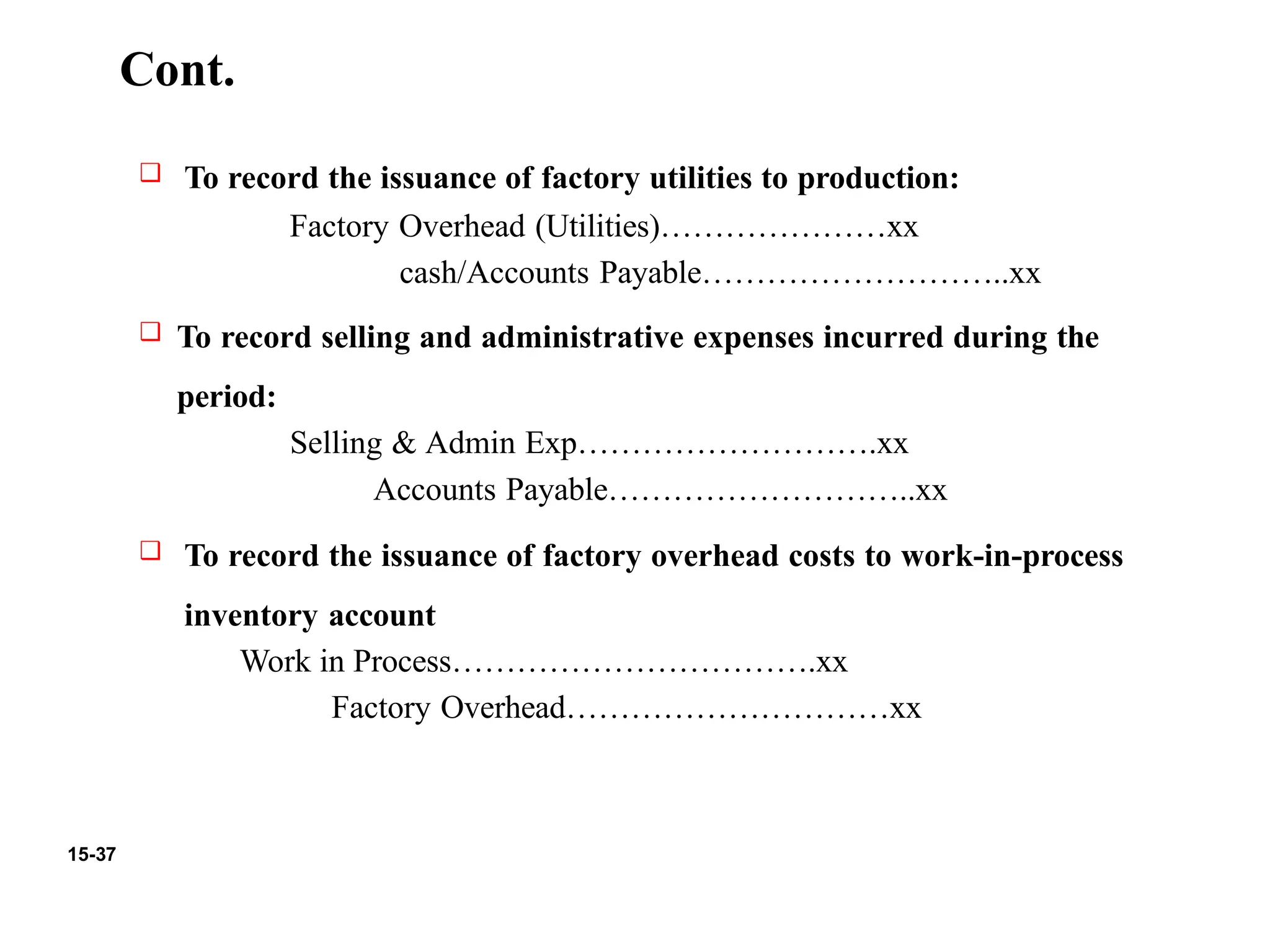

15-37

Cont.

❑ To recordthe issuance of factory utilities to production:

Factory Overhead (Utilities)…………………xx

cash/Accounts Payable………………………..xx

❑ To record selling and administrative expenses incurred during the

period:

Selling & Admin Exp……………………….xx

Accounts Payable………………………..xx

❑ To record the issuance of factory overhead costs to work-in-process

inventory account

Work in Process…………………………….xx

Factory Overhead…………………………xx

39.

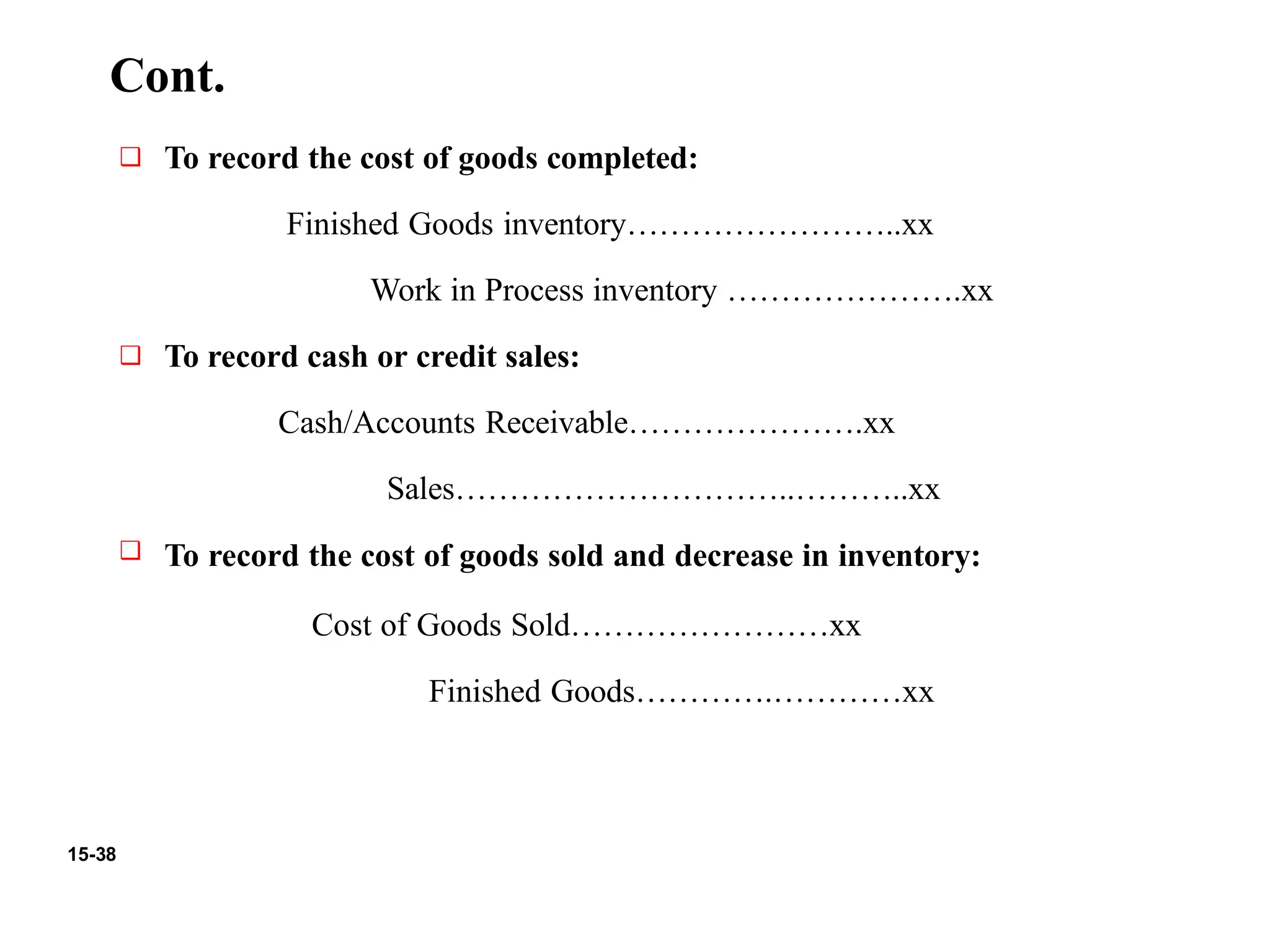

15-38

Cont.

❑ To recordthe cost of goods completed:

Finished Goods inventory……………………..xx

Work in Process inventory ………………….xx

❑ To record cash or credit sales:

Cash/Accounts Receivable………………….xx

Sales…………………………..………..xx

❑ To record the cost of goods sold and decrease in inventory:

Cost of Goods Sold……………………xx

Finished Goods………….…………xx