Larsen & Tourbo

•

1 like•163 views

Larsen & Toubro (L&T) reported modest results for the first quarter of fiscal year 2011 that were below analyst expectations on revenue but positively surprised on margins. Revenue grew 6.4% year-over-year to Rs. 7,885 crore, below estimates, due to flat performance in the engineering and construction segment. However, operating margins expanded significantly by 170 basis points due to lower subcontracting costs. The order backlog remained strong at Rs. 1,07,816 crore as of June 30, 2010 and order inflows were led by the power segment. While most positives are priced into the stock, further upside could come from value unlocking at subsidiary levels.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Larsen & Tourbo

Similar to Larsen & Tourbo (20)

More from Angel Broking

More from Angel Broking (20)

Recently uploaded

Recently uploaded (20)

Larsen & Tourbo

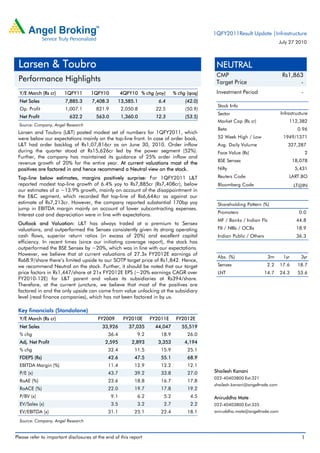

- 1. 1QFY2011Result Update |Infrastructure July 27 2010 Larsen & Toubro NEUTRAL CMP Rs1,863 Performance Highlights Target Price - Y/E March (Rs cr) 1QFY11 1QFY10 4QFY10 % chg (yoy) % chg (qoq) Investment Period - Net Sales 7,885.3 7,408.3 13,585.1 6.4 (42.0) Stock Info Op. Profit 1,007.1 821.9 2,050.8 22.5 (50.9) Sector Infrastructure Net Profit 632.2 563.0 1,360.0 12.3 (53.5) Market Cap (Rs cr) 112,382 Source: Company, Angel Research Beta 0.96 Larsen and Toubro (L&T) posted modest set of numbers for 1QFY2011, which were below our expectations mainly on the top-line front. In case of order book, 52 Week High / Low 1949/1371 L&T had order backlog of Rs1,07,816cr as on June 30, 2010. Order inflow Avg. Daily Volume 327,287 during the quarter stood at Rs15,626cr led by the power segment (52%). Face Value (Rs) 2 Further, the company has maintained its guidance of 25% order inflow and BSE Sensex 18,078 revenue growth of 20% for the entire year. At current valuations most of the positives are factored in and hence recommend a Neutral view on the stock. Nifty 5,431 Top-line below estimates, margins positively surprise: For 1QFY2011 L&T Reuters Code LART.BO reported modest top-line growth of 6.4% yoy to Rs7,885cr (Rs7,408cr), below Bloomberg Code LT@IN our estimates of a ~13.9% growth, mainly on account of the disappointment in the E&C segment, which recorded flat top-line of Rs6,644cr as against our estimate of Rs7,213cr. However, the company reported substantial 170bp yoy Shareholding Pattern (%) jump in EBITDA margin mainly on account of lower subcontracting expenses. Promoters 0.0 Interest cost and depreciation were in line with expectations. MF / Banks / Indian Fls 44.8 Outlook and Valuation: L&T has always traded at a premium to Sensex valuations, and outperformed the Sensex consistently given its strong operating FII / NRIs / OCBs 18.9 cash flows, superior return ratios (in excess of 20%) and excellent capital Indian Public / Others 36.3 efficiency. In recent times (since our initiating coverage report), the stock has outperformed the BSE Sensex by ~20%, which was in line with our expectations. However, we believe that at current valuations of 27.3x FY2012E earnings of Abs. (%) 3m 1yr 3yr Rs68.9/share there’s limited upside to our SOTP target price of Rs1,842. Hence, we recommend Neutral on the stock. Further, it should be noted that our target Sensex 2.2 17.6 18.7 price factors in Rs1,447/share at 21x FY2012E EPS (~20% earnings CAGR over LNT 14.7 24.3 53.6 FY2010-12E) for L&T parent and values its subsidiaries at Rs394/share. Therefore, at the current juncture, we believe that most of the positives are factored in and the only upside can come from value unlocking at the subsidiary level (read finance companies), which has not been factored in by us. Key financials (Standalone) Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E Net Sales 33,926 37,035 44,047 55,519 % chg 36.4 9.2 18.9 26.0 Adj. Net Profit 2,595 2,893 3,353 4,194 % chg 32.4 11.5 15.9 25.1 FDEPS (Rs) 42.6 47.5 55.1 68.9 EBITDA Margin (%) 11.4 12.9 12.2 12.1 P/E (x) 43.7 39.2 33.8 27.0 Shailesh Kanani 022-40403800 Ext:321 RoAE (%) 23.6 18.8 16.7 17.8 shailesh.kanani@angeltrade.com RoACE (%) 22.0 19.7 17.8 19.2 P/BV (x) 9.1 6.2 5.2 4.5 Aniruddha Mate EV/Sales (x) 3.5 3.2 2.7 2.2 022-40403800 Ext:335 EV/EBITDA (x) 31.1 25.1 22.4 18.1 aniruddha.mate@angeltrade.com Source: Company, Angel Research Please refer to important disclosures at the end of this report 1

- 2. 1QFY2011 Result Update | Larsen & Toubro Exhibit 1: Quarterly Performance (Standalone) Y/E March (Rs cr) 1QFY11 1QFY10 4QFY10 % chg (yoy) % chg (qoq) FY10 FY09 % chg Net Sales 7885 7408 13585 6.4 (42.0) 37035 33926 9.2 Total Expenditure 6878 6586 11534 4.4 (40.4) 32295 30094 7.3 Operating Profit 1007.1 821.9 2050.8 22.5 (50.9) 4739.4 3832.4 23.7 OPM (%) 12.8 11.1 15.1 - - 12.8 11.3 - Interest 142.3 109.6 135.6 29.9 5.0 505.3 350.2 44.3 Depreciation 114.2 83.7 116.2 36.3 (1.8) 379.7 282.8 34.2 Non Operating Income 176.8 211.8 329.8 (16.5) (46.4) 768.2 642.9 19.5 Extraordinary/Dividend from Subs 50.0 1030.9 122.3 (95.1) (59.1) 1393.8 870.6 - Profit Before tax 977.3 1871.2 2251.1 (47.8) (56.6) 6016.4 4712.9 27.7 Tax 311.1 273.0 813.0 13.9 (61.7) 1640.9 1231.2 33.3 Reported Net Profit 666.3 1598.2 1438.1 (58.3) (53.7) 4375.5 3481.7 25.7 PAT (%) 8.4 21.6 10.6 - - 11.8 10.3 - Reported EPS 95.4 27.3 23.9 249.6 299.0 73.8 59.5 24.0 Adjusted Profit After Tax 632.2 563.0 1360.0 12.3 (53.5) 2892.9 2595.2 11.5 Adj. PAT (%) 8.0 7.6 10.0 - - 7.8 7.6 - Adj. FDEPS 10.4 9.3 22.3 12.3 (53.5) 47.5 42.6 11.5 Source: Company, Angel Research Exhibit 2: Segmental Performance Y/E March (Rs cr) 1QFY11 1QFY10 4QFY10 % chg (yoy) % chg (qoq) Revenues 7,963 7,476 13,700 Engg & Const. 6,644 6,573 12,109 1.1 (45.1) Mach. & Ind. Products 548 437 682 25.5 (19.6) Electrical & Electronics 745 576 988 29.4 (24.6) Others 122 77 100 58.3 21.5 Intersegment revenue 96 186 180 (48.5) (46.8) EBIT 1,032 858 2,100 Engg & Const. 816.7 699.2 1,846.6 16.8 (55.8) Mach. & Ind. Products 113.0 95.4 143.1 18.5 (21.0) Electrical & Electronics 73.8 68.0 132.9 8.4 (44.5) Others 33.5 4.2 2.0 697.4 1,541.7 Intersegment margins 5.2 8.6 24.3 (39.7) (78.7) Capital Employed 27,109 20,803 25,190 Engg & Const. 7,092 6,979 6,291 1.6 12.7 Mach. & Ind. Products 176 294 224 (40.1) (21.4) Electrical & Electronics 1,109 1,151 1,132 (3.7) (2.0) Others 203 215 203 (5.9) (0.4) Unallocable 18,530 12,163 17,340 52.3 6.9 Source: Company, Angel Research July 27 2010 2

- 3. 1QFY2011 Result Update | Larsen & Toubro Top-line below estimates, margins positively surprise: L&T reported modest top-line growth of 6.4% yoy to Rs7,885cr (Rs7,408cr), below our estimates of ~13.9% growth, mainly on account of the disappointment from the E&C segment, which recorded flat top-line of Rs6,644cr as against our estimate of Rs7,213cr. This was mainly on account of inflows being heavily back ended in FY2010, with 60% of orders coming in 2HFY2010 and 35% in 4QFY2010. However, 6.4% yoy sales growth is in line with the internal projections of the company and they are on track to achieve 20% growth for the year as a whole. The company ended 1QFY2011 with an order book at Rs1,07,816, up 51% yoy. The asking rate is 18.9% yoy (Rs71,339cr) in the remaining nine months of FY2011E to meet its order inflow guidance of 25%. Exhibit 3: Trend in revenues Exhibit 4: Trend in order booking 16000 50.0 35,000 160.0 14000 139.5 140.0 40.0 30,000 39.8 120.0 12000 35.0 25,000 100.0 28.1 30.0 10000 20,000 80.0 25.3 65.2 63.3 8000 20.0 60.0 15,000 47.5 40.0 6000 23.4 20.0 10.0 10,000 14.3 4000 7.3 6.4 - 3.0 5,000 (16.9) - (21.8) (20.0) 2000 (5.7) - (40.0) 0 (10.0) 2QFY093QFY094QFY091QFY102QFY103QFY104QFY101QFY11 2QFY093QFY094QFY091QFY102QFY103QFY104QFY101QFY11 Sales (Rs cr, LHS) Growth (yoy %, RHS) Order Booking (Rs cr, LHS) Growth (yoy %, RHS) Source: Company, Angel Research Source: Company, Angel Research However, the company reported a phenomenal 170bp yoy jump in EBITDA margin mainly on account of lower subcontracting expenses. Interest cost and depreciation were in line with expectations. Exhibit 5: Trend in EBITDA Exhibit 6: Trend in net profit 2,500.0 16.0 1600 12.0 15.0 15.1 12.3 14.0 1400 10.4 2,000.0 10.0 10.0 12.8 12.0 1200 8.8 8.0 11.2 7.6 8.0 1,500.0 10.6 10.0 1000 7.6 7.0 8.8 9.1 8.0 800 6.0 6.0 1,000.0 6.0 600 4.0 4.0 400 500.0 2.0 2.0 200 - - 0 - 2QFY093QFY094QFY091QFY102QFY103QFY104QFY101QFY11 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 EBITDA (Rs cr, LHS) EBITDAM (%, RHS) PAT (Rs cr, LHS) PATM (%, RHS) Source: Company, Angel Research Source: Company, Angel Research July 27 2010 3

- 4. 1QFY2011 Result Update | Larsen & Toubro Strong performance at subsidiary levels Technology subsidiary, L&T InfoTech reported an excellent performance following the recovery in the US and Europe markets. L&T InfoTech reported 19.2% yoy and 23.6% qoq growth in revenue for 1QFY2011. On the profitability front, the subsidiary reported an improvement, with NPM at 14.0%, indicating effective cost controls. The financial subsidiaries registered a revival in business, and witnessed yoy revenue growth of 44.9% in L&T Finance and 72.1% in L&T Infrastructure Finance for 1QFY2011. L&T Finance also saw an increase in its assets to Rs8,000cr (from Rs7,000cr in 4QFY2010), while L&T Infrastructure Finance increased its assets to Rs4,500cr (from Rs3,800cr in 4QFY2010). Exhibit 7: Subsidiary performance 1QFY11 1QFY10 4QFY10 % chg (yoy) % chg (qoq) Revenues L&T InfoTech 565.0 474.0 457.0 19.2 23.6 L&T Finance 287.0 198.0 300.0 44.9 (4.3) L&T Infra. Finance 148.0 86.0 134.0 72.1 10.4 PAT L&T InfoTech 79.0 61.0 90.0 29.5 (12.2) L&T Finance 58.0 24.0 52.0 141.7 11.5 L&T Infra. Finance 48.0 22.0 35.0 118.2 37.1 Asset base L&T Finance 8,000 5,000 7,000 60.0 14.3 L&T Infra. Finance 4,500 3,000 4,300 50.0 4.7 Source: Company, Angel Research Order Book Analysis L& T registered a robust order inflow of Rs15,626cr during 1QFY2011 mainly on account of the power segment, which contributed 52% of the overall order inflow. Orders to the tune of ~89% for the year came from the local market, taking the company’s outstanding order book to Rs1,07,816cr. L&T’s order book is majorly dominated by the power (33%) and infrastructure (32%) segments. Process (15%), hydrocarbon (14%) and others (6%) form the balance part of the order book. Exhibit 8: Quarterly sectoral order inflow trend (Rs cr) Exhibit 9: Quarterly sectoral OB composition trend (Rs cr) 12,000 120,000 10,000 100,000 8,000 80,000 6,000 60,000 4,000 40,000 2,000 20,000 - - 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 1QFY11 Process Hydrocarbon Power Infrastructure Others Process Hydrocarbon Power Infrastructure Others Source: Company, Angel Research Source: Company, Angel Research July 27 2010 4

- 5. 1QFY2011 Result Update | Larsen & Toubro Client-wise, 40% of the outstanding order book comes from the public sector, with 47% coming from the private sector, and the balance being captive work orders. Notably there has been a drop in the share of public sector, which management has cited as not a concern and guided to be revived in the ensuing quarters. Outlook and Valuation: Positives priced in at Rs1,863 The macro outlook for infrastructure in general, and the consequent benefits for L&T in terms of order inflows in particular, remain strong. We believe that the company will continue to occupy a unique position in the Indian engineering and construction space as a diversified, large engineering play, with exposure to areas ranging from power to defence to nuclear to equipment. Further, in light of higher margins in the quarter and management guidance, we are marginally tweaking our numbers to factor in the same. Exhibit 10: 1QFY2011 Actual v/s Estimates Estimates Actual Variation % Net Sales 8,437 7,885 (6.5) OPM (%) 10.7 12.8 207.1bp PAT 592 632 6.8 Source: Company, Angel Research Exhibit 11: Change in estimates FY2011E FY2012E Earlier Estimates Revised Estimates Variation % Earlier Estimates Revised Estimates Variation % Revenues 44,156 44,047 (0.3) 55,744 55,519 (0.4) EBITDA Margins 12.0 12.2 22bp 12.0 12.1 17bp PAT 3,306 3,353 1.4 4,155 4,194 0.9 Source: Company, Angel Research At the CMP of Rs1,863, the stock is trading at 27.0x FY2012E earnings and 4.5x FY2012E P/BV, on a standalone basis. We have used the sum-of-the-parts (SOTP) methodology to value the company to capture all its business initiatives and investments/stakes in the different businesses. On SOTP basis, by ascribing separate values to its parent business on a P/E basis and investments in subsidiaries using the P/E, P/BV and MCap basis, we have arrived at a fair value of Rs1,842 for L&T, which provides limited upside from current levels. Hence, we recommend Neutral on the stock. Further, it should be noted that at our SOTP Target Price, the stock would trade at 27.0x FY2012E standalone EPS of Rs68.9, which would imply a premium of ~60% over Angel’s Sensex Target FY2012E P/E multiple of 17x. This is at a nominal discount to the historical premium commanded by L&T over the Sensex. July 27 2010 5

- 6. 1QFY2011 Result Update | Larsen & Toubro Exhibit 12: L &T - Parent historic P/E multiple premium to BSE Sensex Source: Company, Angel Research The historical 1-year forward P/E band shows that L&T has traded at an average P/E of 24.9x, 28.1x and 30.5x over the past seven, five and three year, respectively. Therefore, our SOTP target price at implied P/E multiple of 27.0x on standalone basis is again at a nominal discount to its historical average. It should be noted here that we believe the discount would remain given: 1) structural change in order book with exposure to higher gestation orders; 2) investments in future ventures – resulting in dilution of return ratios in the medium term, and 3) the earnings growth enjoyed by the company in the past would not be the same going ahead. Exhibit 13: L&T - Parent 1-year forward P/E bands 70.0 60.0 50.0 40.0 30.0 20.0 10.0 0.0 25-Mar-04 25-Mar-05 25-Mar-06 25-Mar-07 25-Mar-08 25-Mar-09 25-Mar-10 25-Nov-03 25-Nov-04 25-Nov-05 25-Nov-06 25-Nov-07 25-Nov-08 25-Nov-09 25-Jul-03 25-Jul-04 25-Jul-05 25-Jul-06 25-Jul-07 25-Jul-08 25-Jul-09 25-Jul-10 P/E 7YEAR AVG 5YEAR AVG 3YEAR AVG Source: Company, Angel Research July 27 2010 6

- 7. 1QFY2011 Result Update | Larsen & Toubro Exhibit 14: SOTP Target price Business Segment Methodology (x) Remarks Rs cr Rs/share % to TP L&T- Parent P/E 21x FY2012E earnings 88,068 1,447 78.6 Infrastructure Subsidiaries 8,063 132 7.2 IDPL (stake - 78.4%) P/BV 2.5x FY2012E Book value 8,063 132 7.2 Key Subsidiaries - Services 8,193 135 7.3 L&T Infotech P/E 14x FY2012E Earnings 4,971 82 4.4 L&T Finance P/BV 1.5x FY2012E Book value 2,016 33 1.8 L&T Infrastructure Finance P/BV 1.5x FY2012E Book value 1,206 20 1.1 Key Subsidiaries - Manufacturing 5,204 86 4.6 Tractor Engineers P/E 12x FY2012E Earnings 242 4 0.2 Associate Companies P/E 12x FY2012E Earnings 1,540 25 1.4 L&T MHI Boilers and Turbines (stake - 51%) P/E 16x FY2012E Earnings 3,422 56 3.1 Other Subsidiaries 2,536 42 2.3 Satyam 6.1% stake Mcap 20% holding company discount 375 6 0.3 Other Investments P/BV 1x FY2012E Book Value 2,161 36 1.9 Total 112,063 1,842 100 Source: Company, Angel Research Exhibit 15: Key Assumptions FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E Order Inflow 30,600 42,020 51,600 69,572 83,104 96,716 Revenues 17,605 24,878 33,926 37,035 44,047 55,519 Order Backlog (Y/E) 36,900 52,680 70,300 100,239 139,487 179,663 OB/Sales (x) 2.1 2.1 2.1 2.7 3.2 3.2 Source: Company, Angel Research Exhibit 16: Angel EPS forecast v/s Consensus Angel Forecast Bloomberg Consensus Variation % FY2011E 55.1 61.6 11.8 FY2012E 68.9 76.4 10.9 Source: Company, Angel Research July 27 2010 7

- 8. 1QFY2011 Result Update | Larsen & Toubro Investment Arguments Proxy to India's infra story: We believe that L&T is in an enviable position, given the apparent shortage of good quality constructors in India. It is in a position to choose its contracts and negotiate for price variation clauses. L&T's strong balance sheet, a sound execution engine, wide array of capabilities, integrated operations tailored to suit India's infrastructure growth story and multiple, recurring value-unlocking triggers over the medium term, lead us to place faith in this default India infrastructure story. Further, L&T has an order book of >Rs1trillon, lending revenue visibility. With signs of pick up in execution, management has guided for an improving scenario and we also believe that most of the pieces are falling into place for the company. Well-capitalised balance sheet funding the expansion: L&T has a well-capitalised balance sheet, at a debt-equity ratio of 0.3x as of FY2010, in spite of having a strong portfolio of assets and having invested in future growth areas. We believe that the key factors for the same are: 1) high margins, and 2) better working capital management. Great Infusion-Dilution opportunity: Investment in the construction segment is expected to double over the Eleventh Plan period, and the PPP model is assuming greater significance in delivering and meeting physical targets in the different segments of the Infrastructure space. The government, through Regulatory changes, is focusing on the construction segment through the PPP mode of investment. It expects the PPP share in the Eleventh Plan to be 30%, as against a mere 19.8% in the Tenth Plan. This has become imperative due to the widening gap between the demand for infrastructure and financial resources available with the government to fund the same. Given the high growth opportunities present in L&T's varied business verticals (Infrastructure and Finance), we feel that the company provides a great infusion-dilution opportunity. It should be noted that such moves lead to short-term dilution in equity, leading to the EPS getting temporarily depressed. However, such moves also shore up the net worth of the company, which fuels its future growth. Further, it also serves as a benchmark for valuing the entity. July 27 2010 8

- 9. 1QFY2011 Result Update | Larsen & Toubro Exhibit 17: Recommendation Summary Company CMP TP Rating Top-line EPS Adj. P/E OB/ (Rs) (Rs) FY10 FY11E FY12E CAGR (%) FY10 FY11E FY12E CAGR (%) FY10 FY11E FY12E Sale CCCL 86.2 - Neutral 1,976 2,444 2,871 20.5 5.0 6.0 7.5 22.5 17.2 14.4 11.5 2.3 GI 213.6 - Neutral 4,489 5,575 6,607 21.3 8.4 10.0 12.1 20.0 13.0 11.0 9.0 2.5 HCC 133 - Neutral 3,629 4,146 4,900 16.2 2.7 3.2 3.8 18.8 21.6 18.4 15.3 4.7 IRB Infra 257 289 Accumulate 1,705 2,778 3,580 44.9 11.6 12.3 14.5 11.8 22.2 20.8 17.7 - IVRCL 176 216 Buy 5,492 6,663 8,294 22.9 7.8 9.6 12.0 23.9 16.3 13.3 10.6 4.3 JP Assoc. 121 178 Buy 10,316 13,281 17,843 31.5 4.7 5.2 7.7 28.5 26.0 23.2 15.8 - Punj 130 170 Buy 10,539 11,088 13,407 12.8 (11.1) 8.3 12.2 - - 15.8 10.7 2.8 NCC 178 - Neutral 4,778 5,913 6,758 18.9 7.8 10.0 10.7 17.4 22.8 17.8 16.6 3.6 Sadbhav 1,290 - Neutral 1,257 1,560 1,911 23.3 43.0 57.5 69.5 27.1 20.3 15.2 12.5 5.4 SI. 476 570 Buy 4,555 5,535 6,428 18.8 25.7 31.9 40.7 25.9 18.5 14.9 11.7 2.5 PEL 409 563 Buy 3,081 3,685 4,297 18.1 23.4 31.2 32.9 18.6 13.1 9.8 9.3 3.5 MPL 157 190 Buy 1,308 1,701 2,120 27.3 5.8 6.4 9.8 29.8 9.3 8.4 5.5 3.1 L&T 1,863 - Neutral 37,035 44,047 55,519 22.4 47.5 55.1 68.9 20.4 30.9 26.7 21.3 2.7 Source: Company, Angel research Exhibit 18: SOTP valuation Company Core Const. Real Estate Road BOT Invst. In Subsidiaries Others Total Rs % to TP Rs % to TP Rs % to TP Rs % to TP Rs % to TP Rs CCCL 90 100 90 Gammon India 121 54 104 46 225 HCC 53 41 59 46 16 13 - - - - 128 IRB Infra 113 40 3 1 165 58 5 2 286 IVRCL 168 78 48 22 216 Punj Lloyd 170 100 - - - - 170 NCC 152 82 18 10 16 8 186 Simplex In. 570 100 570 Patel Engg 460 82 103 18 - 563 Madhucon 98 52 4 2 - - 88 46 190 L&T 1,447 79 - - 394 21 1,841 Source: Company, Angel research July 27 2010 9

- 10. 1QFY2011 Result Update | Larsen & Toubro Profit & Loss Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E Net Sales 17,567 24,855 33,647 36,675 43,680 55,130 Other operating income 38 23 280 360 367 388 Total operating income 17,605 24,878 33,926 37,035 44,047 55,519 % chg 19.2 41.3 36.4 9.2 18.9 26.0 Total Expenditure 15,825 22,051 30,094 32,295 38,701 48,831 Net Raw Materials 8,782 12,963 16,798 17,309 21,447 27,124 Other Mfg costs 4,755 6,168 9,434 11,144 12,230 15,437 Personnel 1,259 1,535 1,998 2,379 2,664 3,308 Other 1,028 1,386 1,864 1,463 2,359 2,962 EBITDA 1,780 2,826 3,832 4,739 5,347 6,688 % chg 58.8 35.6 23.7 12.8 25.1 (% of Net Sales) 10.1 11.4 11.4 12.9 12.2 12.1 Depreciation& Amortisation 168 202 283 380 492 607 EBIT 1,612 2,624 3,550 4,360 4,855 6,081 % chg 62.8 35.3 22.8 11.4 25.3 (% of Net Sales) 9.2 10.6 10.5 11.9 11.1 11.0 Interest & other Charges 93 123 350 505 614 735 Other Income (incl pft from Ass/JV) 454 488 643 768 922 1,112 (% of PBT) 23.0 16.3 16.7 16.6 17.9 17.2 Recurring PBT 1,973 2,989 3,842 4,623 5,163 6,458 % chg 51.5 28.5 20.3 11.7 25.1 Extraordinary Expense/(Inc.) (32) (166) (871) (1,394) - - PBT (reported) 2,005 3,155 4,713 6,016 5,163 6,458 Tax 602 982 1,231 1,641 1,704 2,131 (% of PBT) 30.0 31.1 26.1 27.3 33.0 33.0 PAT (reported) 1,403 2,173 3,482 4,376 3,459 4,327 Less: Minority interest (MI) - - - - - - Prior period items - - - - - - PAT after MI (reported) 1,403 2,173 3,482 4,376 3,459 4,327 ADJ. PAT 1,330 1,960 2,595 2,893 3,353 4,194 % chg 66.7 47.5 32.4 11.5 15.9 25.1 (% of Net Sales) 7.6 7.9 7.7 7.9 7.7 7.6 Basic EPS (Rs) (Reported) 49.5 74.3 59.2 72.6 56.8 71.1 Fully Diluted EPS (Rs) (Diluted) 21.8 32.2 42.6 47.5 55.1 68.9 % chg 47.5 32.4 11.5 15.9 25.1 July 27 2010 10

- 11. 1QFY2011 Result Update | Larsen & Toubro Balance Sheet Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E SOURCES OF FUNDS Equity Share Capital 56.7 58.5 117.5 120.5 121.7 121.7 Preference Capital - - - - - - Reserves& Surplus 5,711.8 9,496.6 12,342.6 18,191.1 21,725.4 25,125.3 Shareholders Funds 5,768.4 9,555.1 12,460.1 18,311.7 21,847.1 25,247.0 Minority Interest - - - - - - Total Loans 2,077.7 3,584.0 6,556.0 6,800.8 7,385.3 8,671.3 Deferred Tax Liability 40.2 61.4 48.5 77.4 77.4 77.4 Total Liabilities 7,886.3 13,200.4 19,064.6 25,189.9 29,309.8 33,995.7 APPLICATION OF FUNDS Gross Block 2,876.0 4,188.9 5,575.0 7,235.8 8,914.3 11,048.6 Less: Acc. 1,087.0 1,239.4 1,418.3 1,727.7 2,219.3 2,826.2 Depreciation Net Block 1,789.0 2,949.5 4,156.7 5,508.1 6,695.0 8,222.4 Capital Work-in- 435.7 695.9 1,037.9 857.7 1,029.2 1,235.0 Progress Goodwill - - - - - - Investments 3,104.4 6,922.3 8,263.7 13,705.4 14,705.4 15,705.4 Current Assets 11,903.8 16,313.5 23,448.0 26,361.6 31,645.6 39,927.0 Cash 1,094.4 964.5 775.3 1,431.9 1,209.1 1,085.9 Loans & Advances 2,277.1 3,663.8 6,790.6 5,997.5 7,844.0 10,647.4 Other 8,532.3 11,685.2 15,882.1 18,932.3 22,592.5 28,193.6 Current liabilities 9,356.4 13,683.8 17,842.4 21,242.9 24,765.3 31,094.0 Net Current Assets 2,547.4 2,629.7 5,605.6 5,118.8 6,880.3 8,832.9 Mis. Exp. not written 9.8 3.1 0.3 - - - off Total Assets 7,886.4 13,200.4 19,064.2 25,189.9 29,309.8 33,995.7 July 27 2010 11

- 12. 1QFY2011 Result Update | Larsen & Toubro Cash Flow Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E Profit before tax 2,004.9 3,155.5 4,712.9 5,880.7 5,163.3 6,458.3 Depreciation 168.2 202.2 282.8 387.0 491.6 606.9 Change in Working Capital (706.4) 376.7 2,048.7 (1,143.4) 1,984.3 2,075.8 Less: Other income 454.2 487.9 642.9 768.2 921.9 1,111.6 Direct taxes paid 604.3 988.3 873.1 1,519.3 1,703.9 2,131.2 Cash Flow from Operations 1,821.0 1,504.7 1,431.0 5,123.6 1,044.8 1,746.5 (Inc.)/ Dec. in Fixed Assets (775.2) (1,622.1) (1,979.8) (1,480.5) (1,850.1) (2,340.1) (Inc.)/ Dec. in Investments (1,072.6) (3,619.8) (1,328.7) (5,441.6) (1,000.0) (1,000.0) Other income 454.2 487.9 642.9 768.2 921.9 1,111.6 Cash Flow from Investing (1,393.6) (4,754.0) (2,665.6) (6,153.9) (1,928.2) (2,228.5) Issue of Equity 23.9 1,701.6 23.0 2,132.7 958.0 - Inc./(Dec.) in loans 739.4 1,559.8 1,921.8 168.0 584.5 1,285.9 Dividend Paid (Incl. Tax) 619.5 114.1 438.8 719.2 880.7 924.8 Others (60.0) (28.0) (461.0) 105.0 (1.0) (2.0) Cash Flow from Financing 83.9 3,119.3 1,045.1 1,686.6 660.8 359.2 Inc./(Dec.) in Cash 511.3 (130.0) (189.5) 656.3 (222.6) (122.8) Opening Cash balances 582.8 1,094.9 964.8 775.3 1,431.6 1,209.1 Closing Cash balances 1,094.1 964.9 775.3 1,431.6 1,209.1 1,086.3 July 27 2010 12

- 13. 1QFY2011 Result Update | Larsen & Toubro Key Ratios Y/E March FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E Valuation Ratio (x) P/E (on FDEPS) 85.3 57.8 43.7 39.2 33.8 27.0 P/CEPS 75.7 52.4 39.4 34.6 29.5 23.6 P/BV 19.7 11.9 9.1 6.2 5.2 4.5 Dividend yield (%) 0.6 0.7 0.5 0.5 0.7 0.7 EV/Sales 6.5 4.7 3.5 3.2 2.7 2.2 EV/EBITDA 64.2 41.0 31.1 25.1 22.4 18.1 EV / Total Assets 14.5 8.8 6.2 4.7 4.1 3.6 Order Book to Sales 2.1 2.1 2.1 2.7 3.2 3.3 Per Share Data (Rs) EPS (Basic) 49.5 74.3 59.2 72.6 56.8 71.1 EPS (fully diluted) 21.8 32.2 42.6 47.5 55.1 68.9 Cash EPS 24.6 35.5 47.3 53.8 63.2 78.9 DPS 10.7 12.6 8.4 10.2 12.4 12.4 Book Value 94.8 157.0 204.8 300.9 359.0 414.9 Dupont Analysis EBIT margin 9.2 10.5 10.5 11.8 11.0 11.0 Tax retention ratio 0.7 0.7 0.7 0.7 0.7 0.7 Asset turnover (x) 2.6 2.6 2.2 1.8 1.7 1.8 ROIC (Post-tax) 16.6 19.0 17.2 15.1 12.5 13.4 Cost of Debt (Post Tax) 3.1 3.0 5.1 5.5 5.8 6.1 Leverage (x) 0.2 0.2 0.4 0.4 0.3 0.3 Operating ROE 18.9 22.8 21.8 18.6 14.5 15.5 Returns (%) ROCE (Pre-tax) 20.4 24.9 22.0 19.7 17.8 19.2 Angel ROIC (Pre-tax) 23.7 27.6 23.3 20.7 18.7 19.9 ROAE 23.0 25.6 23.6 18.8 16.7 17.8 Turnover ratios (x) Asset Turnover (Gross Block) 6.1 7.0 6.9 5.8 5.5 5.6 Inventory / Sales (days) 54 54 54 36 13 13 Receivables (days) 107 94 94 105 101 99 Payables (days) 61 60 63 73 79 73 Working capital cycle (ex-cash) (days) 36.2 22.9 34.9 42.0 38.8 44.1 Solvency ratios (x) Net debt to equity 0.2 0.3 0.5 0.3 0.3 0.3 Net debt to EBITDA 0.6 0.9 1.5 1.1 1.2 1.1 Interest Coverage (EBIT / Interest) 17.3 21.4 10.1 8.6 7.9 8.3 July 27 2010 13

- 14. 1QFY2011 Result Update | Larsen & Toubro Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com DISCLAIMER This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past. Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information. Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have investment positions in the stocks recommended in this report. Disclosure of Interest Statement L&T 1. Analyst ownership of the stock No 2. Angel and its Group companies ownership of the stock Yes 3. Angel and its Group companies' Directors ownership of the stock No 4. Broking relationship with company covered No Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors. Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%) July 27 2010 14