Download to read offline

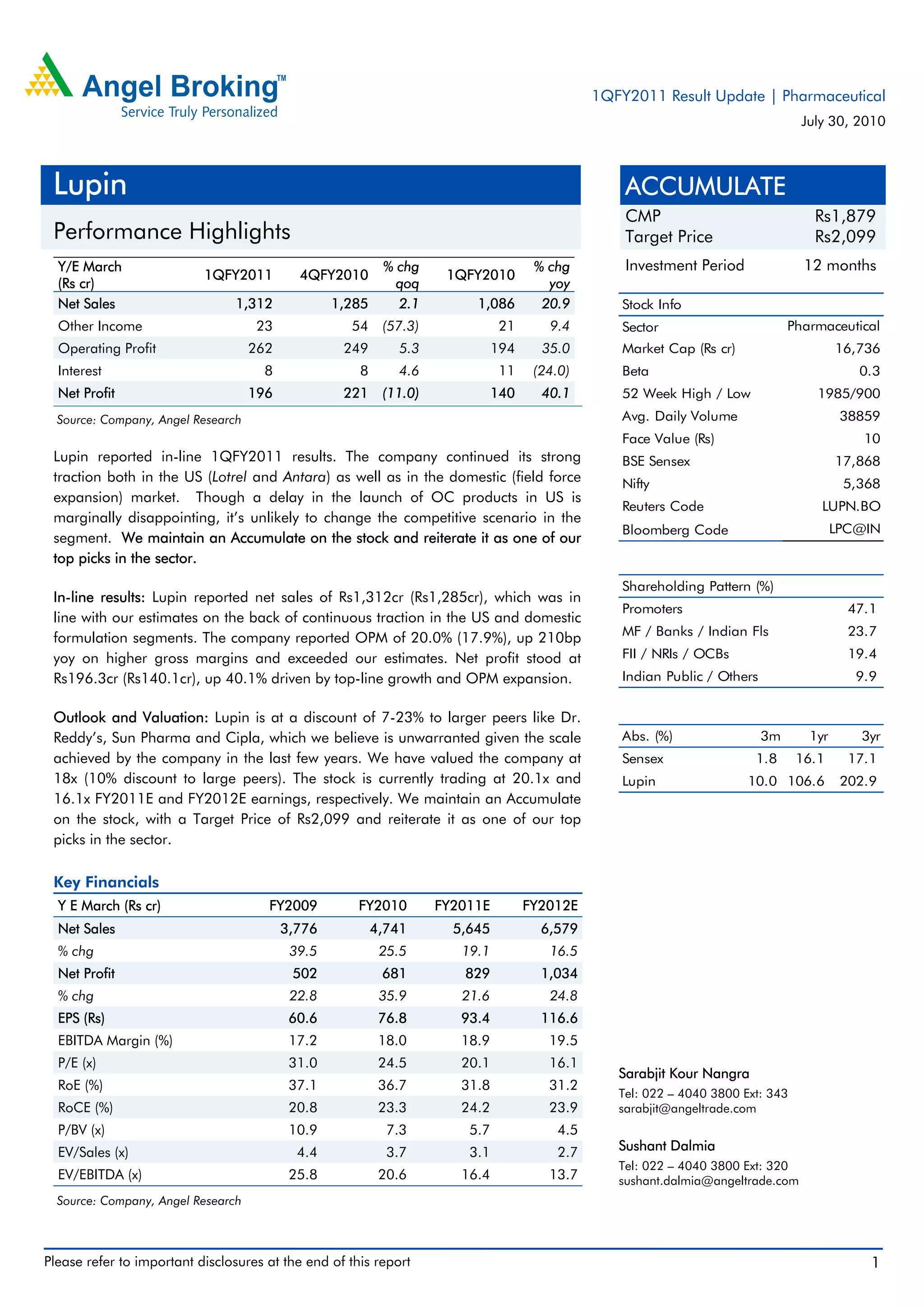

Lupin reported in-line results for the first quarter of fiscal year 2011, with net sales of Rs1,312 crore, operating profit margin of 20%, and net profit of Rs196 crore. Key drivers of growth included strong sales of generic drugs in the US market, as well as expansion of Lupin's domestic field force in India. While the company saw a delay in FDA approval for oral contraceptive drugs, management does not expect this to impact its competitive position. The analyst maintains an 'Accumulate' rating for Lupin based on its scale in key markets like the US and India, as well as its pipeline of generic drug approvals.